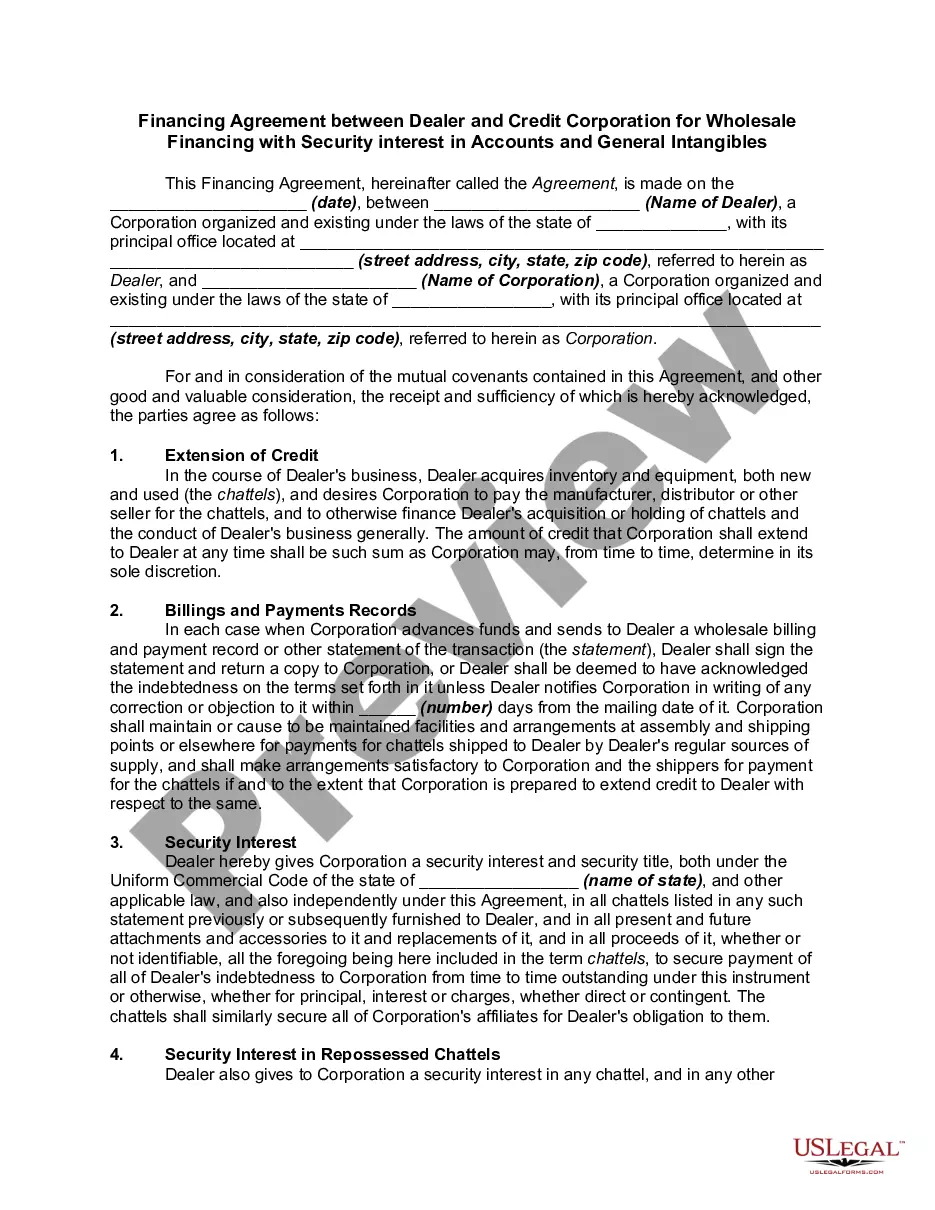

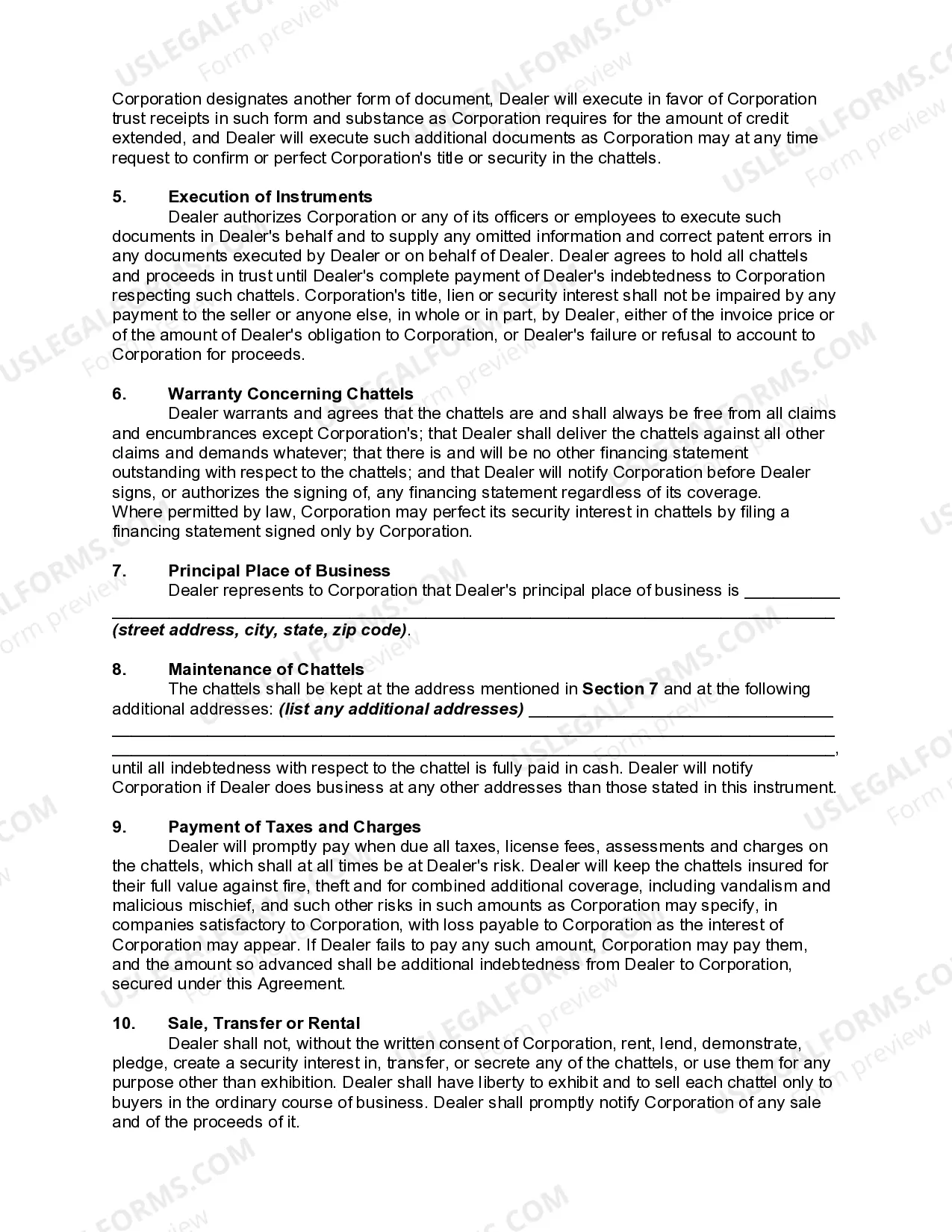

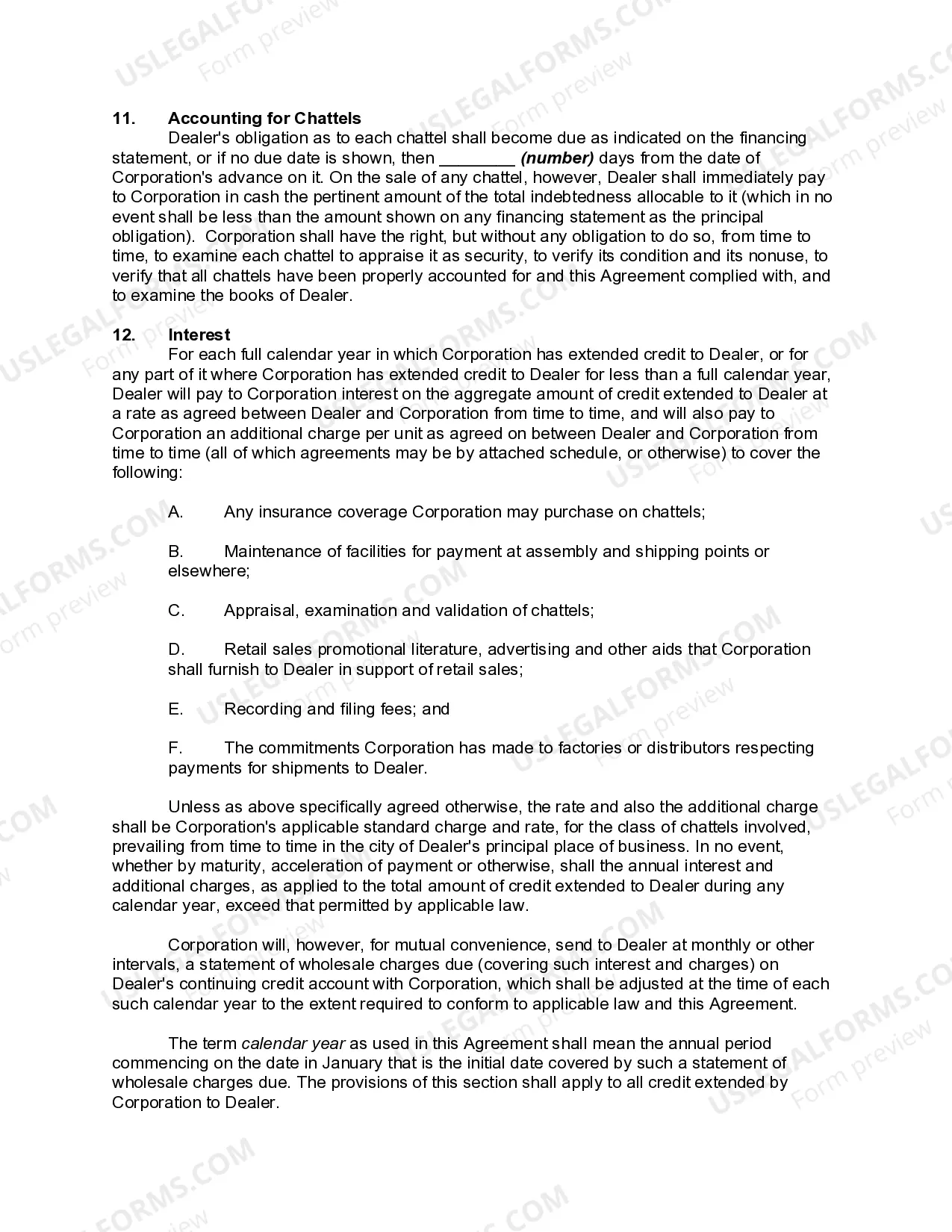

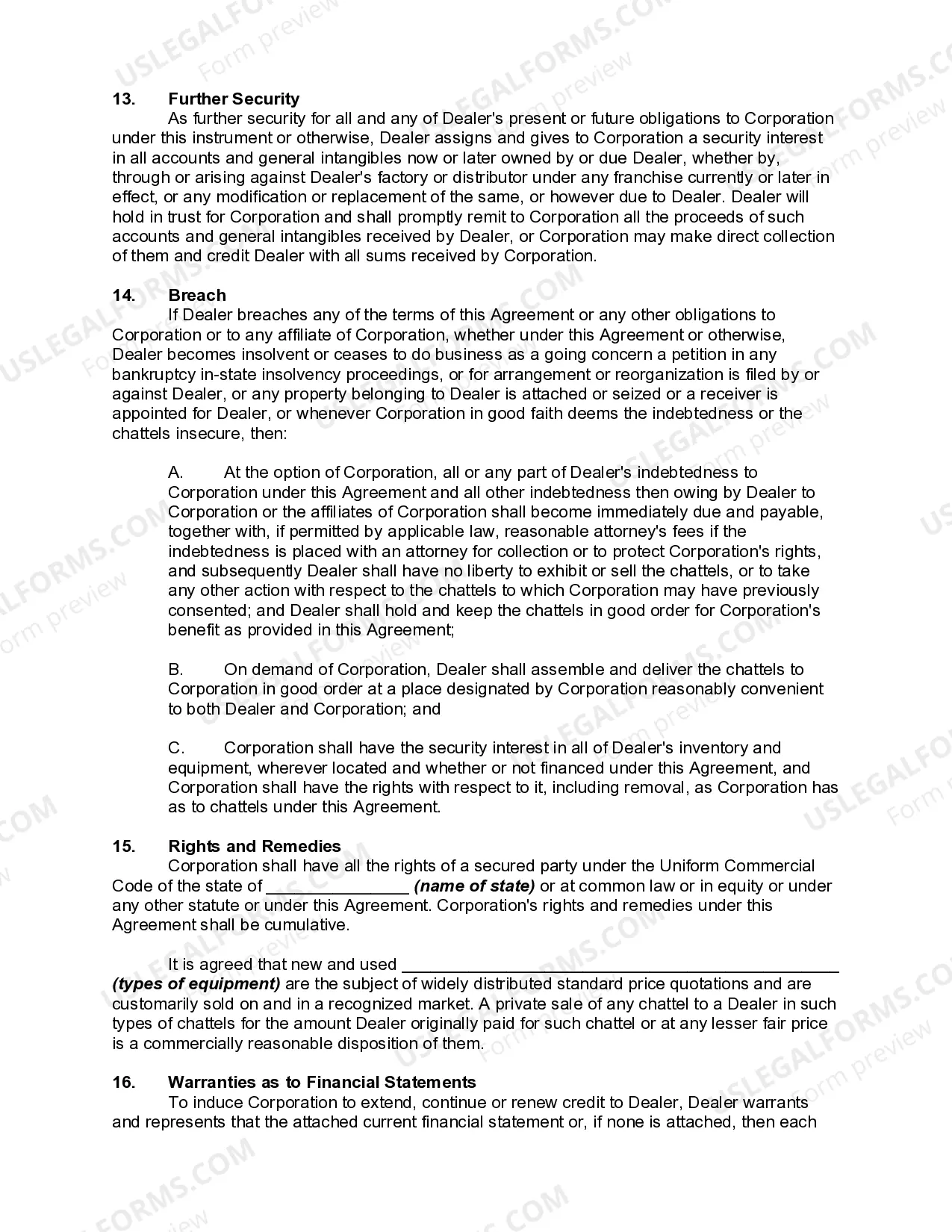

This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

A Minnesota Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legal contract that outlines the terms and conditions under which a credit corporation provides financing to a dealership for the purpose of purchasing inventory. This agreement is specifically applicable in the state of Minnesota and is designed to protect the interests of both the dealer and the credit corporation. It establishes a security interest in the accounts and general intangibles of the dealership, ensuring that the credit corporation has a legal claim on these assets in case of default or non-payment. Keywords: Minnesota, financing agreement, dealer, credit corporation, wholesale financing, security interest, accounts, general intangibles. Different types of Minnesota Financing Agreements between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles may include: 1. Retail Financing Agreement: This type of agreement is specific to financing arrangements between a dealer and credit corporation for retail sales. It covers terms related to customer financing, repayment schedules, and interest rates. 