The Minnesota Certificate of Borrower is a vital document associated with commercial loans in the state of Minnesota. It serves as formal recognition from the borrower to the lender, affirming their understanding and acceptance of the terms and conditions of the loan agreement. This certificate serves to protect the lender's interests and provides additional security for the loan. The Minnesota Certificate of Borrower typically includes specific information such as the borrower's legal name, address, and contact details. It also outlines the details of the loan, including the loan amount, interest rate, repayment terms, and any fees or charges involved. The certificate will often specify the purpose of the loan, whether it's for business expansion, equipment purchase, or working capital. This document demonstrates the borrower's compliance with the lender's requirements and represents a commitment to fulfill their obligations. By signing the Minnesota Certificate of Borrower, the borrower acknowledges that they have read, understood, and agreed to all terms outlined in the loan agreement. This helps establish a level of trust between both parties and provides a platform for successful business dealings. There are various types of Minnesota Certificates of Borrower regarding Commercial Loans, tailored to specific loan scenarios. These may include: 1. Minnesota Certificate of Borrower for Commercial Real Estate Loans: This certificate pertains to loans specifically associated with real estate transactions, such as purchasing or refinancing commercial properties. 2. Minnesota Certificate of Borrower for Equipment Financing: This type of certificate is relevant when the loan is intended for the acquisition or leasing of equipment required for business operations, such as machinery, vehicles, or technology systems. 3. Minnesota Certificate of Borrower for Lines of Credit: In cases where the loan involves a revolving line of credit, this certificate confirms the borrower's commitment to maintaining the agreed-upon credit limit and managing their usage responsibly. 4. Minnesota Certificate of Borrower for Small Business Administration (SBA) Loans: SBA loans are government-backed loans designed to support small businesses. This certificate ensures compliance with SBA requirements and reflects the borrower's understanding of the unique aspects associated with these loan programs. It is important for borrowers in Minnesota to carefully review and understand the terms and conditions specified in the loan agreement before signing the certificate. Seeking professional legal advice can be beneficial to guarantee complete comprehension and ensure compliance with all legal obligations.

