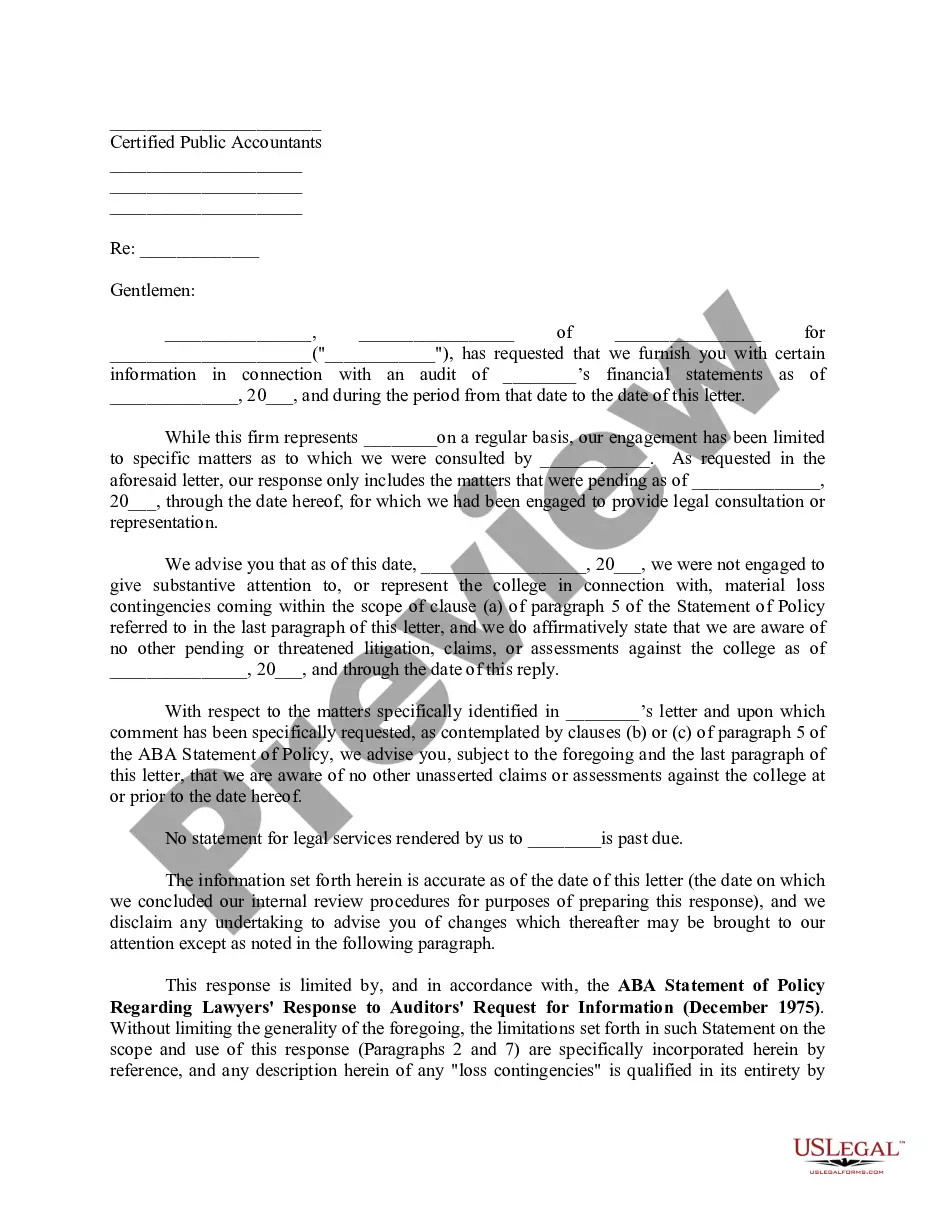

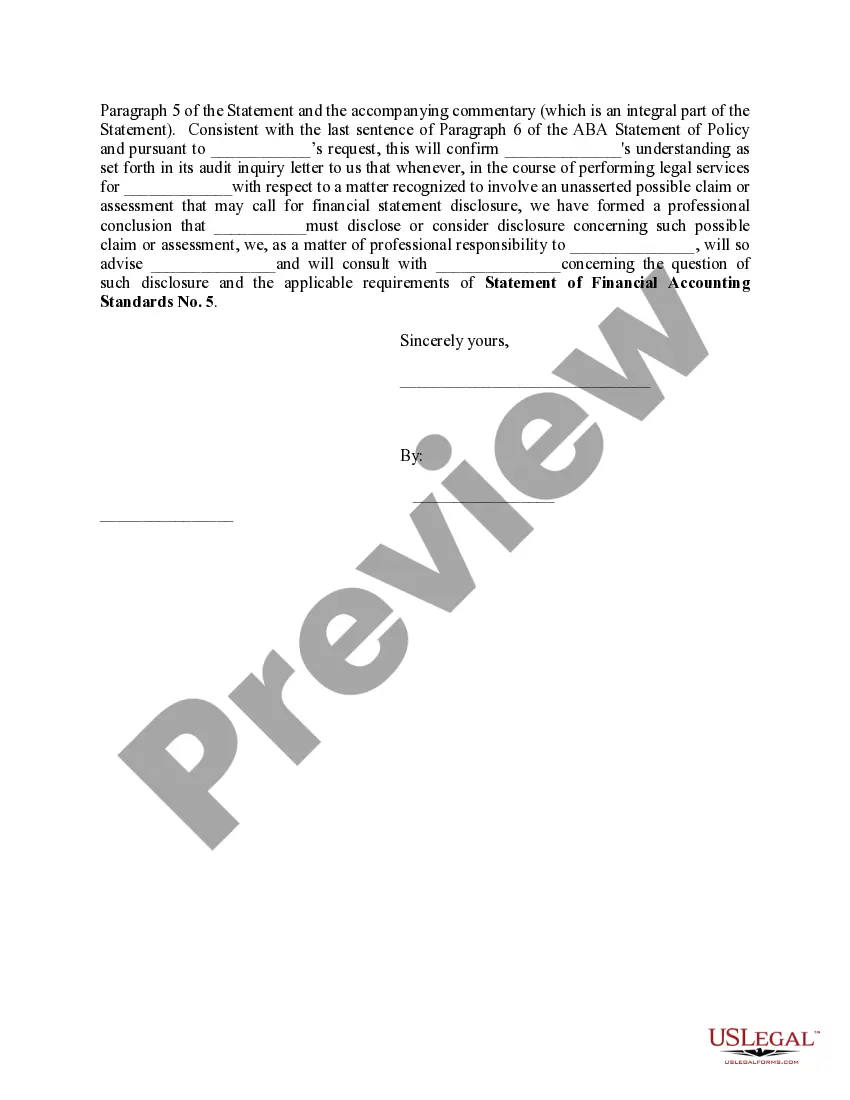

The Minnesota Model Letter Accountants To Auditors is a standardized communication tool widely used in the accounting industry. This letter acts as a formal means of transferring financial information between accountants and auditors, ensuring proper documentation and understanding of key financial aspects. The purpose of this letter is to summarize financial reports, disclose any significant changes, and provide relevant information to auditors for conducting an audit. By following the Minnesota Model, accountants can effectively communicate the required data to auditors, enabling them to perform their audit procedures efficiently and accurately. There are different types of Minnesota Model Letters Accountants To Auditors, each catering to specific financial scenarios and reporting needs. Some common types include: 1. Annual Financial Statements Letter: This letter is usually sent annually to auditors and summarizes the financial performance of an organization during a specific period, typically the fiscal year. It includes crucial information such as balance sheets, income statements, cash flow statements, and accompanying notes. 2. Quarterly Financial Statements Letter: Organizations may also send quarterly letters to auditors, allowing for timely analysis of financial performance and identification of any emerging trends or concerns. These letters usually include condensed financial statements and additional notes highlighting key changes since the previous quarter. 3. Management Discussion and Analysis Letter: In some cases, accountants may provide auditors with a detailed management discussion and analysis (MDA) letter. This type of letter offers a comprehensive analysis of financial performance, significant changes, and anticipated future developments, providing auditors with a holistic view of the organization's financial standing. 4. Significant Accounting Policies and Procedures Letter: As part of their financial reporting responsibilities, accountants may include a letter detailing the significant accounting policies and procedures implemented by the organization. This letter helps auditors understand the accounting methods, valuations, and estimates used in preparing financial statements. Regardless of the specific type of Minnesota Model Letter used, it is crucial to ensure accuracy, clarity, and transparency