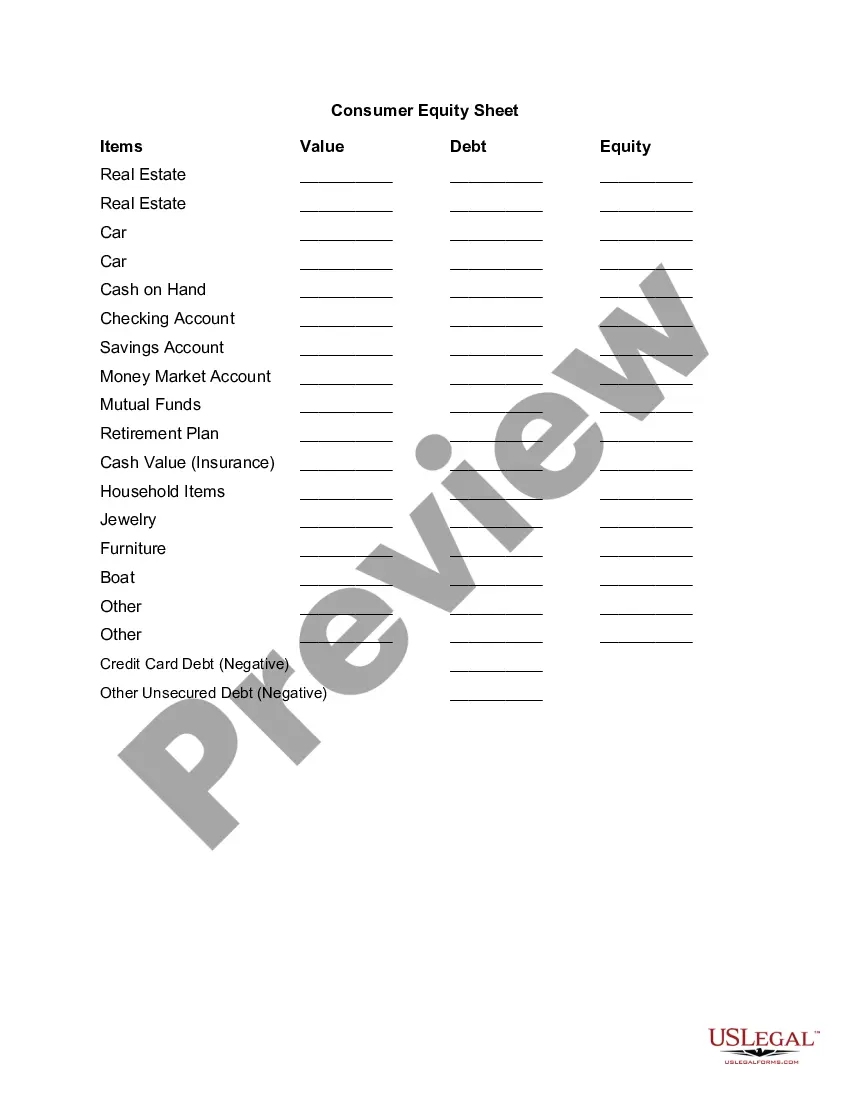

The Minnesota Consumer Equity Sheet is a crucial document that provides a comprehensive overview of a consumer's financial standing and helps evaluate their equity status. It serves as an essential tool for individuals in Minnesota to gain insights into their financial health and make informed decisions about various aspects of their finances. The Minnesota Consumer Equity Sheet is designed to cover multiple facets of a consumer's financial life. It includes a detailed breakdown of assets, liabilities, income, and expenses. By analyzing these components, individuals can gain a clear understanding of their net worth and overall equity position. The document consists of various sections, each focusing on specific areas of financial information. Some key components include: 1. Assets: This section presents a comprehensive list of assets owned by the consumer, such as cash, bank accounts, investments, real estate, vehicles, and other valuable possessions. Each asset is assigned a monetary value, contributing to the overall net worth calculation. 2. Liabilities: Here, all existing debts and financial obligations are showcased. This can include mortgages, loans, credit card debt, student loans, and any other outstanding liabilities. Each liability is accompanied by details about the remaining balance, interest rates, and fixed payment amounts. 3. Income: This section provides a summary of the consumer's income sources, such as employment, business profits, investments, rental income, and any other means of revenue generation. It outlines the stability and consistency of income and helps assess the financial capacity to meet obligations and save for the future. 4. Expenses: Detailed information about the consumer's monthly expenses is noted in this section. It covers a wide range of categories including housing costs, utilities, transportation, groceries, healthcare, entertainment, and discretionary spending. By comparing income and expenses, individuals can determine their ability to manage their financial responsibilities effectively. By thoroughly examining the Minnesota Consumer Equity Sheet, consumers can assess their financial well-being, identify areas of improvement, and make informed decisions about their financial future. It aids in understanding the current equity position and potential for growth. It is essential to regularly update the equity sheet to accurately reflect changing financial circumstances. Although there may not be different types of Minnesota Consumer Equity Sheets, individuals can customize the sheet to meet their specific needs. This customization might involve adding additional sections or tailored categories based on the consumer's unique financial situation.

Minnesota Consumer Equity Sheet

Description

How to fill out Minnesota Consumer Equity Sheet?

US Legal Forms - one of several largest libraries of lawful varieties in the United States - offers a wide range of lawful papers web templates it is possible to acquire or printing. While using website, you can get 1000s of varieties for organization and specific reasons, categorized by classes, says, or key phrases.You will discover the latest models of varieties such as the Minnesota Consumer Equity Sheet within minutes.

If you currently have a monthly subscription, log in and acquire Minnesota Consumer Equity Sheet from the US Legal Forms local library. The Download button will show up on every single type you perspective. You get access to all previously acquired varieties in the My Forms tab of the bank account.

In order to use US Legal Forms the first time, allow me to share straightforward directions to help you began:

- Make sure you have picked out the right type for your personal metropolis/state. Click the Preview button to review the form`s articles. See the type information to actually have selected the right type.

- In case the type doesn`t suit your needs, use the Lookup area on top of the monitor to find the one which does.

- When you are satisfied with the form, affirm your decision by clicking the Get now button. Then, select the pricing plan you favor and provide your references to register on an bank account.

- Process the financial transaction. Utilize your credit card or PayPal bank account to finish the financial transaction.

- Find the format and acquire the form on your own device.

- Make adjustments. Fill out, edit and printing and indicator the acquired Minnesota Consumer Equity Sheet.

Each and every web template you included in your account lacks an expiration time which is the one you have eternally. So, if you wish to acquire or printing an additional duplicate, just check out the My Forms segment and then click in the type you want.

Get access to the Minnesota Consumer Equity Sheet with US Legal Forms, the most comprehensive local library of lawful papers web templates. Use 1000s of professional and status-particular web templates that fulfill your business or specific demands and needs.