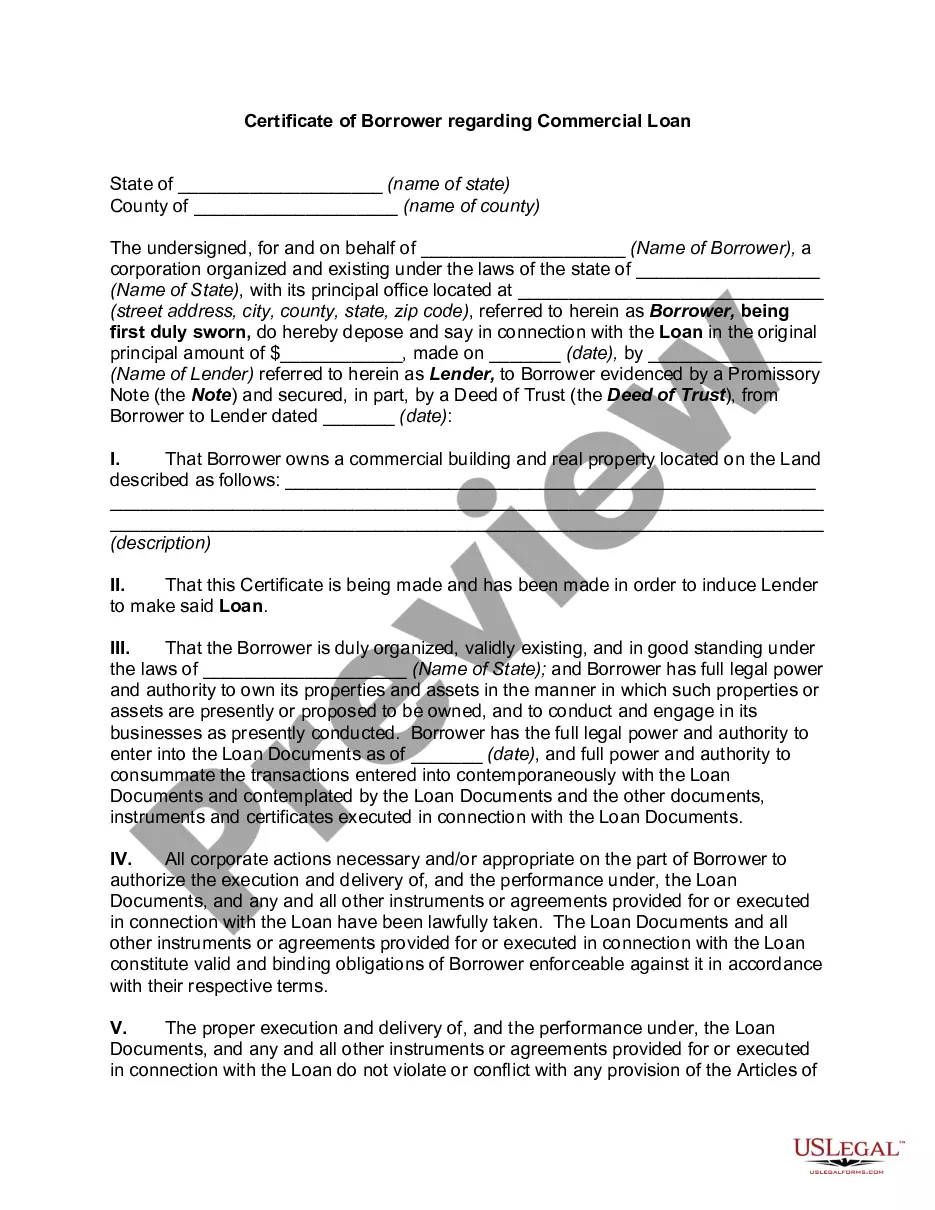

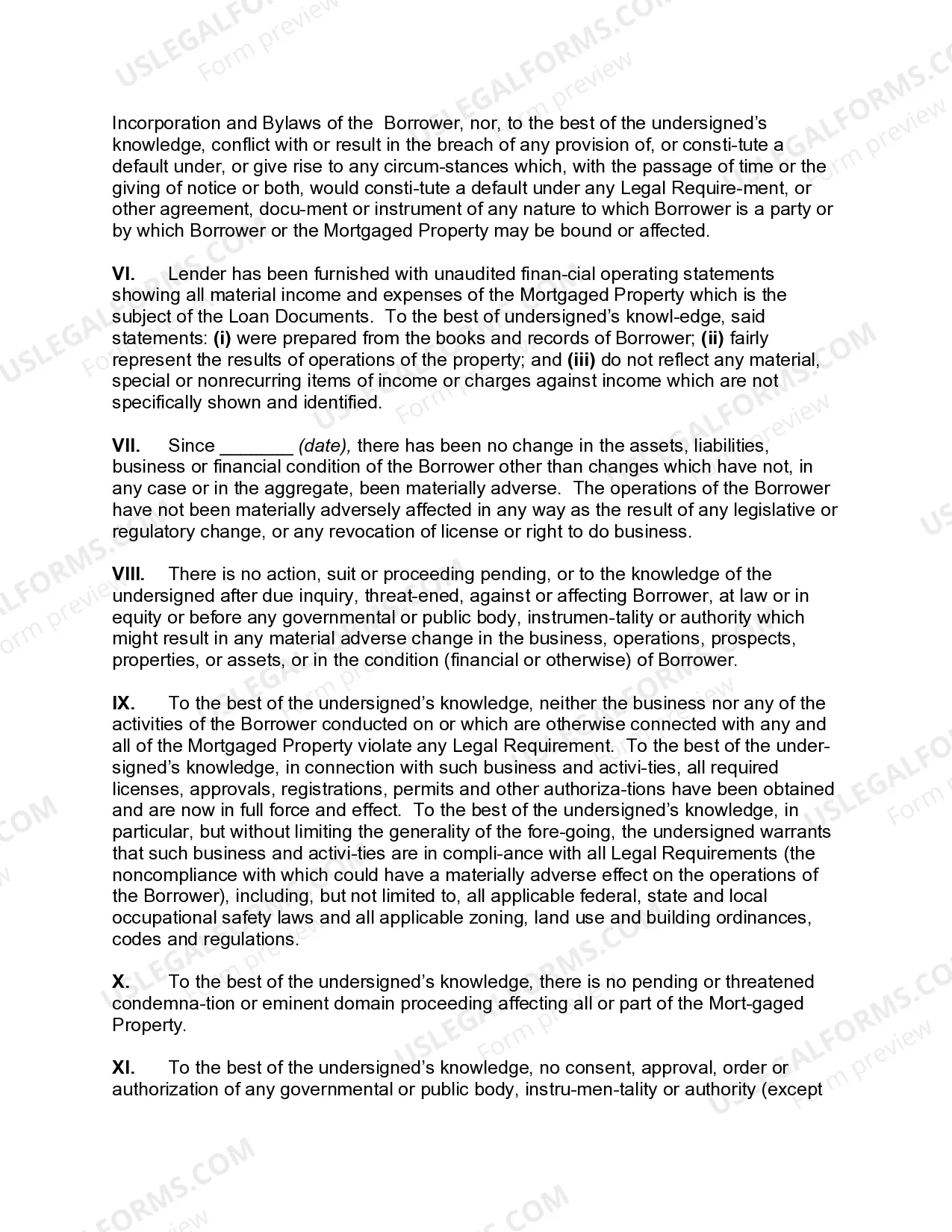

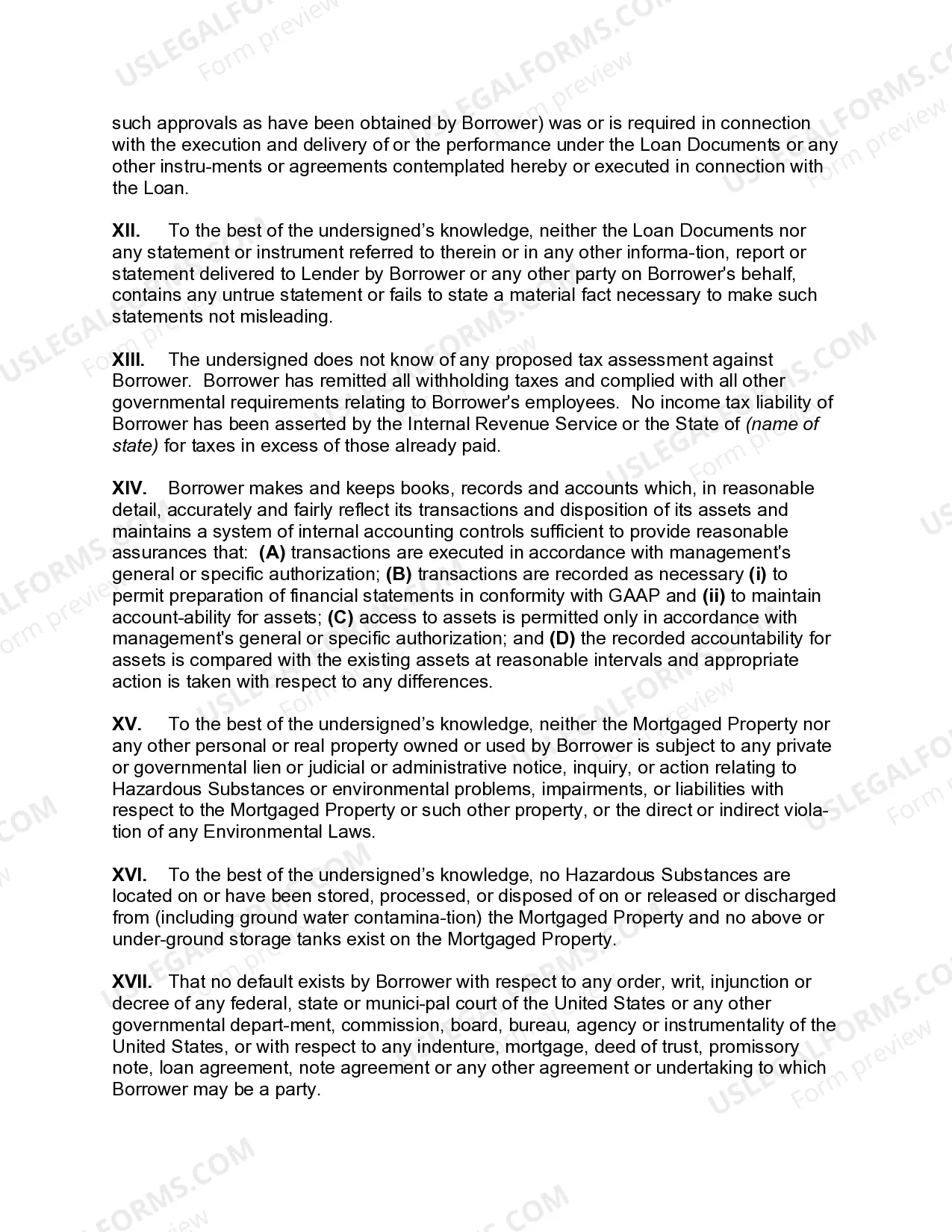

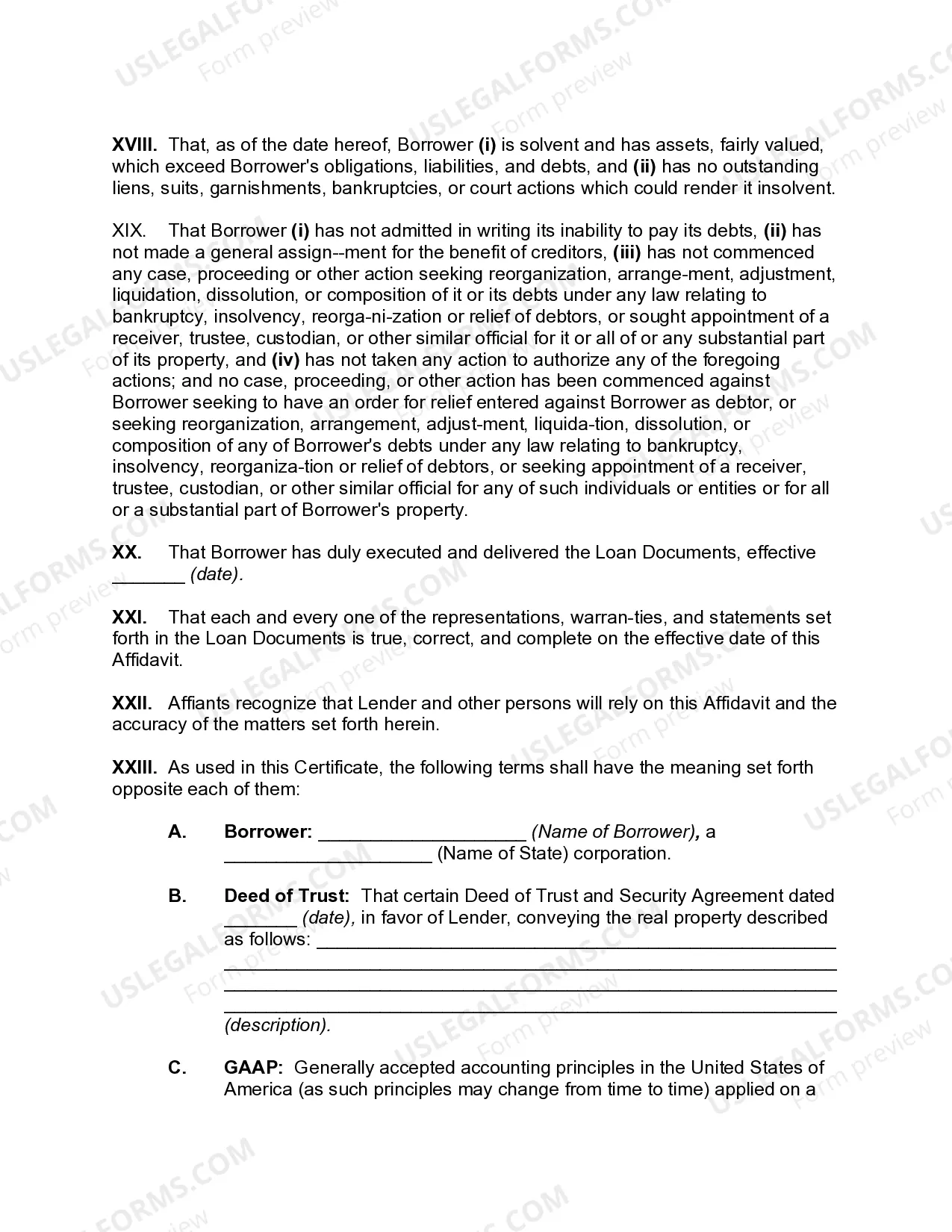

Minnesota Certificate of Borrower regarding Commercial Loan

Description

How to fill out Minnesota Certificate Of Borrower Regarding Commercial Loan?

US Legal Forms - one of the most significant libraries of authorized forms in the USA - offers a wide array of authorized record themes you may obtain or print out. Utilizing the internet site, you will get thousands of forms for enterprise and personal purposes, categorized by groups, states, or key phrases.You can find the newest variations of forms just like the Minnesota Certificate of Borrower regarding Commercial Loan within minutes.

If you have a membership, log in and obtain Minnesota Certificate of Borrower regarding Commercial Loan from your US Legal Forms catalogue. The Acquire option will show up on each and every type you see. You have access to all in the past acquired forms within the My Forms tab of your own bank account.

In order to use US Legal Forms initially, here are straightforward instructions to help you started off:

