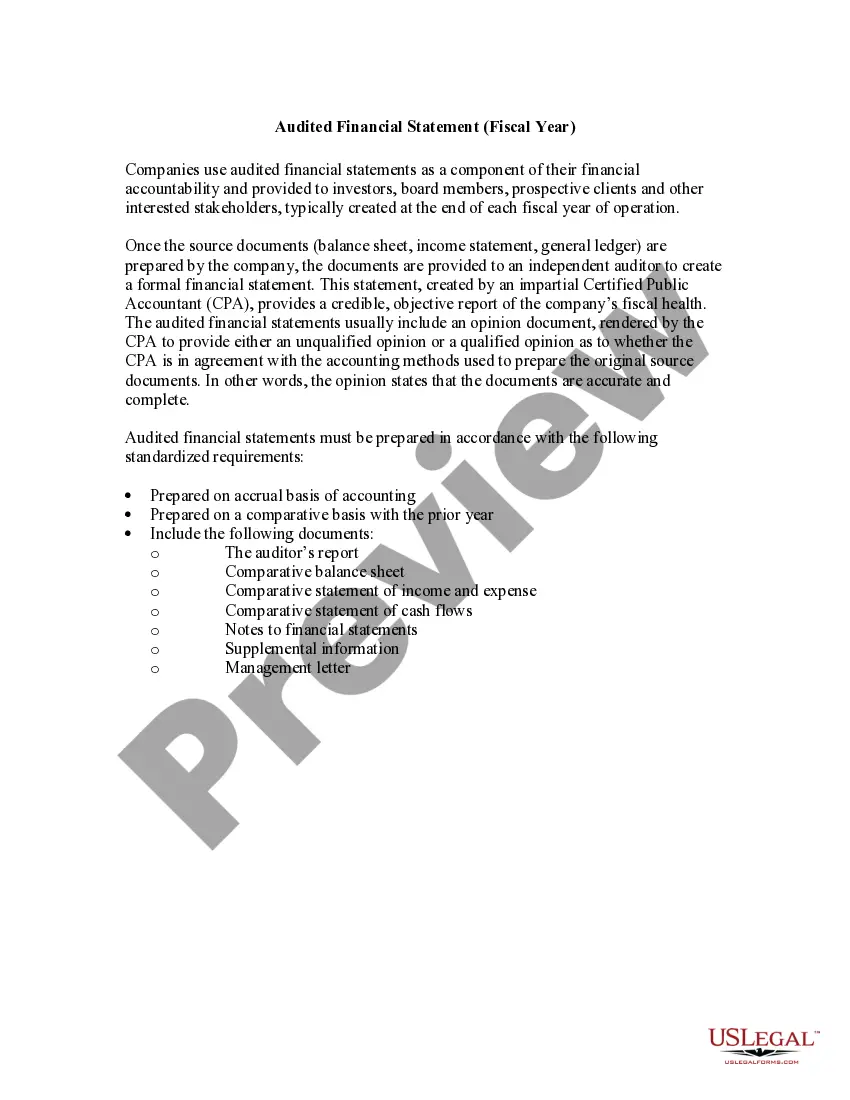

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

Minnesota Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

Locating the appropriate legal document template may be a challenge.

Clearly, there are numerous formats available online, but how can you acquire the legal form you require.

Use the US Legal Forms website.

If you are already a registered user, Log In to your account and click the Download button to receive the Minnesota Report of Independent Accountants after Audit of Financial Statements. Use your account to browse through the legal documents you have previously purchased. Navigate to the My documents section of your account and retrieve another copy of the document you need.

- The service provides a vast array of templates, including the Minnesota Report of Independent Accountants following the Audit of Financial Statements, which you can utilize for business and personal purposes.

- All templates are verified by experts and comply with state and federal regulations.

Form popularity

FAQ

An independent auditor reports on financial statements to provide an unbiased opinion on their accuracy and fairness. This reporting helps build trust among investors, creditors, and other stakeholders who rely on these financial assertions. By issuing a report, auditors enhance the credibility of the information, which is essential in the context of the Minnesota Report of Independent Accountants after Audit of Financial Statements. Employing tools from platforms like USLegalForms can simplify obtaining these reports, ensuring adherence to legal standards.

An accountant's review report is a formal document resulting from a review of financial statements by an independent accountant. This report expresses limited assurance, reflecting that no significant issues were found during the review process. It helps businesses and stakeholders understand their financial status without the extensive procedures of an audit. This review plays a vital role in the broader context of the Minnesota Report of Independent Accountants after Audit of Financial Statements.

The three main types of accounting reports are audits, reviews, and compilations. An audit provides the highest level of assurance, while a review offers limited assurance through analytical procedures. A compilation is the most basic level of reporting, presenting financial information without assurance. All these reports may be relevant to understanding the nuances of the Minnesota Report of Independent Accountants after Audit of Financial Statements.

An independent review report is a document that provides assurance on financial statements. It is issued by a qualified accountant after reviewing the financial information of a business. This type of report typically falls between a full audit and a compilation, offering an efficient way to validate financial data while providing insights. In Minnesota, this report can be included in the Minnesota Report of Independent Accountants after Audit of Financial Statements.

You can find an independent auditor's report on a company's official website, specifically in the investor relations section, or through public financial databases. Public companies are often required to maintain transparency and make these reports easily accessible. By consulting the Minnesota Report of Independent Accountants after Audit of Financial Statements, you can locate and review these important documents.

Generally, a company needs to provide at least two to three years of audited financial statements when planning to go public. These years of financial data help demonstrate the company’s stability and growth potential, assuring investors of its credibility. For further clarity, examining the Minnesota Report of Independent Accountants after Audit of Financial Statements can lend valuable context.

To find a company's audit report, you can search through publicly available financial filings on the company's website or through regulatory bodies like the SEC. This information is typically present in annual reports or Form 10-K filings. By reviewing the Minnesota Report of Independent Accountants after Audit of Financial Statements, you will have access to detailed financial insights.

An independent accountant's report is a statement issued by an accountant attesting to the accuracy and fairness of a company's financial statements. Unlike an audit, this review does not provide the same level of assurance, but it still offers valuable insights. This report is often referenced when discussing the Minnesota Report of Independent Accountants after Audit of Financial Statements.

Audited financial statements are typically public information for organizations required to file with the SEC or other regulatory bodies. This ensures that stakeholders have access to vital financial data necessary for informed decision-making. By reviewing the Minnesota Report of Independent Accountants after Audit of Financial Statements, you can gain a comprehensive understanding of a company's financial performance.

Yes, audited financial statements are often considered public documents, especially for publicly traded companies. This transparency allows investors and other interested parties to evaluate the company's financial position. Therefore, accessing the Minnesota Report of Independent Accountants after Audit of Financial Statements can provide detailed insights into a company's financial health.