in communicating financial information. Accountants must diligently compile and present reliable data, abiding by relevant accounting standards and regulations. By adhering to the Minnesota Model Letter Accountants To Auditors, organizations promote effective collaboration between accounting and auditing professionals, enhancing the overall quality and reliability of financial reporting.

Minnesota Model Letter Accountants To Auditors

Description

How to fill out Minnesota Model Letter Accountants To Auditors?

Are you in a position the place you need documents for sometimes enterprise or specific reasons almost every day? There are a variety of authorized document templates available online, but discovering types you can rely is not straightforward. US Legal Forms gives a huge number of kind templates, such as the Minnesota Model Letter Accountants To Auditors, that happen to be written to meet state and federal demands.

If you are previously familiar with US Legal Forms website and possess an account, basically log in. Following that, you may download the Minnesota Model Letter Accountants To Auditors format.

If you do not provide an bank account and would like to start using US Legal Forms, abide by these steps:

- Obtain the kind you will need and ensure it is for your correct area/region.

- Take advantage of the Preview button to check the shape.

- Read the information to ensure that you have chosen the proper kind.

- In case the kind is not what you are searching for, utilize the Look for industry to discover the kind that meets your needs and demands.

- When you get the correct kind, just click Get now.

- Pick the prices strategy you want, fill out the necessary info to make your bank account, and buy the transaction with your PayPal or charge card.

- Select a handy data file format and download your version.

Locate all of the document templates you possess bought in the My Forms food selection. You can get a further version of Minnesota Model Letter Accountants To Auditors at any time, if needed. Just click the essential kind to download or produce the document format.

Use US Legal Forms, the most comprehensive collection of authorized types, in order to save time and stay away from blunders. The support gives professionally made authorized document templates that can be used for an array of reasons. Produce an account on US Legal Forms and start producing your way of life easier.