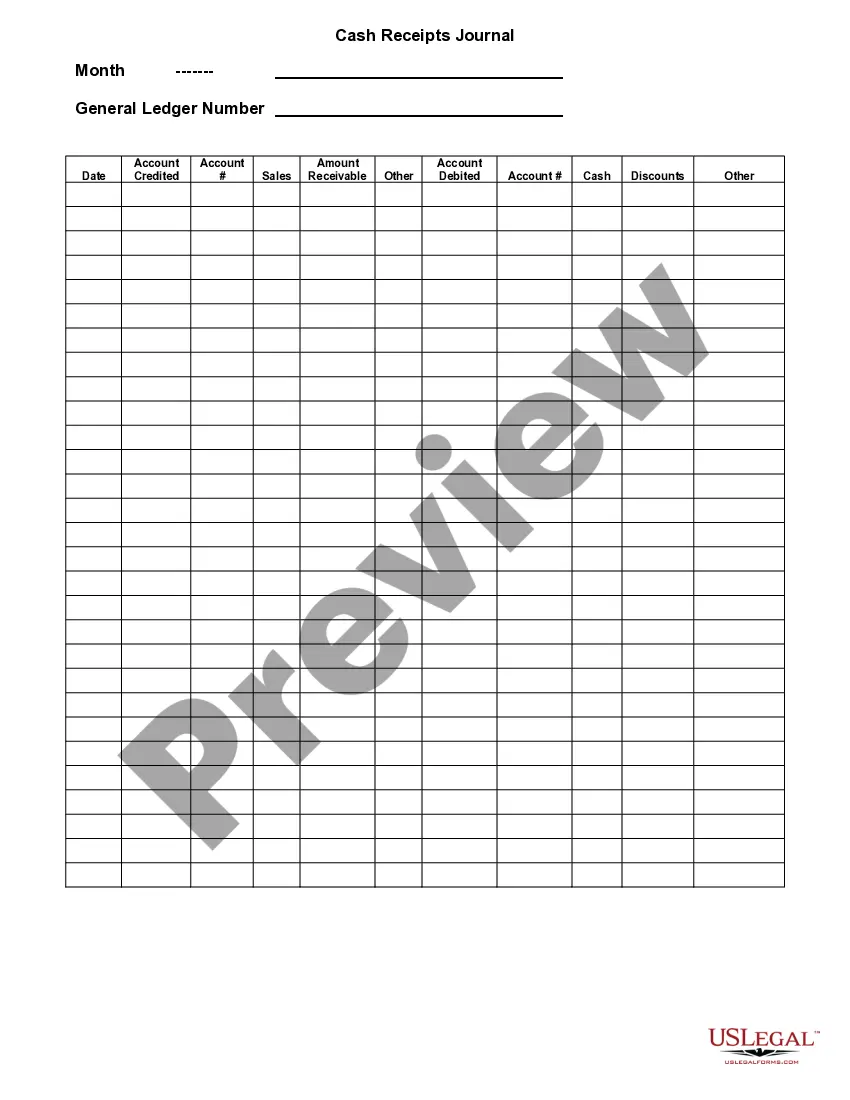

Minnesota Cash Receipts Control Log

Description

How to fill out Cash Receipts Control Log?

Selecting the appropriate legitimate document template can be challenging.

Of course, there are numerous templates accessible online, but how can you find the legitimate form you need.

Utilize the US Legal Forms website. The service offers thousands of templates, such as the Minnesota Cash Receipts Control Log, which can be utilized for both business and personal purposes.

If the document does not meet your needs, use the Search field to find the right one. Once you are confident that the form is appropriate, click on the Purchase now button to obtain it. Choose the payment plan you prefer and enter the required details. Create your account and pay for the order using your PayPal account or credit card. Select the file format and download the legitimate document template to your system. Complete, modify, print, and sign the acquired Minnesota Cash Receipts Control Log. US Legal Forms is the largest library of legal forms where you can find various document templates. Take advantage of the service to obtain professionally crafted documents that meet state requirements.

- All forms are reviewed by experts and comply with state and federal regulations.

- If you are already registered, Log In to your account and click on the Download button to acquire the Minnesota Cash Receipts Control Log.

- Use your account to browse through the legitimate forms you have previously acquired.

- Go to the My documents section of your account to retrieve another copy of the document you need.

- As a new user of US Legal Forms, here are simple steps you can follow.

- First, ensure you have selected the correct form for your city/county. You can review the document using the Preview option and read the form description to confirm it is suitable for you.

Form popularity

FAQ

This is how to post to the cash receipts journal. First, you will post the total of the cash column to the general ledger in the cash account as a debit. Next, you'll take the total of the sales column and post it to the general ledger in the cash account as a debit.

