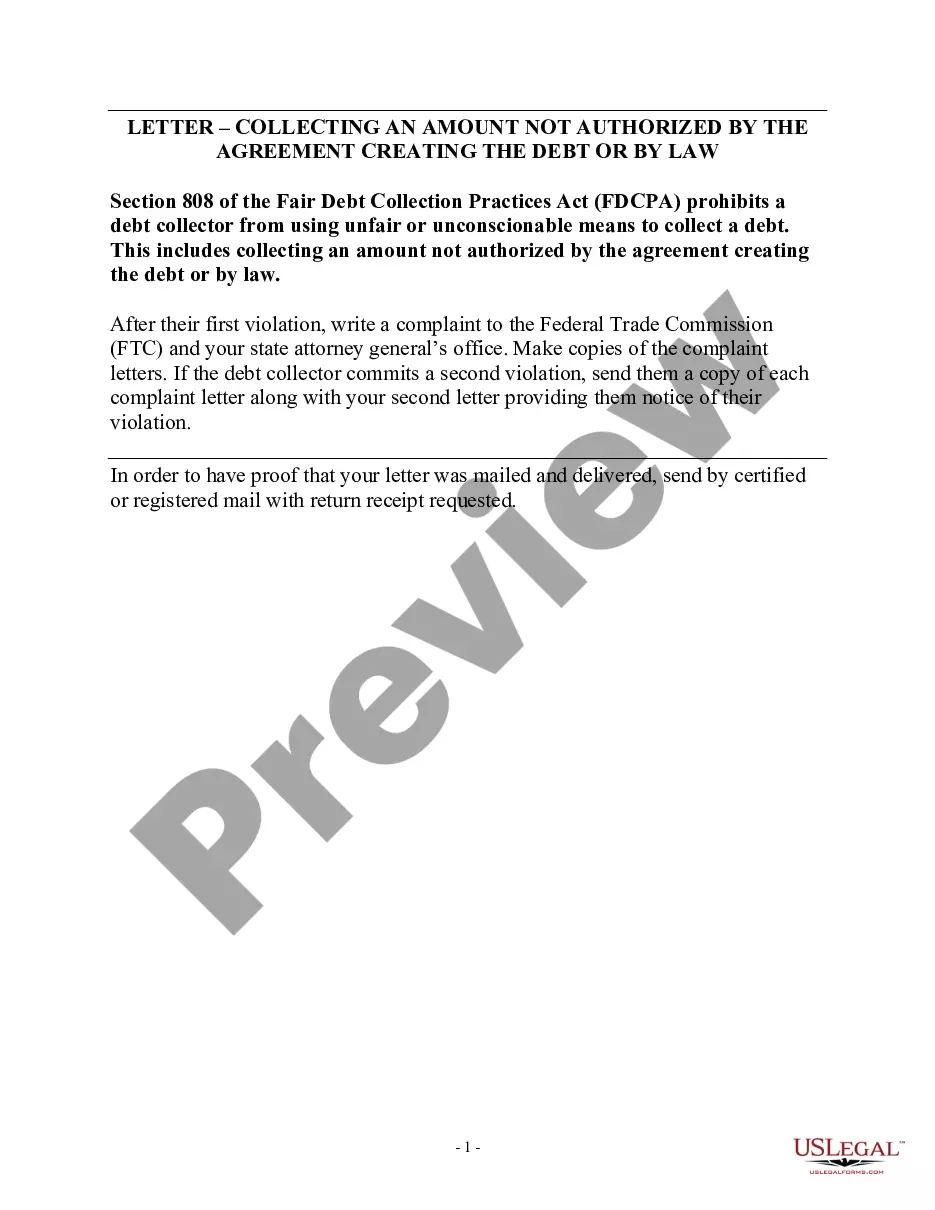

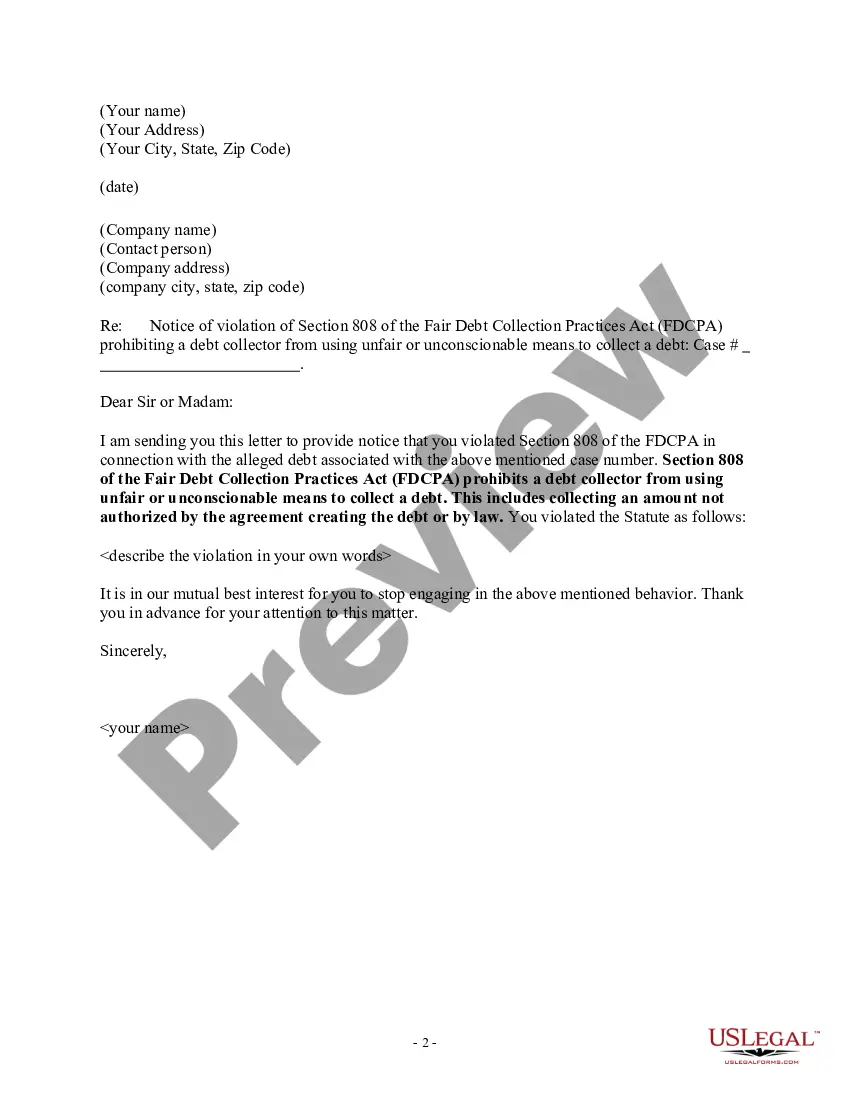

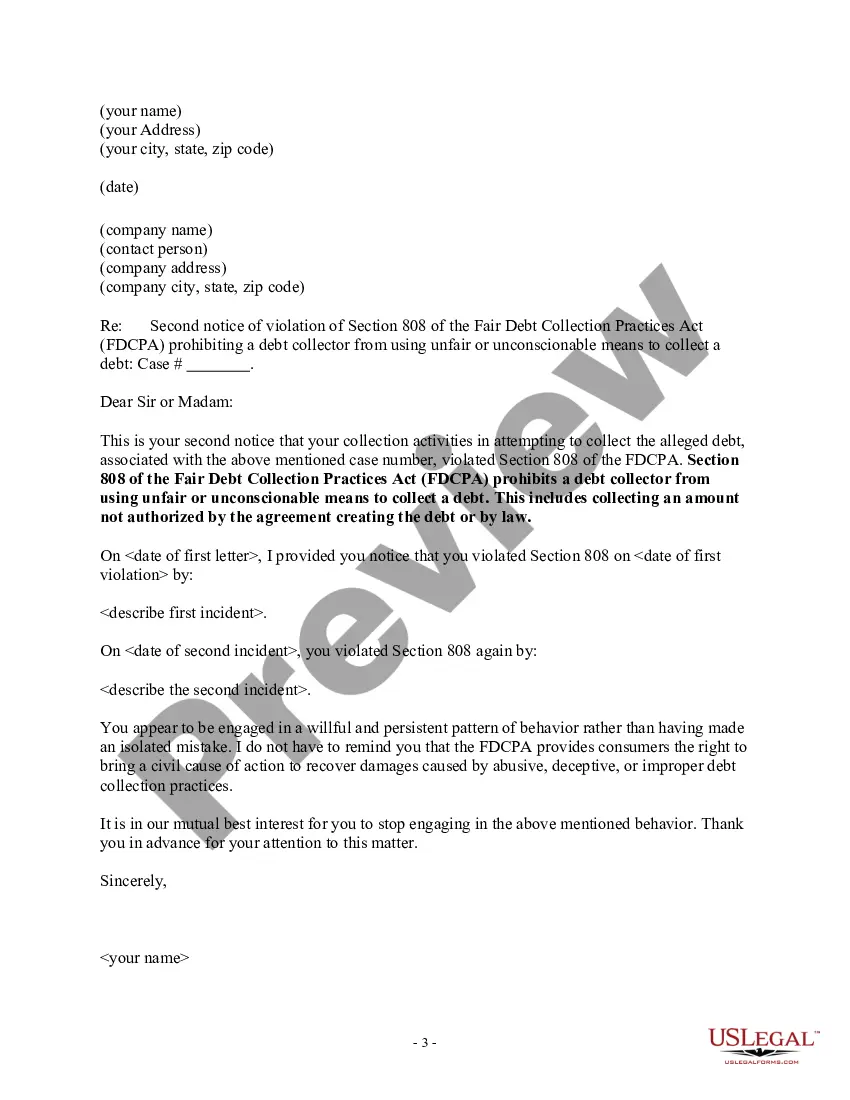

A debt collector may not use unfair or unconscionable means to collect a debt. This includes collecting an amount not authorized by the agreement creating the debt or by law.

