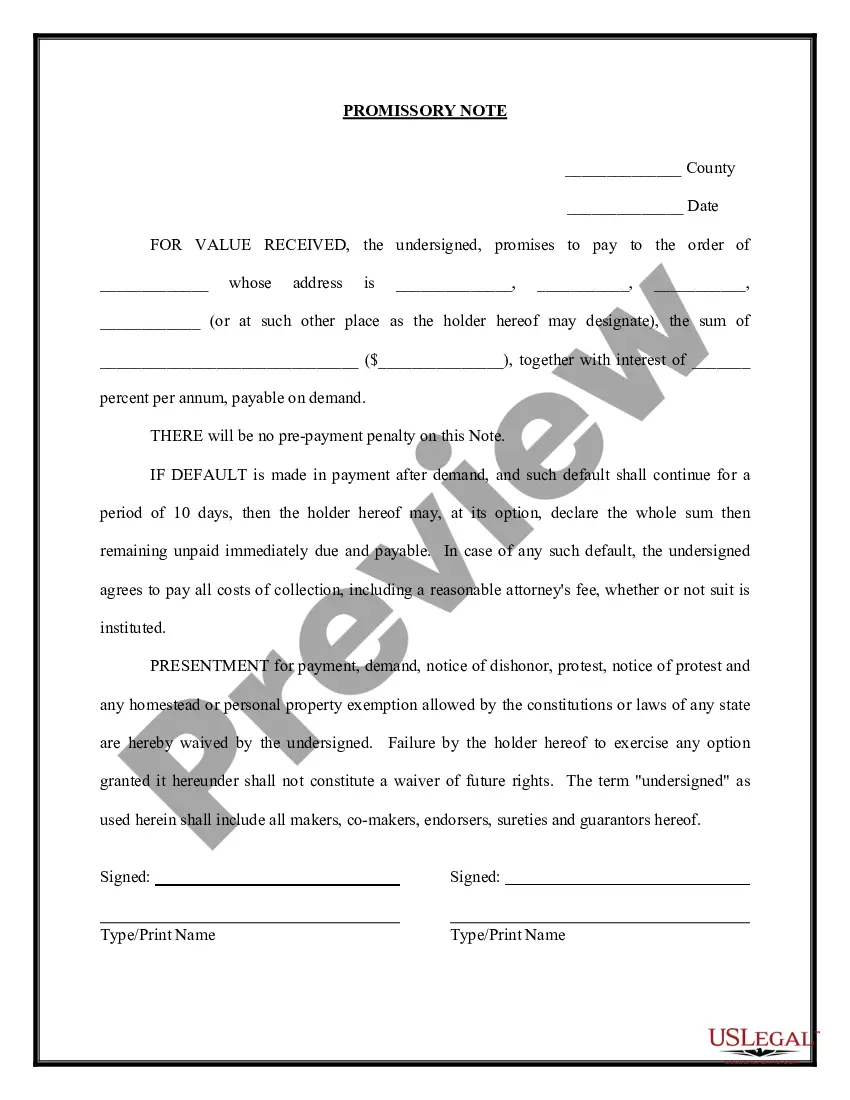

Minnesota Demand Promissory Note

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Demand Promissory Note?

US Legal Forms - one of the largest collections of legal templates in the USA - provides a variety of legal document formats that you can download or print.

Through the website, you can access thousands of templates for business and personal purposes, categorized by types, states, or keywords. You can find the latest versions of documents like the Minnesota Demand Promissory Note in just a few minutes.

If you already have a monthly subscription, Log In and download the Minnesota Demand Promissory Note from the US Legal Forms library. The Download button will appear on each form you view. You can access all previously acquired forms from the My documents tab in your account.

Complete the transaction. Use your credit card or PayPal account to finalize the purchase.

Select the format and download the form to your device. Make modifications. Fill out, edit, print, and sign the downloaded Minnesota Demand Promissory Note. Every template you add to your account has no expiration date and is yours permanently. Thus, if you wish to download or print another copy, simply visit the My documents section and click on the desired form. Gain access to the Minnesota Demand Promissory Note with US Legal Forms, the most extensive library of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs and specifications.

- Ensure you have selected the correct form for your city/state.

- Click the Preview button to review the form's details.

- Check the form description to confirm that you have chosen accurately.

- If the form does not meet your needs, utilize the Search section at the top of the screen to find the one that does.

- Once you are satisfied with the form, confirm your selection by clicking the Purchase now button.