- Ensure you have picked out the right type for your personal city/county. Click the Review option to review the form`s information. Look at the type description to actually have selected the proper type.

- In the event the type doesn`t fit your demands, make use of the Look for industry towards the top of the display screen to find the one which does.

- If you are pleased with the form, affirm your choice by simply clicking the Buy now option. Then, opt for the prices prepare you like and provide your credentials to register for an bank account.

- Method the financial transaction. Utilize your Visa or Mastercard or PayPal bank account to complete the financial transaction.

- Select the formatting and obtain the form on the device.

- Make alterations. Complete, edit and print out and signal the acquired Minnesota Certificate of Borrower regarding Commercial Loan.

Every single format you included in your account lacks an expiry time and is your own permanently. So, if you would like obtain or print out yet another duplicate, just proceed to the My Forms section and click on about the type you want.

Gain access to the Minnesota Certificate of Borrower regarding Commercial Loan with US Legal Forms, by far the most extensive catalogue of authorized record themes. Use thousands of expert and express-particular themes that fulfill your company or personal requirements and demands.

Form popularity

FAQ

The first ratio commercial lenders look at is the Loan-To-Value Ratio. The (LTV) equals the amount of the commercial mortgage divided by the market value of the property as determined by a commercial appraisal. Typically, Loan-To-Value Ratios for commercial real estate loans are capped at 75% or 80%.

Lenders typically look at your credit score ? both business credit score and personal ? along with taking a look at your business's cash flow and debts to determine your ability to repay the loan. In particular, lenders are likely to look at the following factors: Debt service ability. Income and expense trends.

These documents are used by the lenders to evaluate whether or not they will provide you with a loan. Loan documents are necessary to initiate a loan approval process by a lender. Some documents that may be required are tax returns, bank statements, pay stubs, W2, and a proof of income.

A bank will typically request, at a minimum, the following documentation for a startup business: A personal financial statement and personal federal income tax returns from the last one to three years. Projected startup cost estimates. Projected balance sheets and income statements for at least two years.

A business loan agreement is a legally binding document that outlines the details of a loan between a lender and borrower. Loan agreements typically include information like the loan amount, repayment term and due dates, interest rates and other costs.

Borrower Certification means, with respect to any request for a Loan, a certification of the Borrower stating that (i) no Default or Event of Default will occur or be continuing after giving effect to such Loan, and (ii) the proceeds of such Loan will be used solely for Permitted Uses.

Usually, a score of 600 or higher is required. Some loan programs accept scores as low as 500.

What are the Factors Banks Consider Before Granting a Loan to a Business? Credit History. Cash Flow. Collateral. Repayment Capacity. Documents.