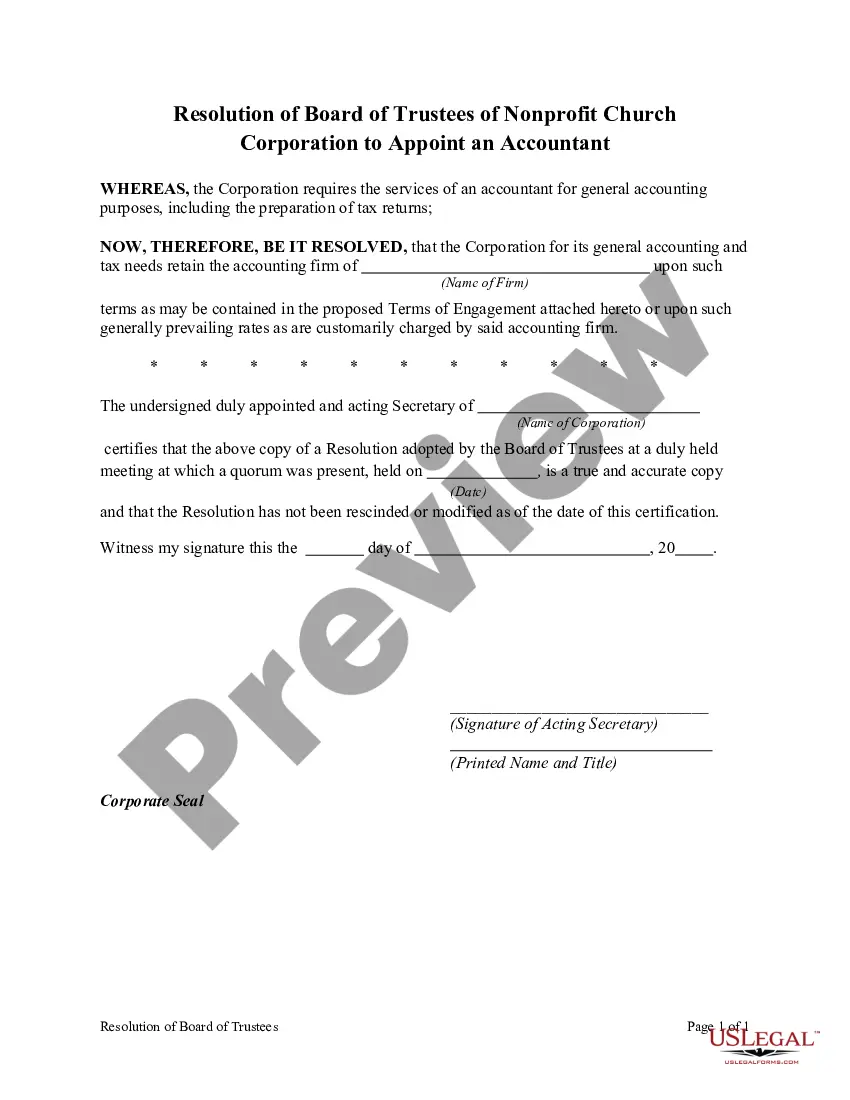

Nonprofit Church Corporate resolutions are generally formal actions and decisions of a corporation, approved by the Board of Trustees or Elders. They are formalized statements that have been voted upon and approved by the corporate trustees, typically authorizing a specific corporate action.