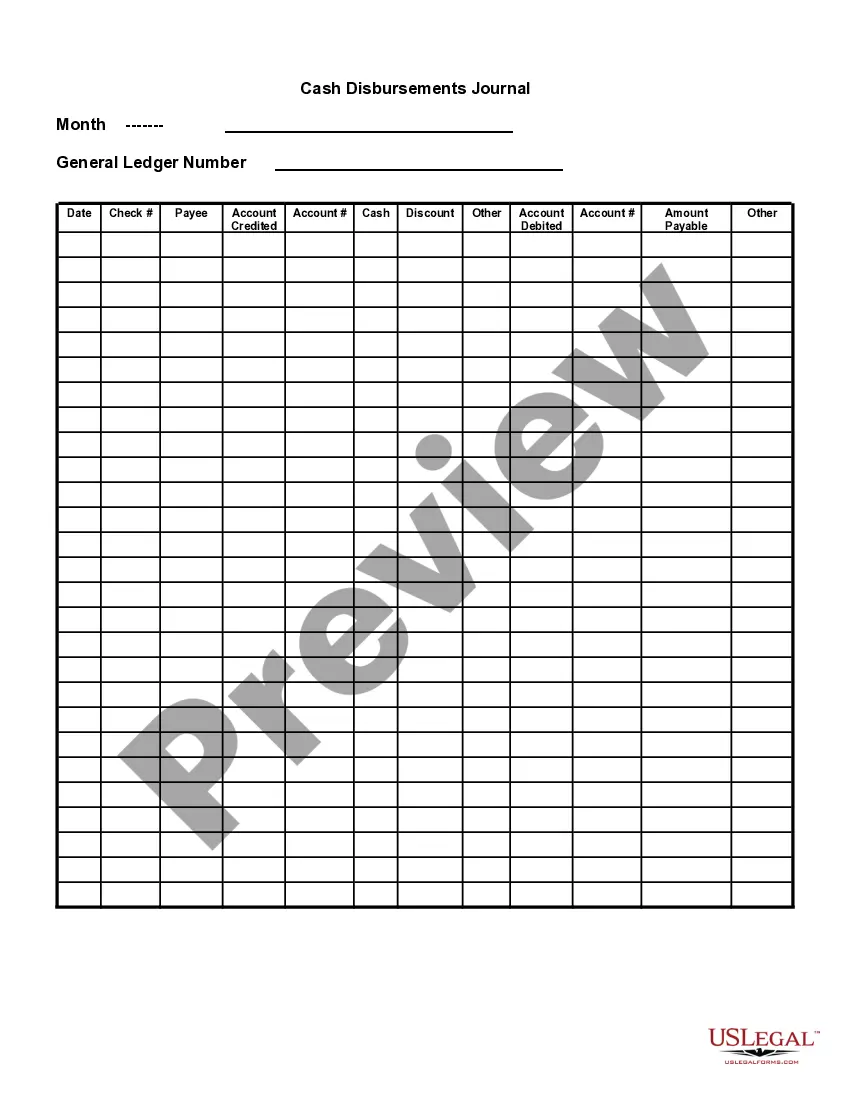

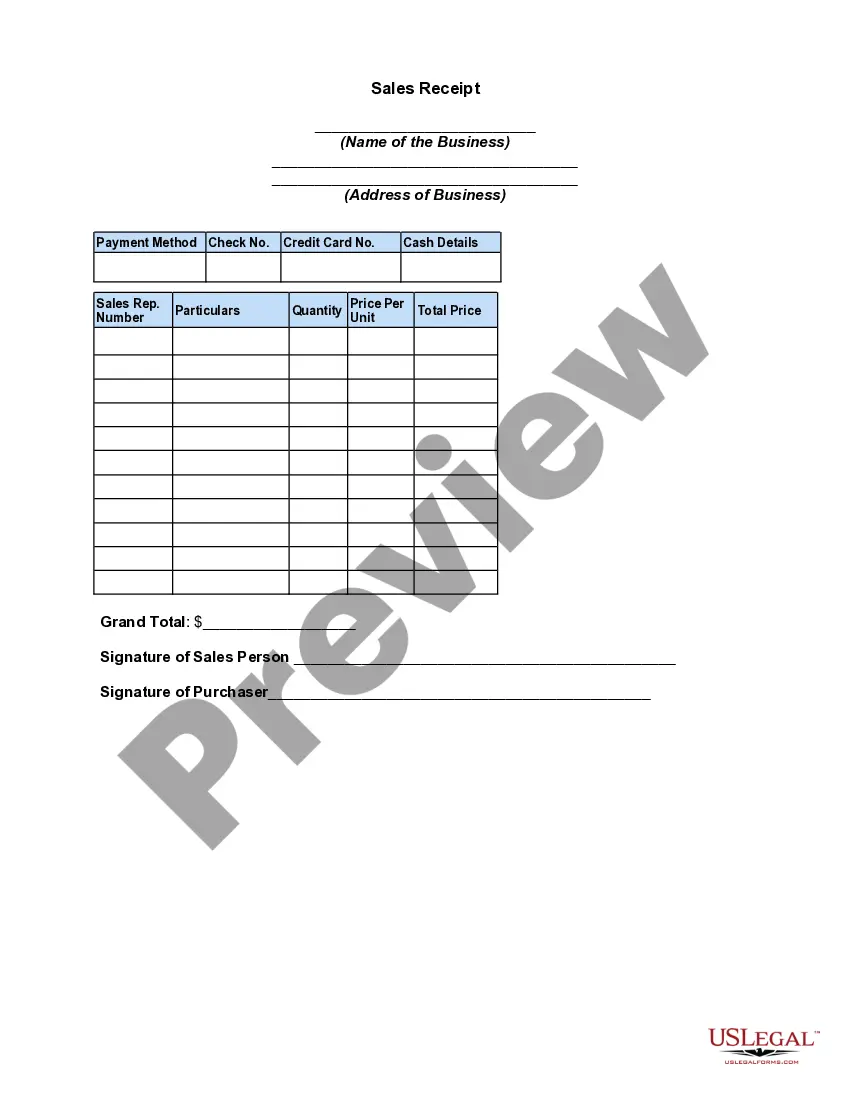

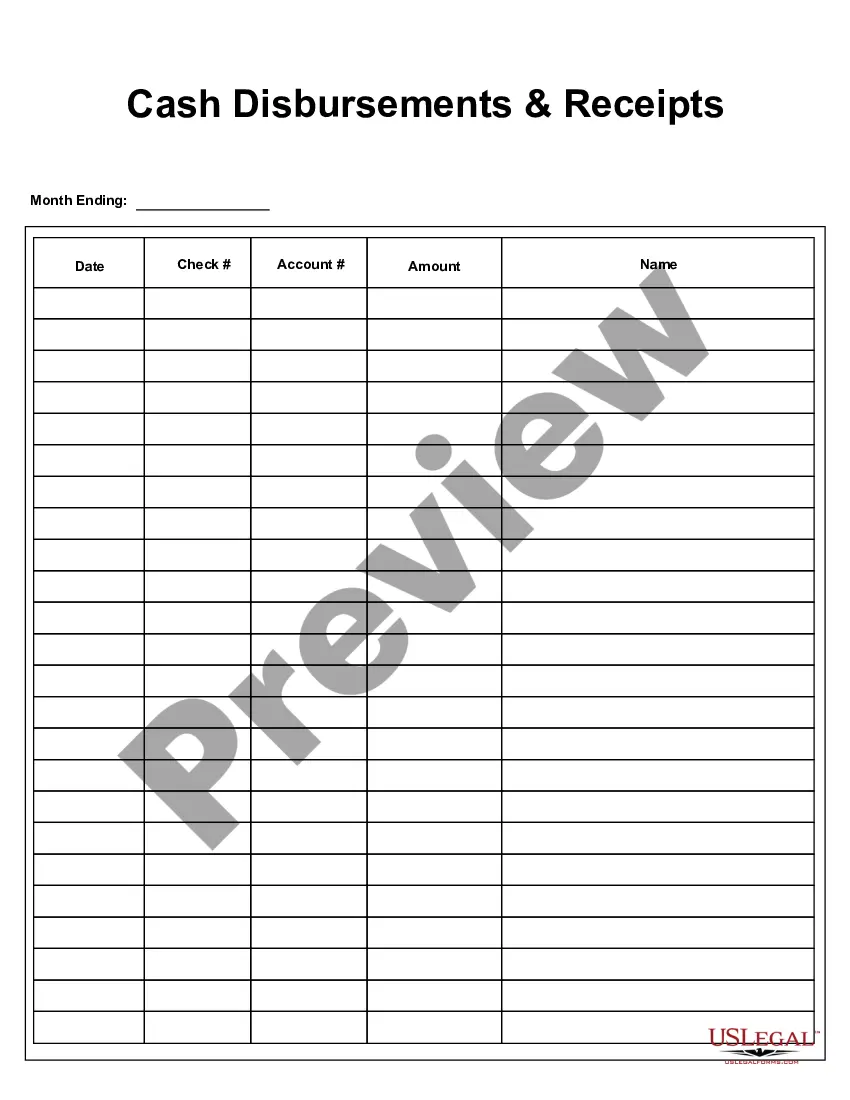

Record Checks and Cash For each check received, state on the form the name of the paying party, the check number and the amount paid. If the receipt was in cash, then state the name of the paying party, check the cash? box, and the amount paid.

