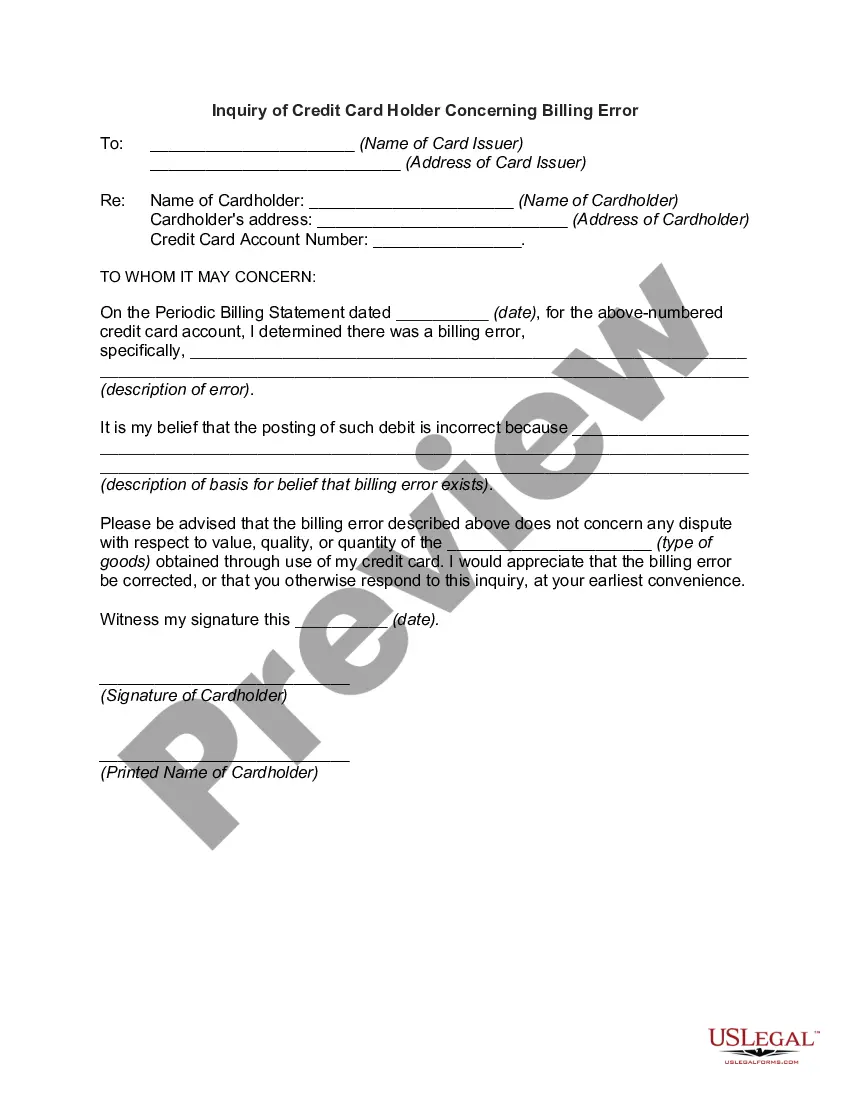

Title: Understanding Minnesota Inquiry of Credit Cardholder Concerning Billing Error: Types and Detailed Description Introduction: In Minnesota, consumers are protected by laws and regulations that allow credit cardholders to inquire about and challenge billing errors. This process, known as the Minnesota Inquiry of Credit Cardholder Concerning Billing Error, ensures fair billing practices and promotes customer confidence in their financial transactions. This article will provide a comprehensive overview of what the inquiry entails, its purpose, and the different types of inquiries that can be made. Keywords: — Minnesota Inquiry of Credit Cardholder Concerning Billing Error — credit cardholder right— - Minnesota credit card billing error — fair billing practice— - credit card billing dispute — credit card billindiscrepancync— - credit card billing statement Types of Minnesota Inquiry of Credit Cardholder Concerning Billing Error: 1. Unauthorized transactions: This type of inquiry occurs when a credit cardholder notices charges on their billing statement that they did not authorize or make. It may involve fraudulent activities, such as identity theft or unauthorized use of the credit card. 2. Incorrect amounts: This type of inquiry arises when a credit cardholder believes there is an error in the amount charged on their billing statement. It may include overcharges, undercharges, or discrepancies in pricing, currency conversion, or fees. 3. Goods or services not received: This type of inquiry occurs when a credit cardholder paid for goods or services but did not receive them as agreed upon. It may involve instances where the merchant fails to deliver the promised products, issues defective goods, or renders substandard services. 4. Duplicate charges: This type of inquiry arises when a credit cardholder notices repeated charges for the same transaction on their credit card statement. It may be due to technical errors, merchant mishaps, or delayed processing. Detailed Description: The Minnesota Inquiry of Credit Cardholder Concerning Billing Error provides credit cardholders with the right to dispute errors on their credit card bills. When a billing error is detected, it is crucial for the cardholder to take prompt action to protect their rights and resolve the matter. The following steps should be followed: 1. Review the billing statement: Carefully examine the credit card statement, noting any discrepancies, unauthorized transactions, incorrect amounts, or goods/services not received. 2. Gather evidence: Collect all supporting documentation related to the disputed transaction(s), such as receipts, order confirmations, emails, or any relevant communication with merchants. 3. Contact the credit card issuer: Notify the credit card issuer promptly, preferably in writing, clearly explaining the nature of the billing error and providing all relevant information and evidence. Include copies of supporting documents to strengthen the case. 4. Credit card issuer's investigation: The credit card issuer is obligated to investigate the dispute within a specific timeframe (usually 30 days) and provide a written response acknowledging the inquiry. During the investigation, the issuer may contact the merchant or request additional information from the cardholder. 5. Resolution and corrective action: Upon completion of the investigation, the credit card issuer will inform the cardholder of the findings. If an error is confirmed, the cardholder may receive a credit for the disputed amount on their next statement. If no error is found, the issuer will provide an explanation for their decision. Conclusion: The Minnesota Inquiry of Credit Cardholder Concerning Billing Error offers protection and recourse to credit cardholders who suspect errors in their billing statements. By understanding the different types of inquiries and following the appropriate steps, consumers can actively rectify billing errors, ensure fair billing practices, and safeguard their financial interests.

