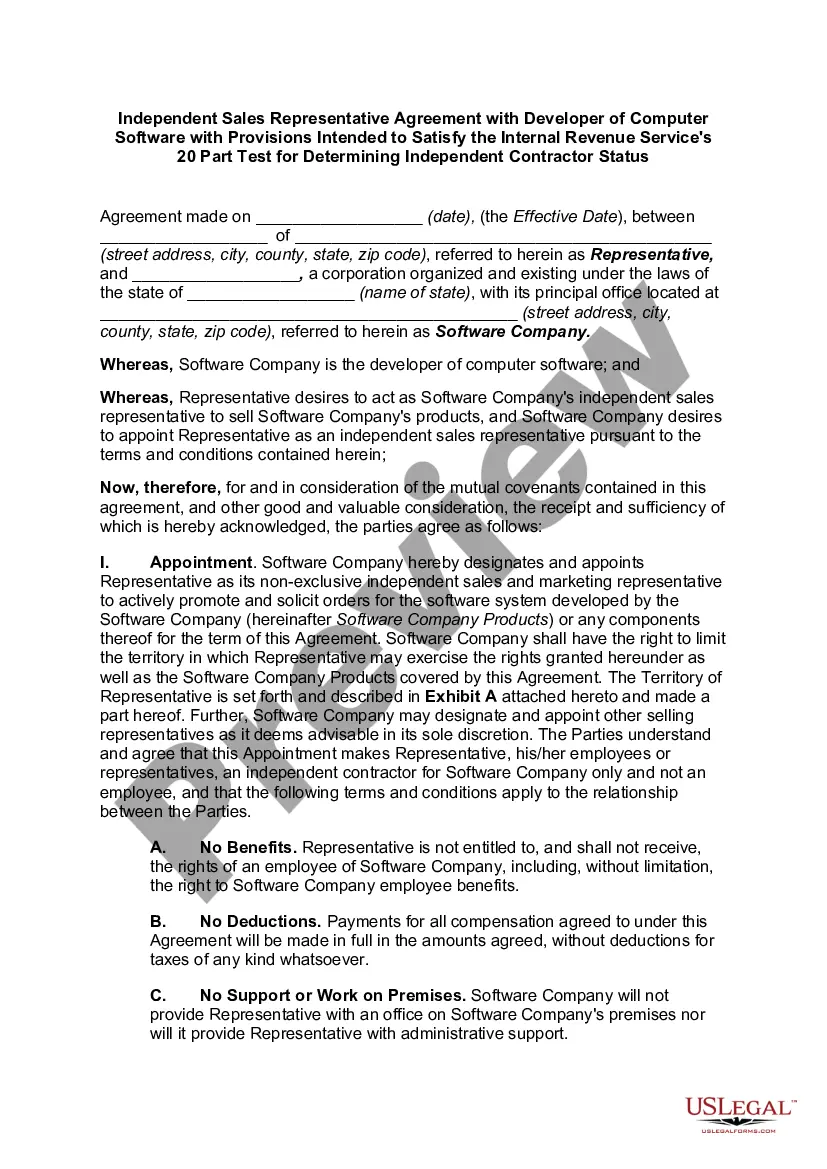

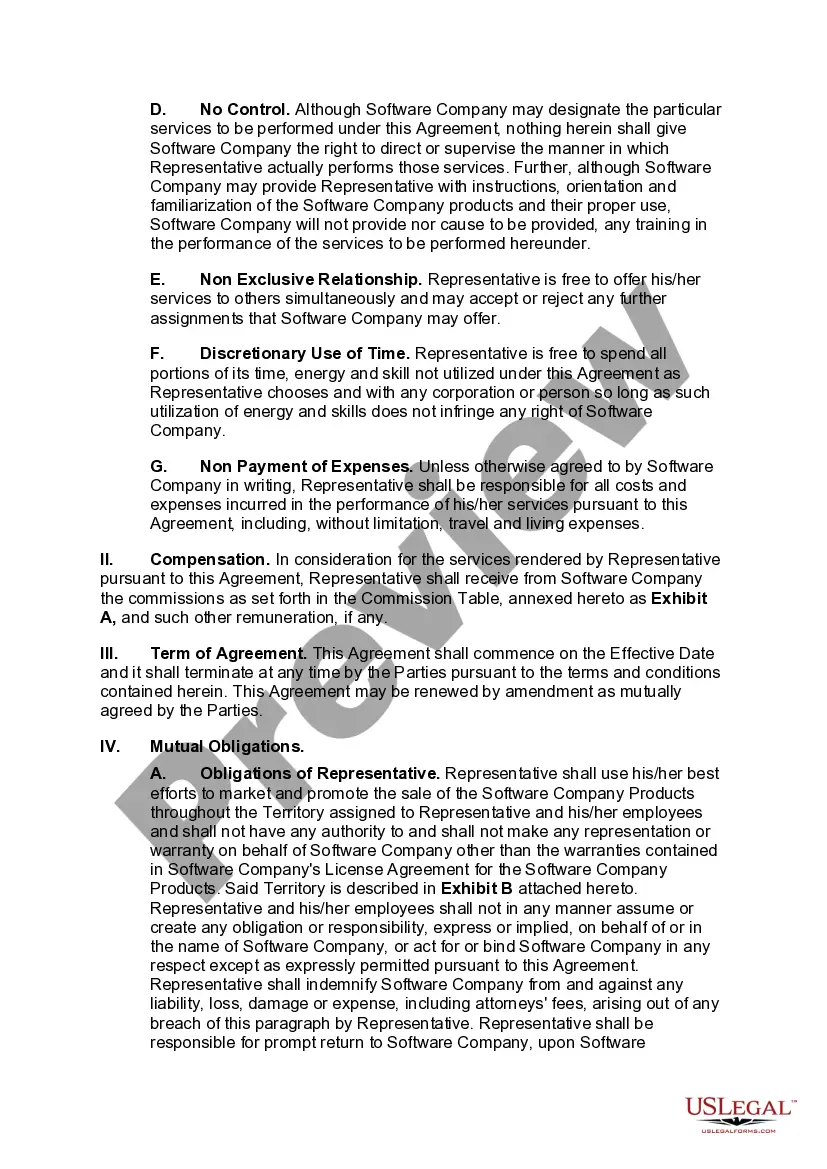

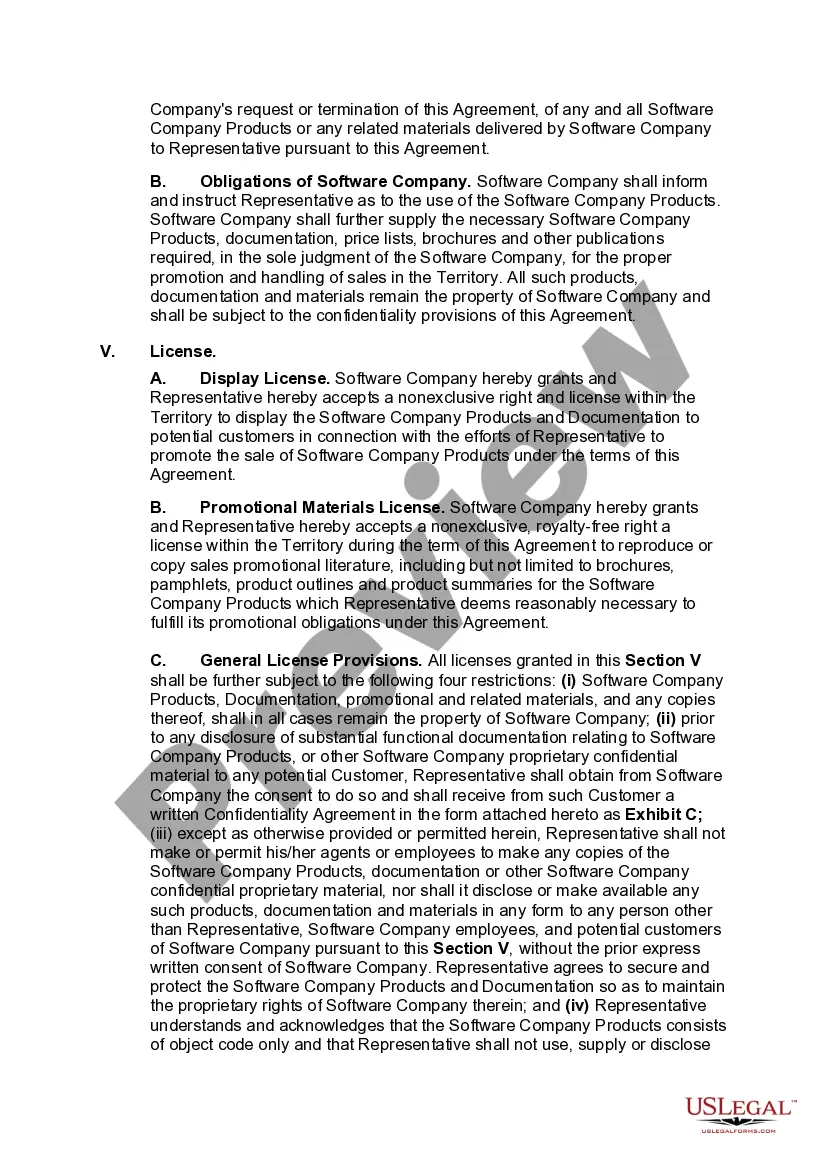

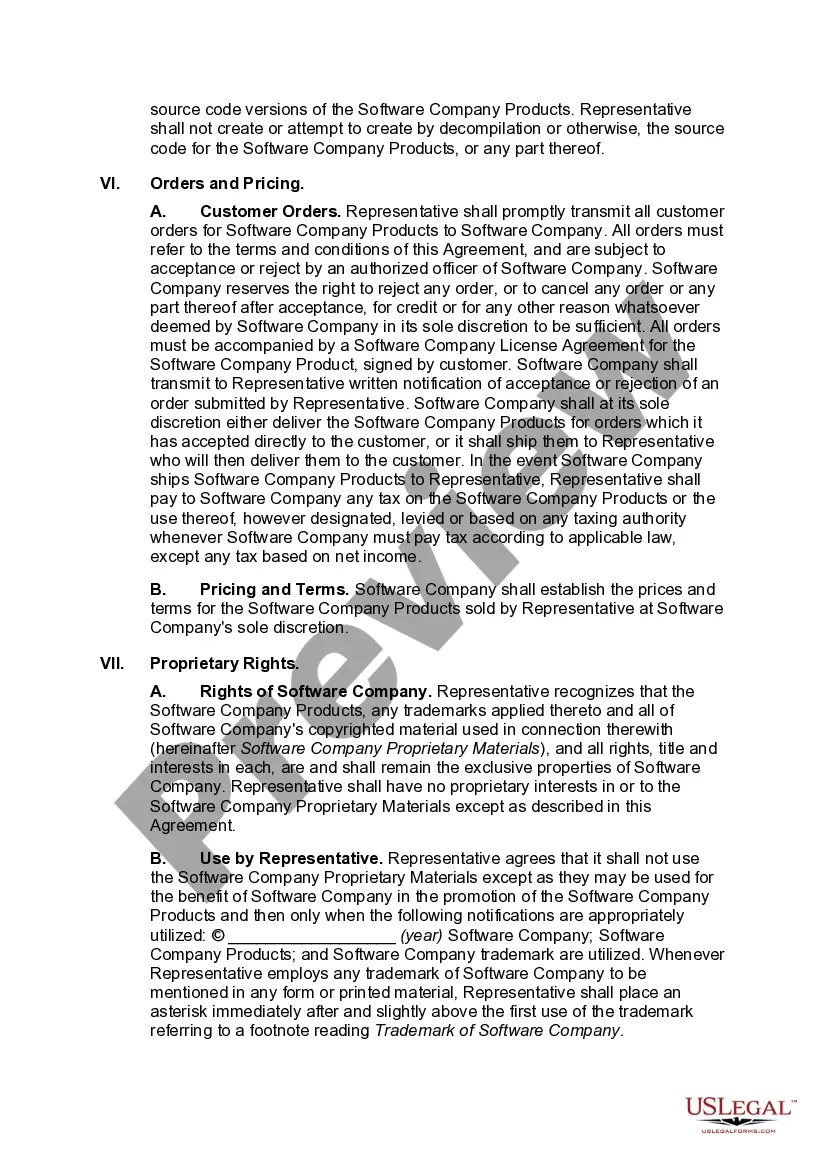

Title: Understanding Minnesota Independent Sales Representative Agreement with Developer of Computer Software to Ensure Independent Contractor Status Keywords: Minnesota, independent sales representative agreement, developer of computer software, Internal Revenue Service, 20-part test, independent contractor status Introduction: In Minnesota, it is crucial for both the developer of computer software and independent sales representatives to establish their working relationship through a well-defined agreement. This article will delve into the different types of Minnesota Independent Sales Representative Agreements with Developers of Computer Software, specifically crafted to satisfy the Internal Revenue Service's 20 Part Test defining independent contractor status. Understanding these agreements is essential for both parties to ensure legal compliance and to protect their rights and obligations. 1. Minnesota Independent Sales Representative Agreement with Developer of Computer Software: This type of agreement is designed to clearly outline the terms and conditions between a developer of computer software and an independent sales representative operating within the state of Minnesota. By tailoring the agreement to meet the criteria set forth by the Internal Revenue Service, both parties can establish the independent contractor status and mitigate any potential misclassification issues. 2. Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test: To ensure compliance with the Internal Revenue Service's 20 Part Test for determining independent contractor status, specific provisions should be included in the agreement. These provisions may cover factors such as control, financial aspects, relationship details, and the overall nature of the working arrangement. Including these provisions allows both the developer and representative to demonstrate their commitment to maintaining an independent contractor relationship, as required by the IRS. Key Provisions of the Agreement: a. Control: The agreement should clearly outline that the developer does not exert direct control over the representative's work methods or results. This provision emphasizes the independent nature of the relationship. b. Financial Aspects: Addressing compensation terms, such as commissions, and clarifying that the representative is responsible for their own expenses, further supports the independent contractor status. c. Relationship Details: Defining the working relationship as non-exclusive, and allowing the representative to work with other similar businesses, reaffirms the independent nature of the engagement. d. Nature of the Working Arrangement: Providing a clear description of the representative's duties, as well as the freedom to set their own work schedule, strengthens the argument for independent contractor status. Conclusion: By entering into a Minnesota Independent Sales Representative Agreement with Developer of Computer Software, with provisions intended to satisfy the Internal Revenue Service's 20 Part Test for determining independent contractor status, both parties can establish a solid foundation for their working relationship. It is important to consult legal professionals familiar with Minnesota labor laws to ensure the agreement meets all necessary requirements and safeguards the rights and obligations of both parties involved.

Minnesota Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status

Description

How to fill out Minnesota Independent Sales Representative Agreement With Developer Of Computer Software With Provisions Intended To Satisfy The Internal Revenue Service's 20 Part Test For Determining Independent Contractor Status?

US Legal Forms - one of the most significant libraries of legitimate varieties in the United States - delivers a wide array of legitimate papers layouts you may obtain or produce. While using website, you can get thousands of varieties for business and personal uses, sorted by types, says, or key phrases.You can get the most recent models of varieties such as the Minnesota Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status within minutes.

If you already possess a registration, log in and obtain Minnesota Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status from the US Legal Forms library. The Obtain key will appear on every type you look at. You gain access to all previously delivered electronically varieties in the My Forms tab of your own account.

If you want to use US Legal Forms initially, listed here are easy directions to help you started out:

- Be sure you have selected the correct type for your personal area/area. Go through the Preview key to examine the form`s articles. Read the type explanation to ensure that you have selected the right type.

- When the type doesn`t match your needs, use the Look for area near the top of the display to find the one that does.

- In case you are pleased with the shape, confirm your choice by visiting the Acquire now key. Then, choose the rates plan you prefer and provide your qualifications to register for an account.

- Approach the purchase. Make use of your credit card or PayPal account to accomplish the purchase.

- Find the structure and obtain the shape on the device.

- Make alterations. Fill out, change and produce and signal the delivered electronically Minnesota Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status.

Each web template you added to your bank account does not have an expiration day and it is the one you have forever. So, in order to obtain or produce an additional duplicate, just proceed to the My Forms segment and click about the type you need.

Gain access to the Minnesota Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status with US Legal Forms, one of the most extensive library of legitimate papers layouts. Use thousands of skilled and express-distinct layouts that fulfill your small business or personal requires and needs.