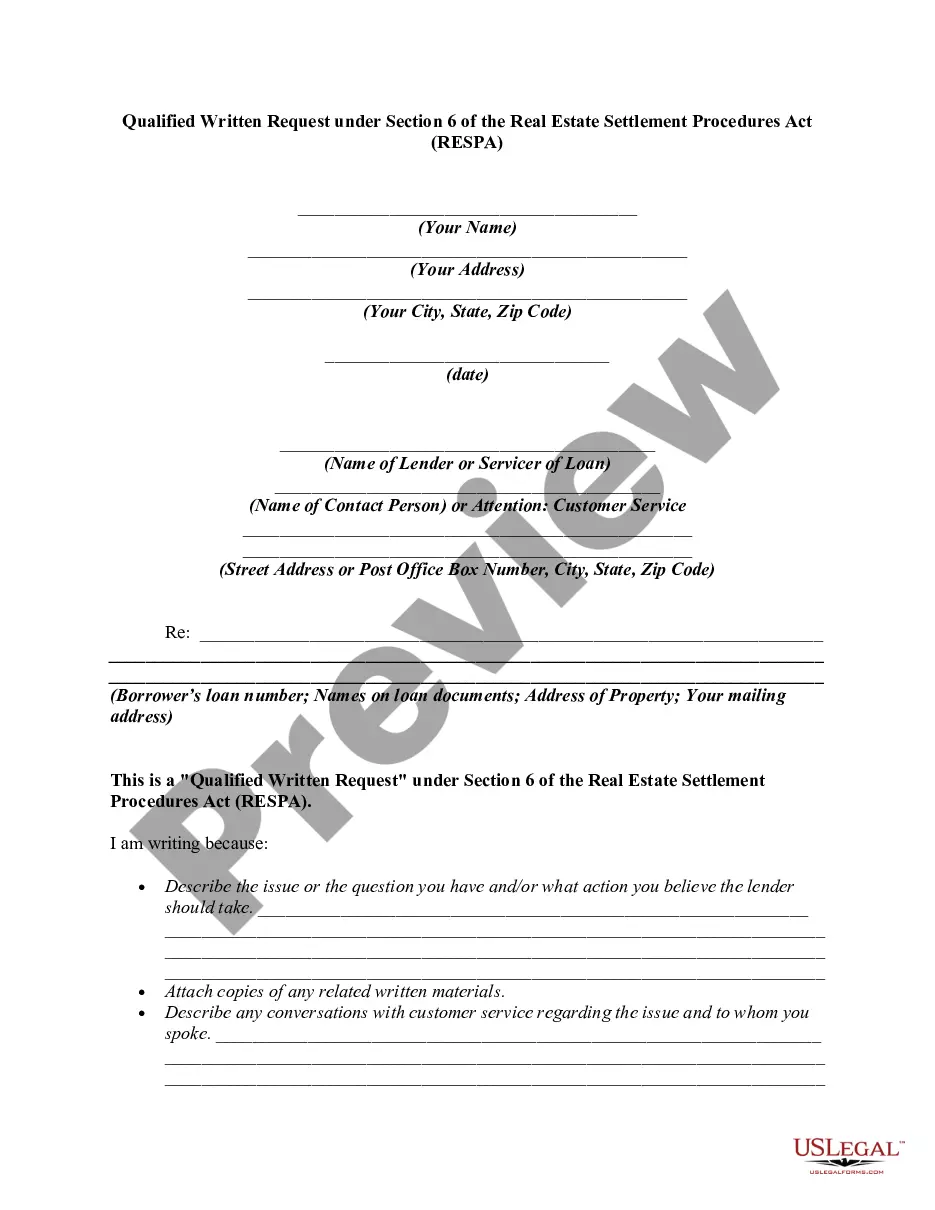

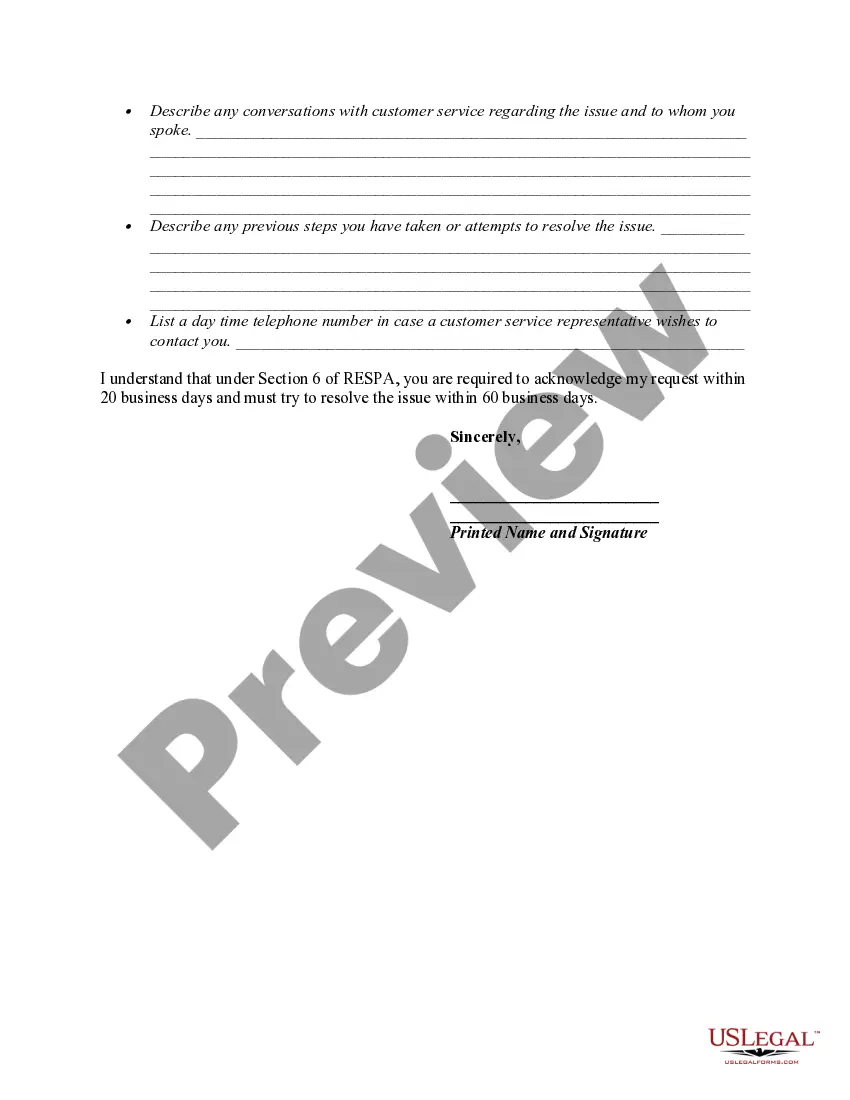

12 USC 2605(e) creates a duty of a loan servicer to respond to the inquiries of borrowers regarding loans covered by RESPA. If the borrower believes there is an error in the mortgage account, he or she can make a "qualified written request" to the loan servicer. The request must be in writing, identify the borrower by name and account, and include a statement of reasons why the borrower believes the account is in error. The request should include the words "qualified written request". It cannot be written on the payment coupon, but must be on a separate piece of paper. The Department of Housing and Urban Development provides a sample letter.

The servicer must acknowledge receipt of the request within 20 days. The servicer then has 60 days (from the request) to take action on the request. The servicer has to either provide a written notification that the error has been corrected, or provide a written explanation as to why the servicer believes the account is correct. Either way, the servicer has to provide the name and telephone number of a person with whom the borrower can discuss the matter.