- Next, choose your pricing plan and provide your details to create an account.

Form popularity

FAQ

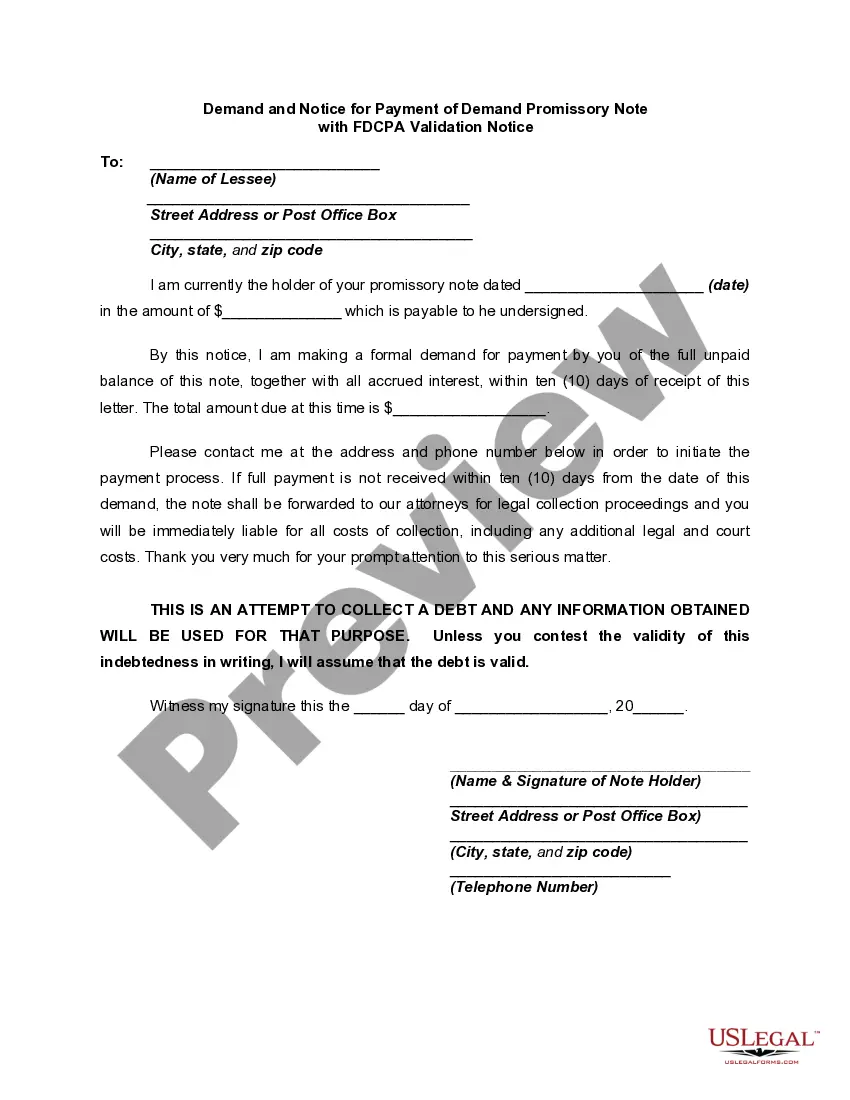

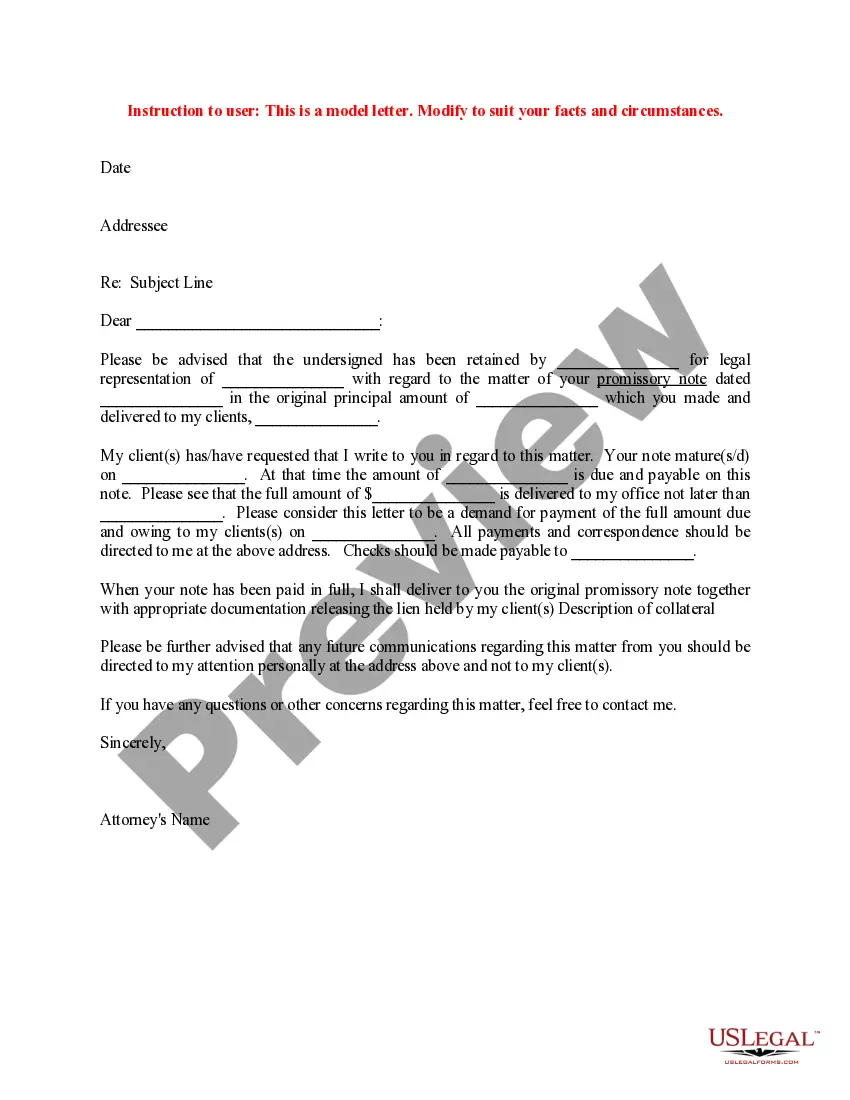

To effectively demand payment on your Minnesota Demand Promissory Note, send a formal written notice to the borrower. In this notice, specify the amount owed, cite the due date, and include any interest calculations if applicable. Taking a methodical approach helps reinforce your position and can motivate timely payment.

Yes, a promissory note can be made payable on demand, which is a common feature in Minnesota Demand Promissory Notes. This means the lender can request payment at any time, offering flexibility. It's essential to clearly state this condition in the note to avoid any misunderstandings.

To demand payment on a Minnesota Demand Promissory Note, begin by reviewing the terms stated in the document. You typically send a written demand to the borrower, specifying the amount due and any applicable deadlines. This formal approach helps maintain clarity and sets a professional tone for the transaction.

To obtain your Minnesota Demand Promissory Note, you can use online resources like USLegalForms. Simply select the appropriate form tailored to Minnesota's laws, fill it out accurately, and download it for your records. Having a formal promissory note is essential to ensure all parties are on the same page regarding payment terms.

Writing a simple promissory note involves stating the key elements: the lender's name, borrower's name, amount borrowed, interest rate, and due date. For a Minnesota Demand Promissory Note, emphasize that repayment is required upon demand. Make sure the note is written in clear, concise language, and both parties sign the document to make it enforceable.