2. Floor Plan Financing Agreement: This agreement is designed for dealership financing related to inventory purchases. It outlines the terms under which the dealer can borrow funds from the credit corporation to acquire and hold inventory for sale. The agreement typically includes provisions for monthly interest payments and repayment upon the sale of each unit. 3. Promissory Note Financing Agreement: This agreement is a form of debt instrument where the dealer promises to repay the credit corporation a specific amount, plus interest, within a predetermined timeframe. It may include collateral, such as the dealership's accounts and general intangibles. 4. Revolving Line of Credit Agreement: This type of agreement provides the dealer with ongoing access to a predetermined credit limit. The dealer can borrow against this limit as needed, repaying and re-borrowing within the agreed terms set forth in the agreement. It offers flexibility and convenience for the dealer's financing needs. It is important for both the dealer and the credit corporation to carefully review and understand the terms of these agreements before signing. Seeking legal counsel is advised to ensure compliance with Minnesota state laws and to protect the interests of all parties involved.A Minnesota Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legal contract that outlines the terms and conditions under which a credit corporation provides financing to a dealership for the purpose of purchasing inventory. This agreement is specifically applicable in the state of Minnesota and is designed to protect the interests of both the dealer and the credit corporation. It establishes a security interest in the accounts and general intangibles of the dealership, ensuring that the credit corporation has a legal claim on these assets in case of default or non-payment. Keywords: Minnesota, financing agreement, dealer, credit corporation, wholesale financing, security interest, accounts, general intangibles. Different types of Minnesota Financing Agreements between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles may include: 1. Retail Financing Agreement: This type of agreement is specific to financing arrangements between a dealer and credit corporation for retail sales. It covers terms related to customer financing, repayment schedules, and interest rates. 2. Floor Plan Financing Agreement: This agreement is designed for dealership financing related to inventory purchases. It outlines the terms under which the dealer can borrow funds from the credit corporation to acquire and hold inventory for sale. The agreement typically includes provisions for monthly interest payments and repayment upon the sale of each unit. 3. Promissory Note Financing Agreement: This agreement is a form of debt instrument where the dealer promises to repay the credit corporation a specific amount, plus interest, within a predetermined timeframe. It may include collateral, such as the dealership's accounts and general intangibles. 4. Revolving Line of Credit Agreement: This type of agreement provides the dealer with ongoing access to a predetermined credit limit. The dealer can borrow against this limit as needed, repaying and re-borrowing within the agreed terms set forth in the agreement. It offers flexibility and convenience for the dealer's financing needs. It is important for both the dealer and the credit corporation to carefully review and understand the terms of these agreements before signing. Seeking legal counsel is advised to ensure compliance with Minnesota state laws and to protect the interests of all parties involved.