Minnesota Qualified Written Request (BWR) is a powerful tool provided under Section 6 of the Real Estate Settlement Procedures Act (RESP) that allows borrowers in Minnesota to formally request information, seek clarification, or resolve issues related to their mortgage loan. The BWR serves as a means for borrowers to communicate their concerns and receive a timely and detailed response from their loan service or lender. Under Section 6 of RESP, the Minnesota BWR empowers borrowers to seek information or lodge complaints regarding the servicing or administration of their mortgage loan. It ensures transparency, fairness, and accountability in the mortgage lending process. By submitting a BWR, borrowers can address issues such as errors in loan statements, unauthorized fees, incorrect loan payment applications, or inadequate escrow account management. The Minnesota BWR should include specific details to help the loan service or lender understand the concerns clearly. Important components of a BWR include the borrower's name, loan number, and property address. Borrowers should describe the issue(s) they are experiencing concisely and provide supporting documentation if available. Additionally, it is essential to request specific actions or information to resolve the problem. Regarding types of Minnesota Was, there are no specific subtypes distinguished under Section 6 of RESP. However, borrowers may submit Was for various reasons, including but not limited to: 1. Loan Statement Discrepancies: Borrowers can request an explanation for discrepancies between their loan statements and actual payments made. This may involve incorrect application of payments, allocation of funds, or the inclusion of unauthorized fees. 2. Escrow Account Issues: If borrowers suspect improper handling of their escrow account, such as miscalculations, inadequate disbursements for taxes and insurance, or unjustified shortages or surpluses in the account, they can file a BWR to rectify the situation. 3. Loan Modification or Loss Mitigation Queries: Borrowers seeking loan modification or exploring loss mitigation options, like loan refinancing or foreclosure alternatives, can submit a BWR to gather relevant information, determine eligibility, or address concerns. 4. Unresolved Complaints: If borrowers have previously filed complaints with their loan service or lender but have not received satisfactory responses or resolutions, they can escalate the matter by serving a BWR to ensure their concerns are appropriately addressed. It is crucial for borrowers in Minnesota to be informed about their rights under Section 6 of RESP, allowing them to leverage the Minnesota BWR effectively. Submitting a BWR can be a vital step in resolving mortgage-related issues and ensuring fair treatment throughout the loan servicing process.Minnesota Qualified Written Request (BWR) is a powerful tool provided under Section 6 of the Real Estate Settlement Procedures Act (RESP) that allows borrowers in Minnesota to formally request information, seek clarification, or resolve issues related to their mortgage loan. The BWR serves as a means for borrowers to communicate their concerns and receive a timely and detailed response from their loan service or lender. Under Section 6 of RESP, the Minnesota BWR empowers borrowers to seek information or lodge complaints regarding the servicing or administration of their mortgage loan. It ensures transparency, fairness, and accountability in the mortgage lending process. By submitting a BWR, borrowers can address issues such as errors in loan statements, unauthorized fees, incorrect loan payment applications, or inadequate escrow account management. The Minnesota BWR should include specific details to help the loan service or lender understand the concerns clearly. Important components of a BWR include the borrower's name, loan number, and property address. Borrowers should describe the issue(s) they are experiencing concisely and provide supporting documentation if available. Additionally, it is essential to request specific actions or information to resolve the problem. Regarding types of Minnesota Was, there are no specific subtypes distinguished under Section 6 of RESP. However, borrowers may submit Was for various reasons, including but not limited to: 1. Loan Statement Discrepancies: Borrowers can request an explanation for discrepancies between their loan statements and actual payments made. This may involve incorrect application of payments, allocation of funds, or the inclusion of unauthorized fees. 2. Escrow Account Issues: If borrowers suspect improper handling of their escrow account, such as miscalculations, inadequate disbursements for taxes and insurance, or unjustified shortages or surpluses in the account, they can file a BWR to rectify the situation. 3. Loan Modification or Loss Mitigation Queries: Borrowers seeking loan modification or exploring loss mitigation options, like loan refinancing or foreclosure alternatives, can submit a BWR to gather relevant information, determine eligibility, or address concerns. 4. Unresolved Complaints: If borrowers have previously filed complaints with their loan service or lender but have not received satisfactory responses or resolutions, they can escalate the matter by serving a BWR to ensure their concerns are appropriately addressed. It is crucial for borrowers in Minnesota to be informed about their rights under Section 6 of RESP, allowing them to leverage the Minnesota BWR effectively. Submitting a BWR can be a vital step in resolving mortgage-related issues and ensuring fair treatment throughout the loan servicing process.