Examples of promissory notes include personal loans, student loans, and business loans. A Minnesota Demand Promissory Note may be used in various situations where lenders want immediate payment upon demand or during a specified period. Each note can be tailored to fit the specific needs of the transaction.

In Minnesota, notarization is not a strict requirement for a promissory note to be legally enforceable. However, having a Minnesota Demand Promissory Note notarized enhances its credibility and can aid in resolving disputes if they arise. It is generally a good practice to have the document notarized to protect both parties involved.

A Minnesota Demand Promissory Note may be deemed invalid if it lacks essential information or does not meet legal requirements. For example, if the note does not specify a repayment amount or lacks signatures from both parties, it may not hold up in court. Additionally, notes executed under duress or fraud can also be invalid. It is crucial to follow the correct guidelines to ensure your demand promissory note remains enforceable.

Yes, a Minnesota Demand Promissory Note can indeed be structured to be payable to the bearer on demand. This means that anyone holding the note can present it for payment at any time. However, it is vital to ensure the language in the note clearly states this stipulation. By using the right terms, you can create flexibility in how the note can be redeemed.

Indeed, a Minnesota Demand Promissory Note qualifies as a demand instrument. This type of note signifies that the borrower must repay upon request, which provides the lender with control over the repayment timeline. Understanding this characteristic ensures that everyone involved knows their rights and responsibilities.