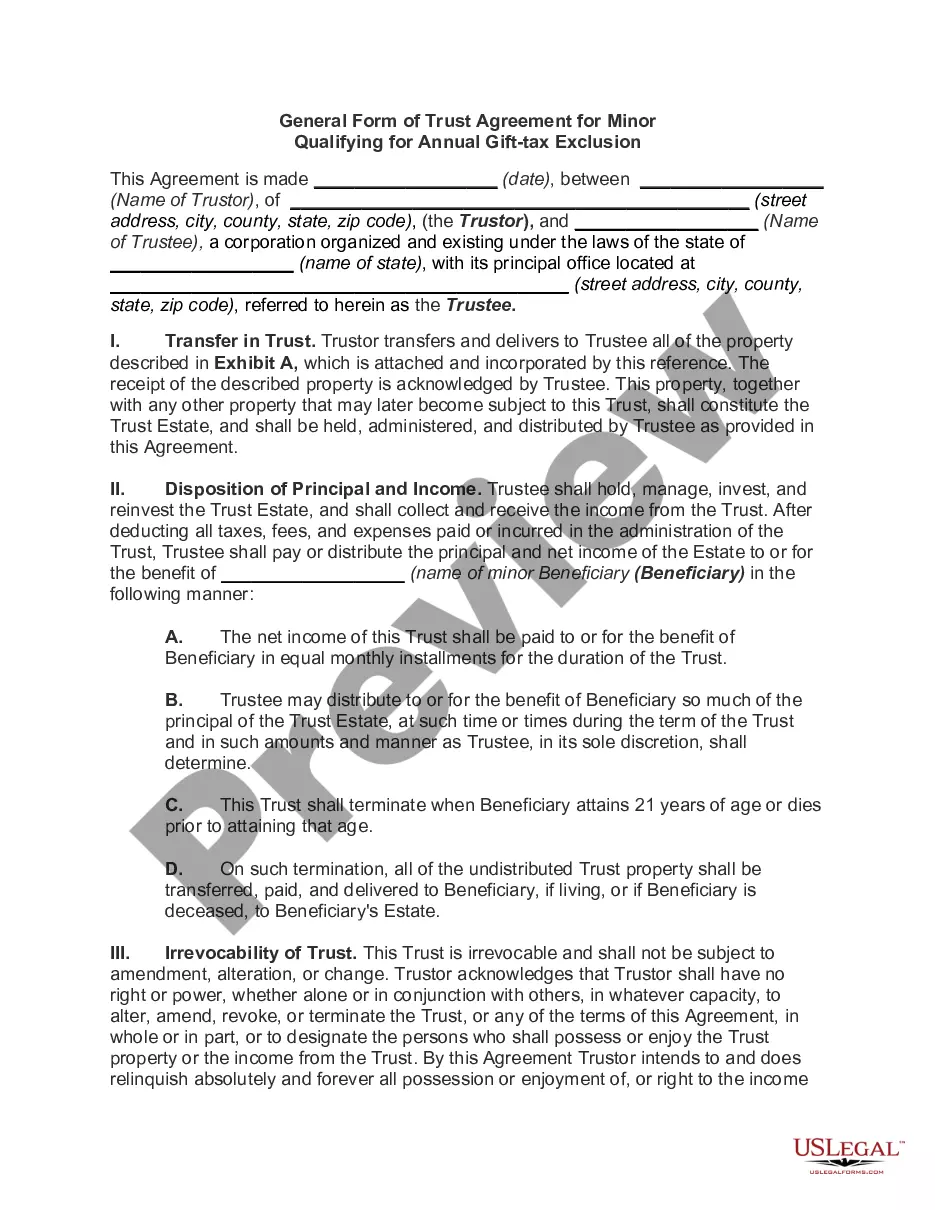

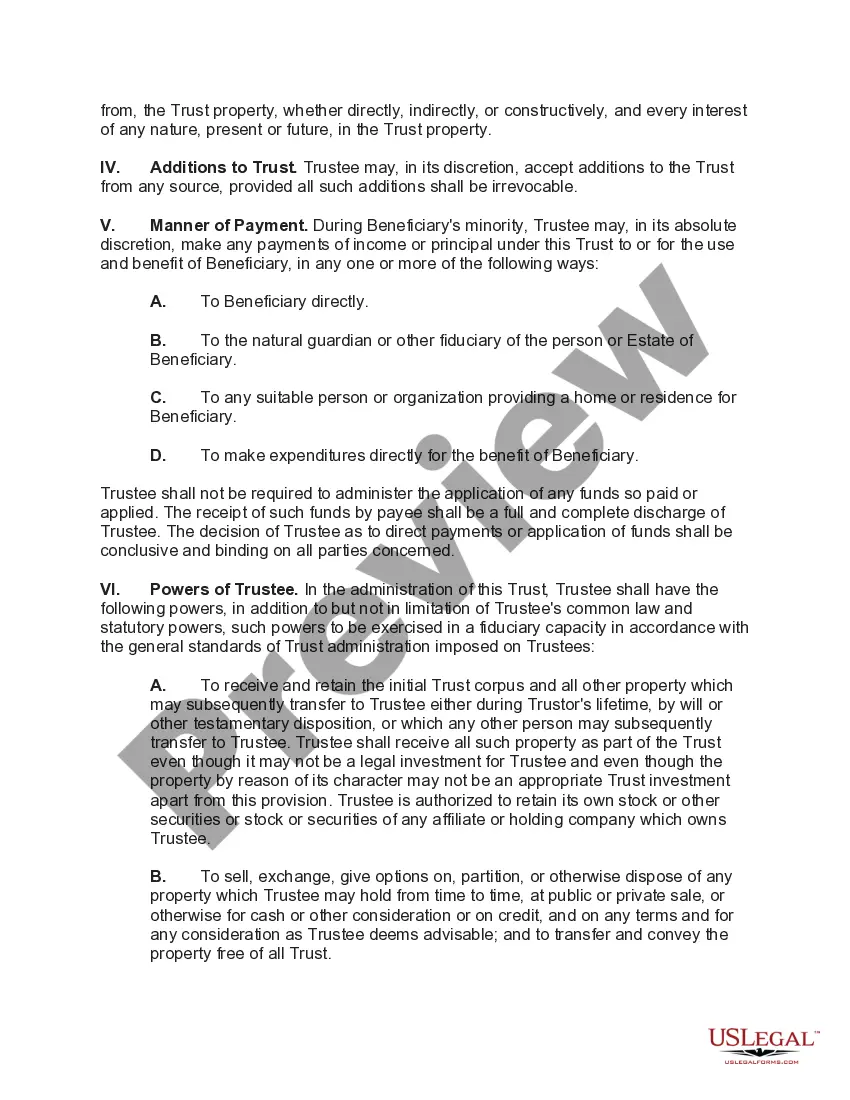

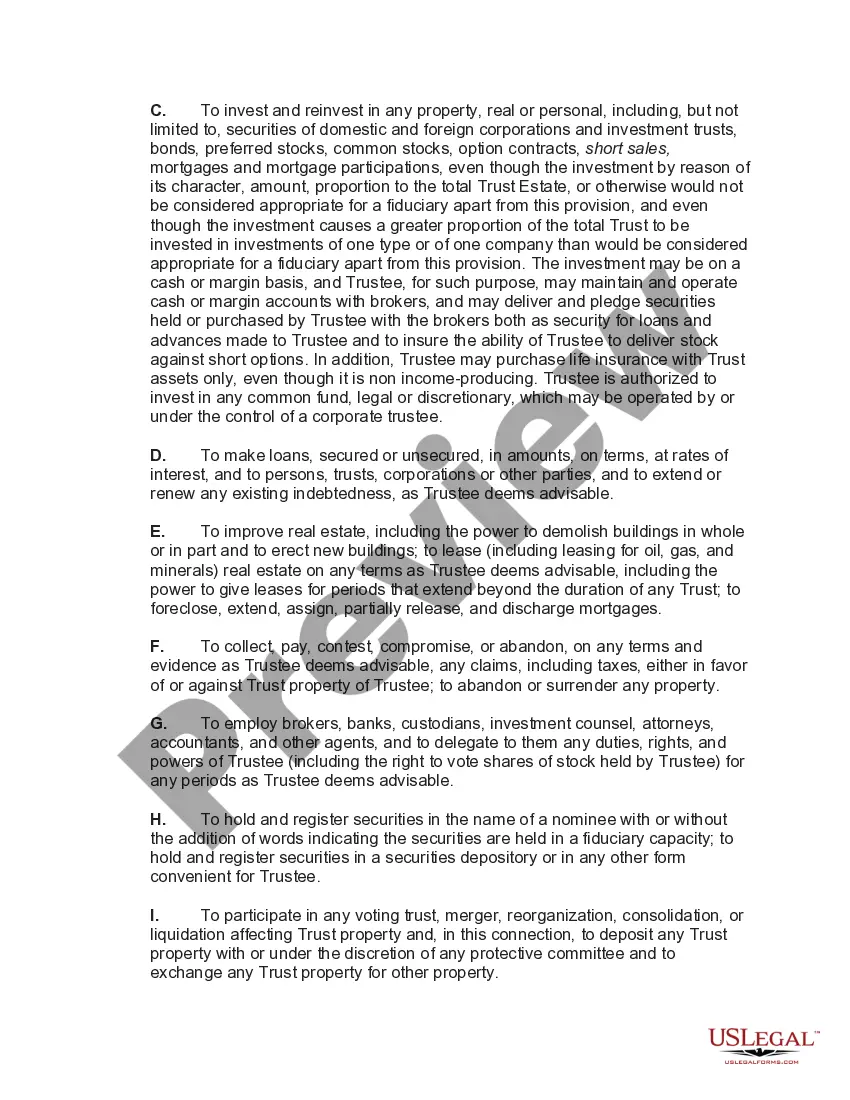

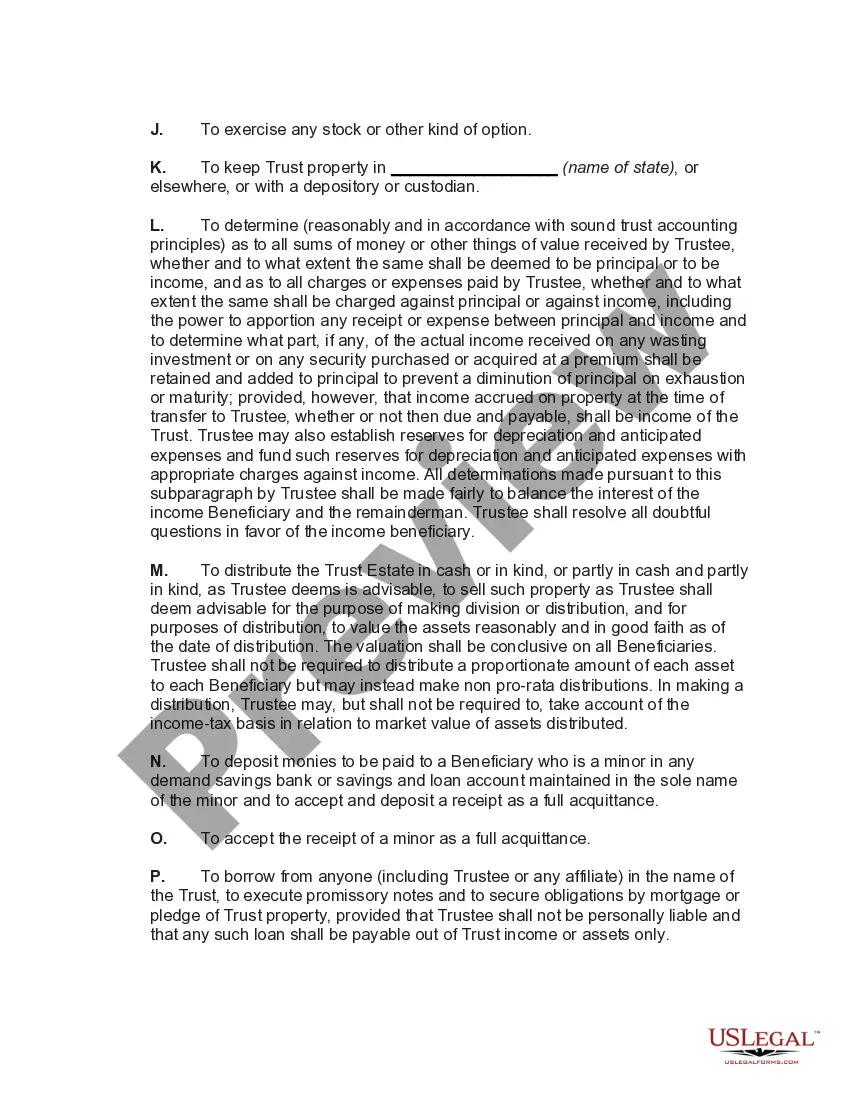

The Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion is a legal document designed to establish a trust for minors in accordance with the requirements for qualifying for the annual gift tax exclusion. This type of trust allows individuals to make gifts to minors without incurring any gift tax liability, as long as certain conditions are met. The purpose of this trust agreement is to ensure that the gifted assets are managed and preserved until the minor reaches a certain age or achieves specific milestones as stipulated in the trust document. During this period, the designated trustee is responsible for overseeing and managing the assets in the best interests of the minor beneficiary. The Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion requires several key elements to be included. Firstly, the agreement must clearly establish the donor's intent to create a trust for the minor beneficiary. It should also outline the specific assets being transferred into the trust as gifts. Additionally, the trust agreement should clearly state the conditions and terms under which the assets will be distributed to the minor. These conditions