Minnesota Inquiry of Credit Cardholder Concerning Billing Error

Description

How to fill out Minnesota Inquiry Of Credit Cardholder Concerning Billing Error?

US Legal Forms - one of the greatest libraries of legal varieties in the States - delivers an array of legal file themes you are able to obtain or printing. Utilizing the internet site, you can get 1000s of varieties for organization and person uses, sorted by groups, suggests, or keywords and phrases.You can find the newest versions of varieties just like the Minnesota Inquiry of Credit Cardholder Concerning Billing Error in seconds.

If you currently have a registration, log in and obtain Minnesota Inquiry of Credit Cardholder Concerning Billing Error in the US Legal Forms collection. The Down load switch will show up on every kind you see. You have accessibility to all in the past delivered electronically varieties within the My Forms tab of the bank account.

If you want to use US Legal Forms the very first time, here are simple recommendations to help you began:

- Ensure you have selected the right kind to your city/area. Click on the Preview switch to analyze the form`s content. Read the kind information to ensure that you have chosen the appropriate kind.

- In the event the kind doesn`t fit your specifications, take advantage of the Research discipline towards the top of the monitor to obtain the one who does.

- If you are happy with the shape, confirm your option by simply clicking the Purchase now switch. Then, opt for the rates plan you prefer and supply your accreditations to register on an bank account.

- Process the purchase. Use your bank card or PayPal bank account to finish the purchase.

- Pick the structure and obtain the shape on your device.

- Make modifications. Complete, modify and printing and indicator the delivered electronically Minnesota Inquiry of Credit Cardholder Concerning Billing Error.

Each template you put into your account lacks an expiration time and it is your own for a long time. So, if you wish to obtain or printing another version, just go to the My Forms segment and click on on the kind you want.

Gain access to the Minnesota Inquiry of Credit Cardholder Concerning Billing Error with US Legal Forms, the most comprehensive collection of legal file themes. Use 1000s of specialist and state-particular themes that meet your organization or person requires and specifications.

Form popularity

FAQ

Section 1026.13(c)(2) requires creditors to investigate the dispute, correct any errors found, and notify the consumer of the outcome no later than two complete billing cycles or 90 days after receiving the billing error notice.

If you believe an error has been made on your credit card bill, you should send your credit card company a written letter within 60 days of the charge appearing on your billing statement. The letter should include information that identifies yourself and what you are disputing.

Federal law only protects cardholders for a limited time 60 days to be exact after a fraudulent or incorrect charge has been made. Thankfully I noticed the billing error within a few days of it posting to my account and started the dispute process right away.

How to Dispute a Billing ErrorRespond quickly. You have 60 days from the time the billing statement is sent to request a correction, so act quickly.Your request needs to be in writing.Then you wait.Don't withhold payment!Cover yourself.

Before you get yourself involved in a lengthy formal dispute, speak with the merchant. Bring your receipt and credit card statement, and take the time to explain the discrepancy. The merchant may clear up the mistake without having to involve the credit card company. If not, take your complaint to the next level.

If you believe an error has been made on your credit card bill, you should send your credit card company a written letter within 60 days of the charge appearing on your billing statement. The letter should include information that identifies yourself and what you are disputing.

If you believe an error has been made on your credit card bill, you should send your credit card company a written letter within 60 days of the charge appearing on your billing statement. The letter should include information that identifies yourself and what you are disputing.

If you have an issue with your credit card or bank account, report it to the Consumer Financial Protection Bureau. Go to consumerfinance.gov/complaint or call (855) 411-CFPB (2372).

How to Dispute a Billing ErrorRespond quickly. You have 60 days from the time the billing statement is sent to request a correction, so act quickly.Your request needs to be in writing.Then you wait.Don't withhold payment!Cover yourself.25-Oct-2015