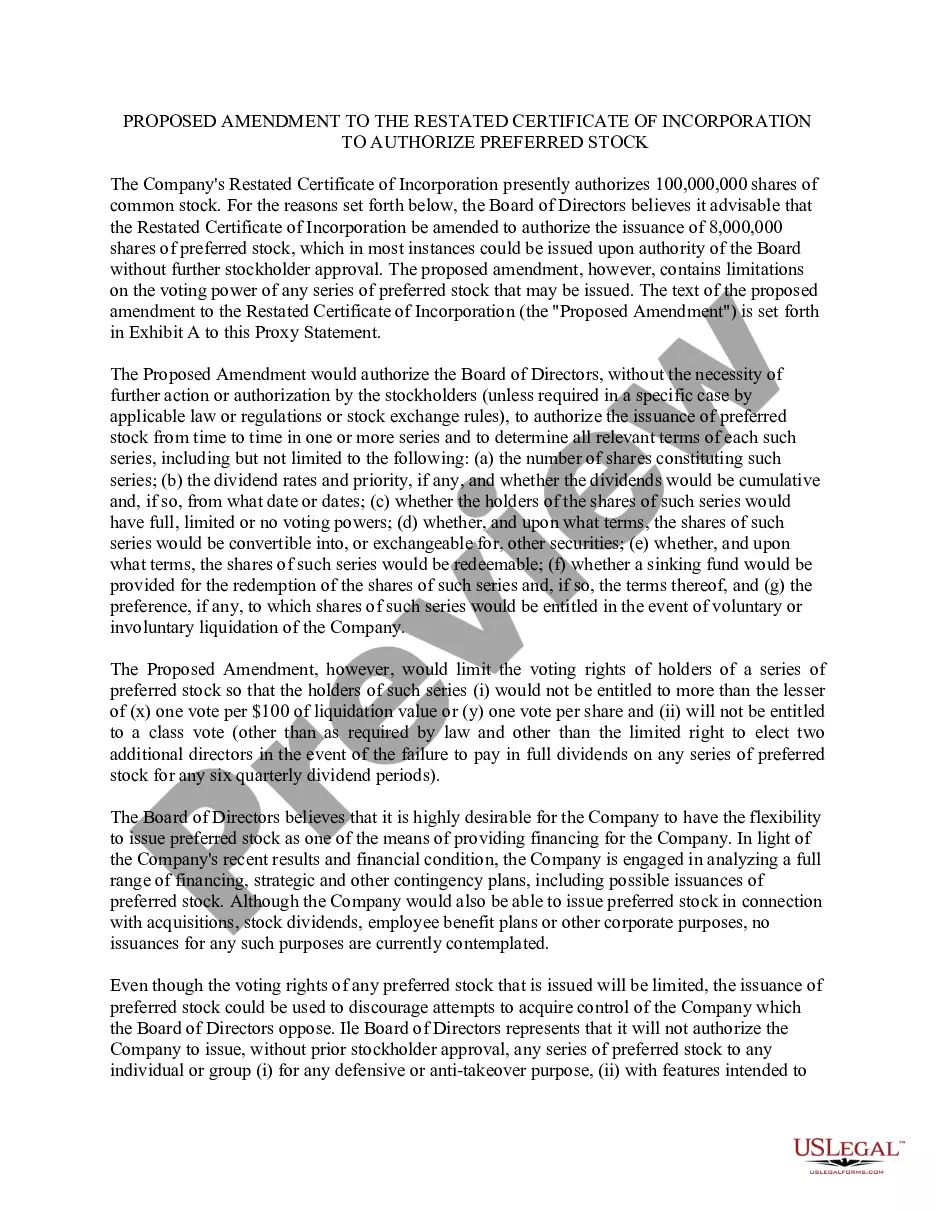

Minnesota Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

Discovering the right lawful file template might be a have difficulties. Obviously, there are a lot of themes available online, but how can you find the lawful form you want? Utilize the US Legal Forms internet site. The services delivers a huge number of themes, for example the Minnesota Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, which you can use for enterprise and personal requires. Each of the types are checked by specialists and meet state and federal specifications.

When you are already listed, log in to the bank account and click the Download button to obtain the Minnesota Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock. Make use of your bank account to appear from the lawful types you might have bought earlier. Go to the My Forms tab of your bank account and have one more copy in the file you want.

When you are a whole new customer of US Legal Forms, allow me to share simple instructions that you can stick to:

- Very first, make sure you have selected the appropriate form for your area/county. It is possible to look through the form utilizing the Preview button and read the form description to make sure this is basically the best for you.

- In case the form fails to meet your preferences, utilize the Seach industry to discover the right form.

- When you are certain the form is suitable, click the Acquire now button to obtain the form.

- Pick the prices program you need and enter the needed information and facts. Make your bank account and pay for your order with your PayPal bank account or credit card.

- Opt for the file formatting and obtain the lawful file template to the system.

- Total, revise and print and sign the received Minnesota Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

US Legal Forms is the greatest local library of lawful types where you can find different file themes. Utilize the company to obtain expertly-made documents that stick to express specifications.

Form popularity

FAQ

An Amended and Restated Certificate of Incorporation is a legal document filed with the Secretary of State that restates, integrates, and adjusts the startup's initial Articles of Incorporation (i.e. the company's Charter).

?Amended? means that the document has ?changed?? that someone has revised the document. ?Restated? means ?presented in its entirety?, ? as a single, complete document. ingly, ?amended and restated? means a complete document into which one or more changes have been incorporated.