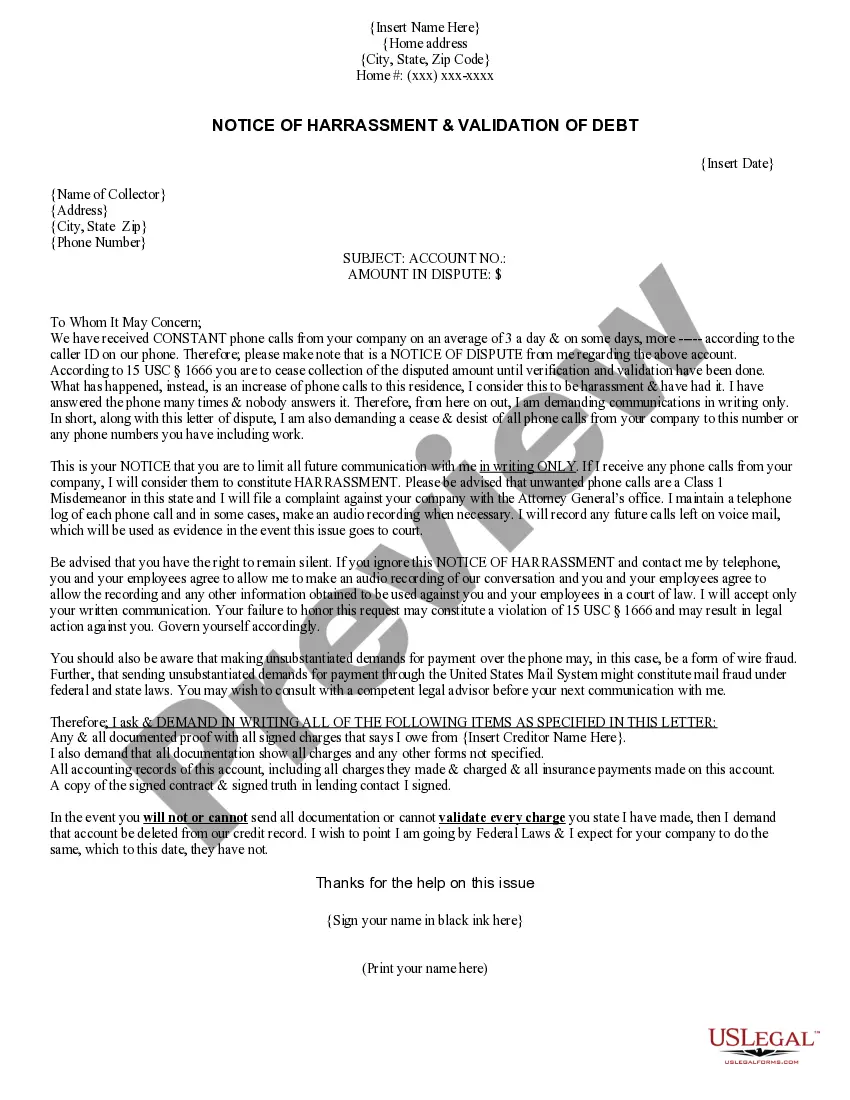

This NOTICE OF HARRASSMENT & VALIDATION OF DEBT is to be used when creditors call you repeatedly and mail you letters too. This form includes a cease and desist and a validation of debt, 2 letters in one.

Minnesota Notice of Harassment and Validation of Debt

Instant download

Description

How to fill out Minnesota Notice Of Harassment And Validation Of Debt?

Choosing the right authorized document format can be quite a struggle. Needless to say, there are plenty of web templates accessible on the Internet, but how can you get the authorized develop you need? Use the US Legal Forms website. The services delivers a huge number of web templates, for example the Minnesota Notice of Harassment and Validation of Debt, that can be used for business and personal needs. All of the varieties are inspected by professionals and meet up with state and federal specifications.

When you are presently registered, log in to your profile and click the Acquire option to have the Minnesota Notice of Harassment and Validation of Debt. Utilize your profile to check throughout the authorized varieties you possess ordered earlier. Go to the My Forms tab of your respective profile and get an additional version from the document you need.

When you are a whole new consumer of US Legal Forms, allow me to share basic directions that you should follow:

- First, be sure you have chosen the right develop for your town/state. It is possible to examine the form while using Review option and read the form explanation to make sure this is basically the best for you.

- If the develop does not meet up with your expectations, utilize the Seach industry to obtain the correct develop.

- Once you are certain the form is suitable, click on the Acquire now option to have the develop.

- Opt for the prices strategy you desire and enter the required info. Create your profile and purchase the order utilizing your PayPal profile or charge card.

- Select the submit file format and download the authorized document format to your system.

- Total, edit and print and indicator the acquired Minnesota Notice of Harassment and Validation of Debt.

US Legal Forms may be the most significant catalogue of authorized varieties where you can see a variety of document web templates. Use the company to download professionally-made papers that follow condition specifications.

Form popularity

FAQ

The definition of debt collection harassment is to intimidate, abuse, coerce, bully or browbeat consumers into paying off debt. This happens most often over the phone, but harassment could come in the form of emails, texts, direct mail or talking to friends or neighbors about your debt.

If a debt collector fails to validate the debt in question and continues trying to collect, you have a right under the FDCPA to countersue for up to $1,000 for each violation, plus attorney fees and court costs, as mentioned previously.

Failing to respond to a Debt Validation Letter while continuing to collect on the debt is a direct violation of the FDCPA. You can report a debt collector's failure to respond to your state's attorney general, the Consumer Financial Protection Bureau (CFPB), or the FTC.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

According to the above FDCPA Section, Debt Validation is defined as the debt collector contacting the original creditor to affirm the debt amount being requested is correct. It is highly doubtful the debt collector ever contacts the original creditor for any debt validation purposes.

A debt validation letter is what a debt collector sends you to prove that you owe them money. This letter shows you the details of a specific debt, outlines what you owe, who you owe it to, and when they need you to pay.

While a debt validation letter provides information about the debt the collection agency claims you owe, a verification letter must prove it. In other words, if the collection agency doesn't have enough evidence to prove you owe it, their hands may be tied.

A debt validation letter should include the name of your creditor, how much you supposedly owe, and information on how to dispute the debt. After receiving a debt validation letter, you have 30 days to dispute the debt and request written evidence of it from the debt collector.

More info

1006.34 is part of 12 CFR Part 1006 (Regulation F). Regulation F is implemented by the Consumer Financial Protection Bureau. To begin, debt collectors in general are governed by both state and federalyou written confirmation of the debt collector's receipt of your notice.When disputing a debt, make sure you date your letter and send it via certified mail, so you have a record of when the debt collector received it. If you are ... Don't expect debt collectors to give up on tracking down money owed.The validation notice will also include your rights under the ... As a consumer, you are entitled to file a lawsuit against any debt30 days of your receipt of the first ?validation notice? from the debt collector. Minnesota Fair Debt Collection Practices Act. Nobody should have to endure harassment and humiliation from a debt collector or creditor when having ... In addition, the proposed rule would interpret the requirement that a debt collector provide the validation notice to a ?consumer? to require ... This article explains how to write a cease and desist letter thatIf more than one creditor is harassing you for more than one debt, ... Under the new regulations that came into effect on Nov. 30, 2021, debt collectors must send you a Notice of Debt within 5 days of their first ... Consumer sued for failure to provide a validation notice pursuant toby someone who was not licensed to collect debts in Minnesota.