may include reaching a certain age, completing specific education goals, or achieving financial independence. The agreement should also mention any limitations or restrictions on the use of trust assets until the conditions are met. Furthermore, it is essential to name a suitable trustee in the trust agreement. The trustee is responsible for managing the assets, making investment decisions, and distributing funds or other assets to the minor beneficiary as outlined in the agreement. The trustee must act in the best interest of the minor and adhere to the terms and guidelines specified in the trust document. There may be different variations or types of Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion, depending on specific circumstances or needs. Some variants may focus on educational purposes, where the assets in the trust are primarily intended to be used for financing the beneficiary's education. Others may have specific age-related conditions, such as distributing a portion of the assets when the beneficiary turns 18 and the remaining balance upon reaching 25 years of age. In conclusion, the Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion is a legal document that enables individuals to create a trust for gifting assets to minors while benefiting from the annual gift tax exclusion. This trust agreement outlines the terms, conditions, and limitations for managing the gifted assets until the minor beneficiary meets certain criteria. Seek professional legal advice to ensure compliance with Minnesota state laws and individual circumstances when using this form.

Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion

Description

How to fill out Minnesota General Form Of Trust Agreement For Minor Qualifying For Annual Gift Tax Exclusion?

If you wish to total, obtain, or print out authorized record themes, use US Legal Forms, the largest variety of authorized varieties, which can be found on-line. Make use of the site`s basic and practical look for to find the documents you will need. Numerous themes for company and individual purposes are sorted by categories and suggests, or keywords and phrases. Use US Legal Forms to find the Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion within a few click throughs.

In case you are previously a US Legal Forms customer, log in to the account and click the Down load option to have the Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion. You can also access varieties you formerly saved in the My Forms tab of your account.

Should you use US Legal Forms for the first time, follow the instructions listed below:

- Step 1. Make sure you have selected the shape for your right city/country.

- Step 2. Take advantage of the Review option to examine the form`s content. Don`t forget about to read the explanation.

- Step 3. In case you are not happy together with the form, take advantage of the Look for industry at the top of the display screen to get other models of the authorized form web template.

- Step 4. Upon having discovered the shape you will need, click on the Purchase now option. Choose the prices program you favor and add your accreditations to sign up for the account.

- Step 5. Process the purchase. You can use your bank card or PayPal account to complete the purchase.

- Step 6. Choose the file format of the authorized form and obtain it on the system.

- Step 7. Full, modify and print out or indication the Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion.

Each and every authorized record web template you buy is yours eternally. You possess acces to each and every form you saved in your acccount. Go through the My Forms portion and pick a form to print out or obtain once more.

Remain competitive and obtain, and print out the Minnesota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion with US Legal Forms. There are millions of expert and condition-certain varieties you may use to your company or individual demands.