Minnesota Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law

Category:

State:

Multi-State

Control #:

US-DCPA-42

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Minnesota Notice To Debt Collector - Collecting An Amount Not Authorized By Agreement Or By Law?

Are you currently within a place that you need to have documents for either business or individual functions virtually every day? There are tons of authorized papers layouts available online, but getting kinds you can trust is not effortless. US Legal Forms provides a large number of kind layouts, such as the Minnesota Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law, that are composed to fulfill state and federal specifications.

In case you are already knowledgeable about US Legal Forms site and get an account, simply log in. Afterward, it is possible to down load the Minnesota Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law template.

Should you not offer an account and would like to start using US Legal Forms, adopt these measures:

- Discover the kind you will need and ensure it is to the correct metropolis/region.

- Take advantage of the Review option to examine the shape.

- See the explanation to actually have selected the correct kind.

- In case the kind is not what you are searching for, use the Research area to get the kind that fits your needs and specifications.

- Whenever you obtain the correct kind, simply click Get now.

- Choose the prices plan you would like, complete the required details to make your account, and purchase your order utilizing your PayPal or bank card.

- Select a handy paper format and down load your version.

Discover each of the papers layouts you may have bought in the My Forms menus. You may get a additional version of Minnesota Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law any time, if required. Just click the required kind to down load or print out the papers template.

Use US Legal Forms, one of the most comprehensive variety of authorized forms, to conserve time as well as prevent blunders. The services provides expertly manufactured authorized papers layouts which can be used for a range of functions. Make an account on US Legal Forms and commence creating your way of life easier.

Form popularity

FAQ

For most debts, the time limit is 6 years since you last wrote to them or made a payment. The time limit is longer for mortgage debts. If your home is repossessed and you still owe money on your mortgage, the time limit is 6 years for the interest on the mortgage and 12 years on the main amount.

You are not obliged let a debt collector into your home and they don't have the right to take goods away. It's very important to understand that a debt collector is not the same as an enforcement agent or bailiff. Debt collectors have no special legal powers.

The statute of limitations for bringing a lawsuit for breach of contract under Minnesota law is six (6) years. This means that a creditor or debt collector can sue you anytime within six (6) years from the date of your last purchase or last payment, whichever was later.

Once a judgment is docketed, a judgment lien in Minnesota generally lasts for 10 years.

The validation notice is meant to help you recognize whether the debt is yours and dispute the debt if it is not yours. The notice generally must include: A statement that the communication is from a debt collector. The name and mailing information of the debt collector and the consumer.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

Repeated calls. Threats of violence. Publishing information about you. Abusive or obscene language.

5 years (to file a lien. Lien remains in place for 10 years.) As you can see in the chart above, debt collectors in Minnesota have between four and six years from the last payment to pursue legal action, depending on the type of debt. After the statute of limitations runs out, the debt becomes known as time-barred.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

More info

21-May-2019 ? all FDCPA-covered debt collectors. provisions that rely on the Bureau's. Dodd-Frank Act rulemaking authority generally would not, therefore, ... You may owe a debt, but you still have rights. And debt collectors have to obey the law. If You Owe Money Creditors don't want to bring in a debt collection ...21-May-2019 ? Proposed rule Start Printed Page 23275provisions that rely on the Bureau's Dodd-Frank Act rulemaking authority generally would not, therefore, ... If a private collection agency worked on your ED-held loans, it will no longerFederal law related to the collection of debts owed to the government ... After they get your no-contact letter, the collector can only call or write you to tell you what legal action they plan to take. Remember, sending a no-contact ... 07-Jul-2021 ? Before completing any transaction on your behalf through any SezzleWhere prohibited by law, Sezzle does not charge fees for account ... By S Glover · Cited by 3 ? inclusion in William Mitchell Law Review by an authorized administratorIn Minnesota, debt collectors and debt buyers may commence. 13-Aug-2020 ? Under the CARES Act, a servicer of federally backed mortgage loan may not:While Illinois and Minnesota do not treat debt collectors as ... A written request to cease communication will not prohibit the debt collector or collection agency from taking any other action authorized by law to collect ... (19) attempt to collect any amount of money from a debtor or charge a fee to a creditor that is not authorized by agreement with the client;.