Title: Understanding the Minnesota Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant Introduction: The Minnesota Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant refers to a formal decision made by the board of trustees of a nonprofit church organization in Minnesota to appoint an accountant for financial management and oversight. This resolution plays a critical role in ensuring accurate financial reporting, compliance with legal requirements, and transparency within the organization. In this article, we will explore the significance of this resolution, outline its key components, and highlight different types of resolutions that can be adopted by the board of trustees. 1. Importance of the Resolution: The Minnesota Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant is crucial in upholding financial integrity within nonprofit church organizations. By appointing an accountant, the board of trustees takes proactive measures to manage the church's financial affairs, safeguarding the organization's reputation and the trust of its community members. 2. Key Components of the Resolution: A. Purpose Statement: The resolution should clearly state the purpose of appointing an accountant, such as ensuring accurate financial record-keeping, complying with tax regulations, conducting internal audits, or preparing necessary financial statements. B. Appointment Details: The resolution should specify the details of the accountant's appointment, including their qualifications, scope of responsibilities, term limits, and reporting lines within the organization. C. Reporting Requirements: The resolution may include provisions requiring the accountant to provide regular financial reports and updates to the board of trustees or its designated committee. D. Compliance and Ethical Considerations: The resolution should emphasize the importance of the accountant's adherence to relevant laws, regulations, and ethical standards to maintain the highest level of financial accountability and transparency. 3. Types of Minnesota Resolutions of Board of Trustees for Accountant Appointment: A. Annual Appointment Resolution: This type of resolution is used when the board of trustees wishes to appoint an accountant on an annual basis, ensuring periodic review and evaluation of the church's financial practices. B. Special Appointment Resolution: In certain situations, such as when financial irregularities or significant changes occur, the board may pass a special appointment resolution to appoint an accountant outside the regular appointment cycle. C. Committee Authorization Resolution: This resolution allows the board to delegate the authority to appoint an accountant to a specific committee formed from within its members, which then fulfills the role of selecting and overseeing the accountant's activities. Conclusion: The Minnesota Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant serves as a vital mechanism for nonprofit church organizations to ensure accurate financial management, compliance, and transparency. By adopting this resolution, the board of trustees fulfills its fiduciary duty to the organization and its stakeholders, guaranteeing efficient financial oversight and contributing to the long-term sustainability of the nonprofit church corporation.Title: Understanding the Minnesota Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant Introduction: The Minnesota Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant refers to a formal decision made by the board of trustees of a nonprofit church organization in Minnesota to appoint an accountant for financial management and oversight. This resolution plays a critical role in ensuring accurate financial reporting, compliance with legal requirements, and transparency within the organization. In this article, we will explore the significance of this resolution, outline its key components, and highlight different types of resolutions that can be adopted by the board of trustees. 1. Importance of the Resolution: The Minnesota Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant is crucial in upholding financial integrity within nonprofit church organizations. By appointing an accountant, the board of trustees takes proactive measures to manage the church's financial affairs, safeguarding the organization's reputation and the trust of its community members. 2. Key Components of the Resolution: A. Purpose Statement: The resolution should clearly state the purpose of appointing an accountant, such as ensuring accurate financial record-keeping, complying with tax regulations, conducting internal audits, or preparing necessary financial statements. B. Appointment Details: The resolution should specify the details of the accountant's appointment, including their qualifications, scope of responsibilities, term limits, and reporting lines within the organization. C. Reporting Requirements: The resolution may include provisions requiring the accountant to provide regular financial reports and updates to the board of trustees or its designated committee. D. Compliance and Ethical Considerations: The resolution should emphasize the importance of the accountant's adherence to relevant laws, regulations, and ethical standards to maintain the highest level of financial accountability and transparency. 3. Types of Minnesota Resolutions of Board of Trustees for Accountant Appointment: A. Annual Appointment Resolution: This type of resolution is used when the board of trustees wishes to appoint an accountant on an annual basis, ensuring periodic review and evaluation of the church's financial practices. B. Special Appointment Resolution: In certain situations, such as when financial irregularities or significant changes occur, the board may pass a special appointment resolution to appoint an accountant outside the regular appointment cycle. C. Committee Authorization Resolution: This resolution allows the board to delegate the authority to appoint an accountant to a specific committee formed from within its members, which then fulfills the role of selecting and overseeing the accountant's activities. Conclusion: The Minnesota Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant serves as a vital mechanism for nonprofit church organizations to ensure accurate financial management, compliance, and transparency. By adopting this resolution, the board of trustees fulfills its fiduciary duty to the organization and its stakeholders, guaranteeing efficient financial oversight and contributing to the long-term sustainability of the nonprofit church corporation.