This includes cash sales, receipt of funds from a bank loan, payments from customer accounts, and the sale of assets.

What are cash receipts? You record cash receipts when your business receives cash from an external source, such as a customer, investor, or bank. And when you collect money from a customer, you need to record the transaction and reflect the sale on your balance sheet.

A cash receipt business log is a source document used during cash transactions when receipts or a cash register may not be available.

A cash receipts log is used to track the cash receipts of a business. Although the format of the cash receipts log varies from business to business, the essential details presented on the form are the same and include the customer's name, amount of cash receipt and details related to the payment.

Best practices:Record cash receipts when received.Keep funds secured.Document transfers.Give receipts to each customer.Don't share passwords.Give each cashier a separate cash drawer.Supervisors verify cash deposits.Supervisors approve all voided refunded transactions.

Record any cash payments as a debit in your cash receipts journal like usual. Then, debit the customer's accounts receivable account for any purchase made on credit. In your sales journal, record the total credit entry.

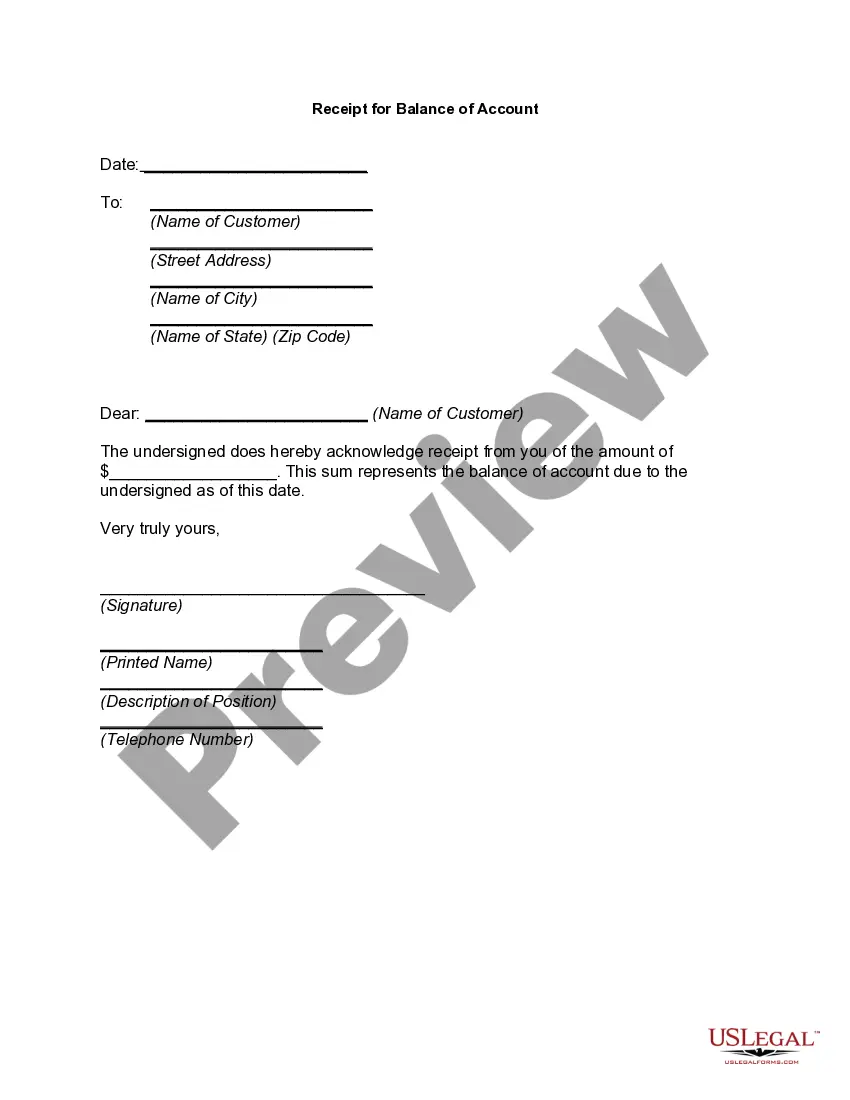

A cash receipt is a printed acknowledgement of the amount of cash received during a transaction involving the transfer of cash or cash equivalent. The original copy of the cash receipt is given to the customer, while the other copy is kept by the seller for accounting purposes.

Record any cash payments as a debit in your cash receipts journal like usual. Then, debit the customer's accounts receivable account for any purchase made on credit. In your sales journal, record the total credit entry.