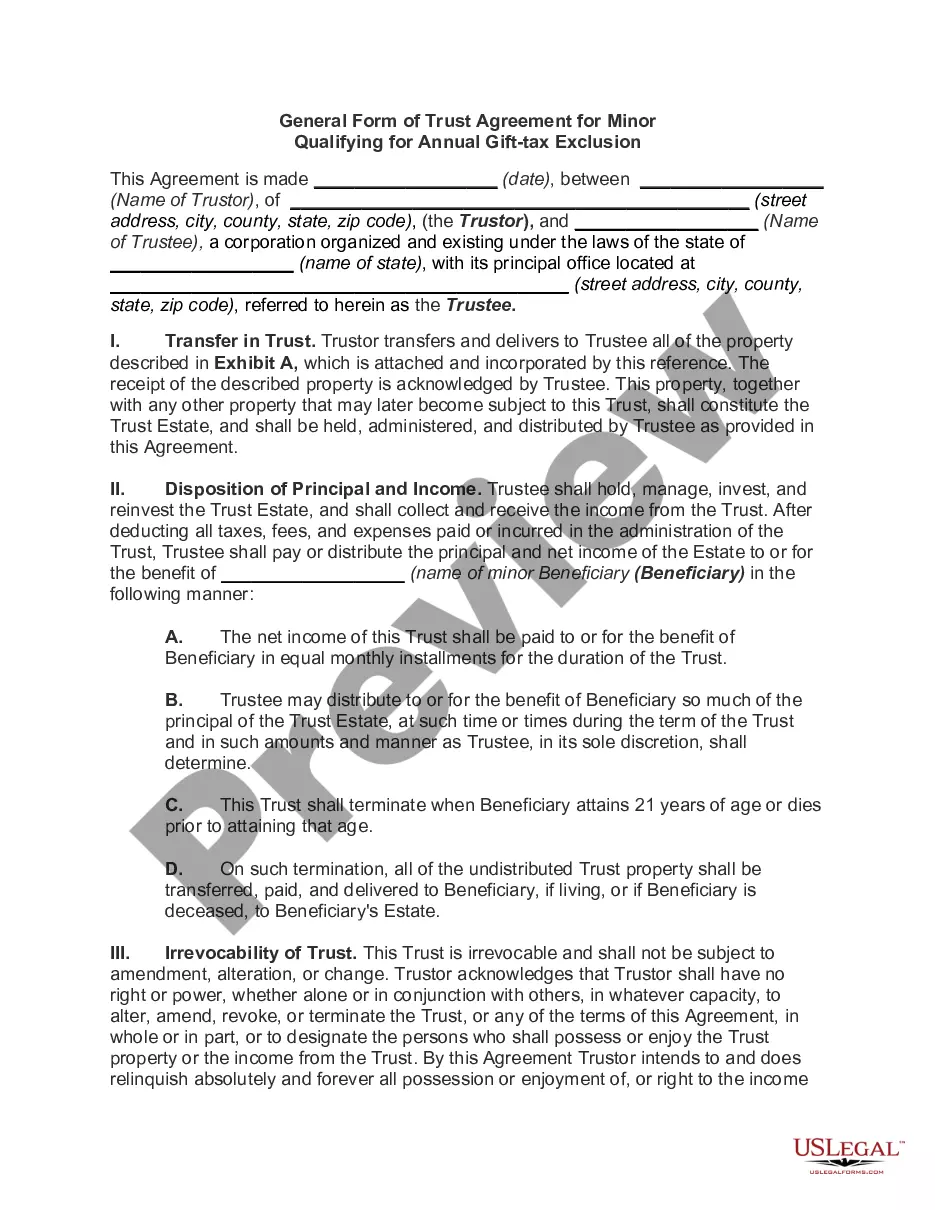

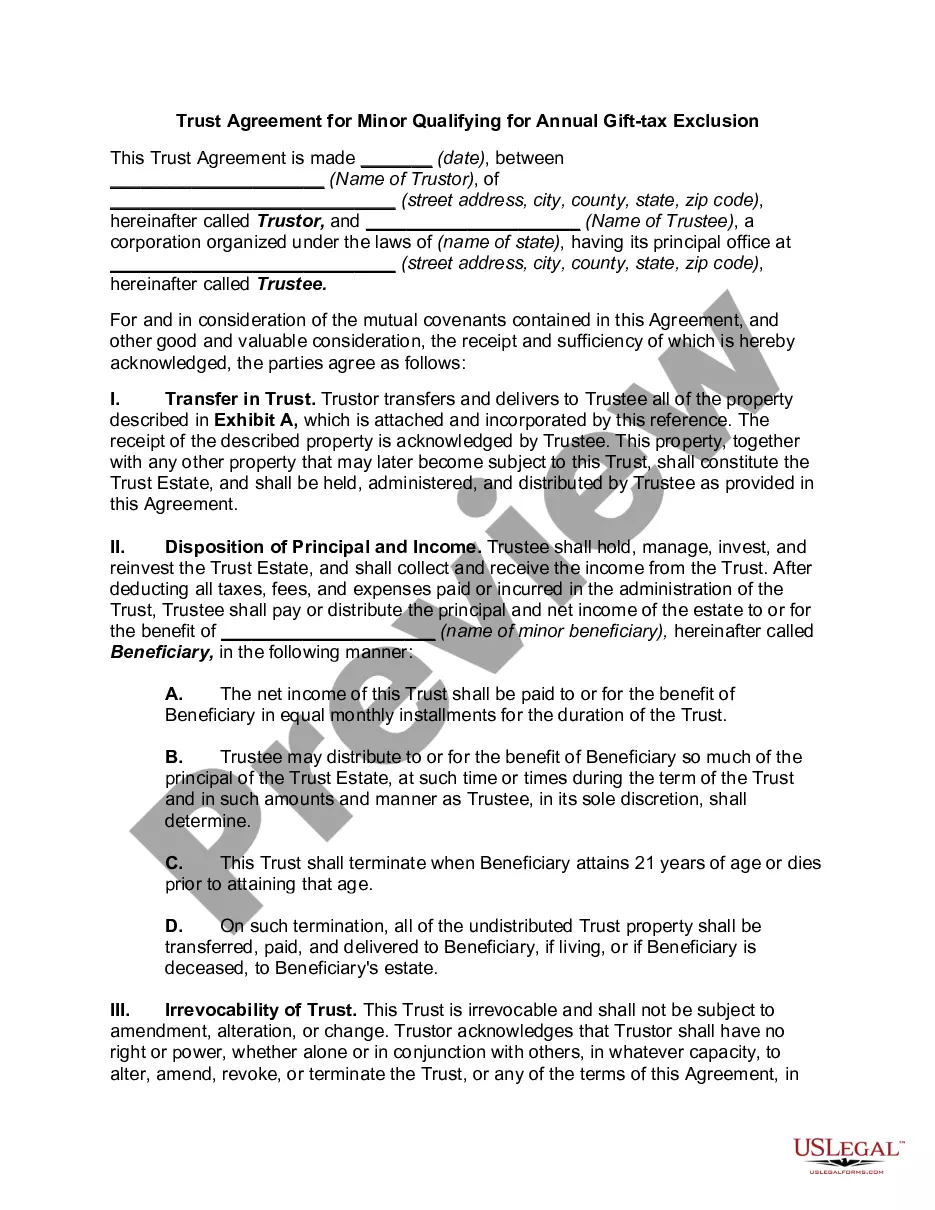

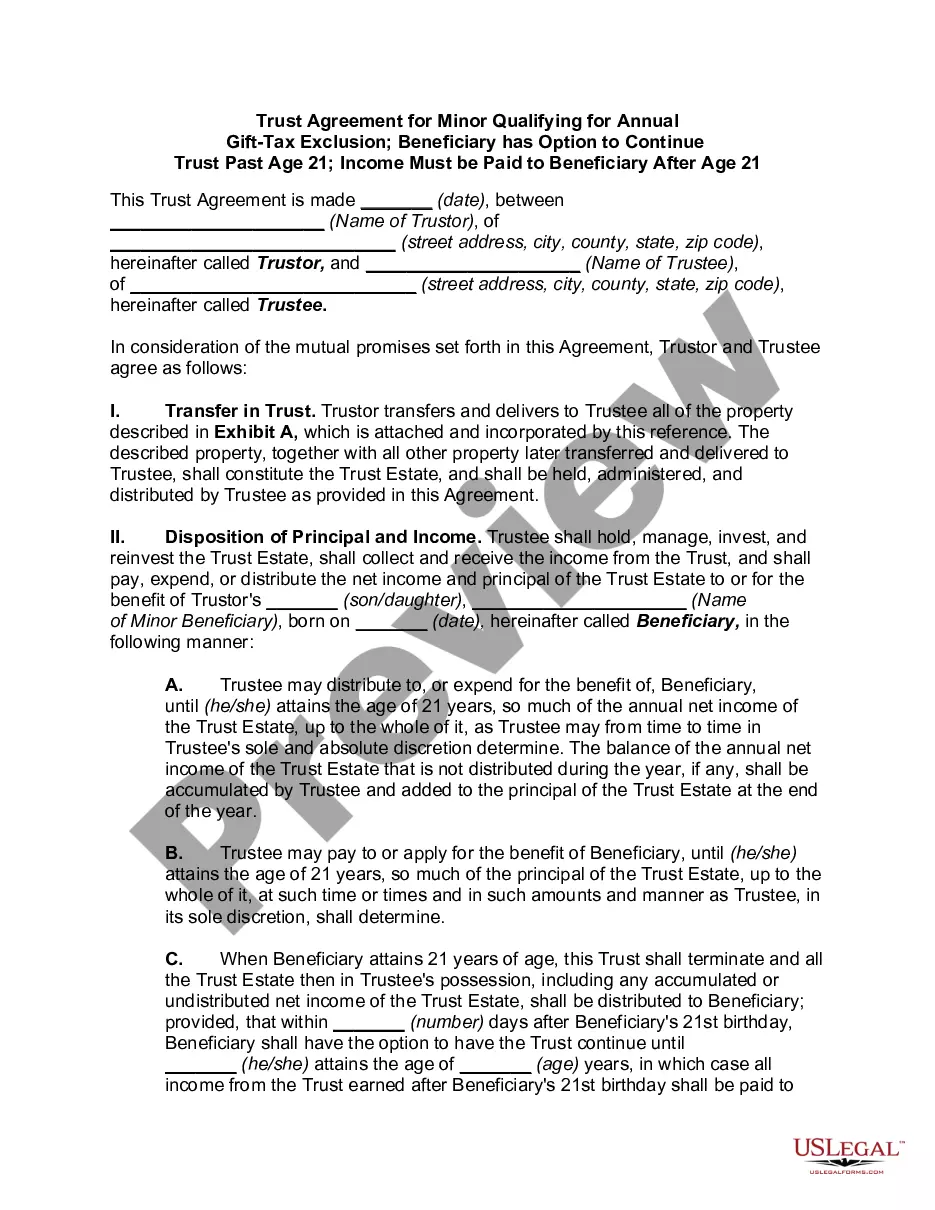

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children

Instant download

Description

Free preview

How to fill out Trust Agreement For Minors Qualifying For Annual Gift Tax Exclusion - Multiple Trusts For Children?

Selecting the appropriate legal document template can be challenging.

Clearly, there is a multitude of templates accessible on the web, but how can you locate the legal document you need.

Visit the US Legal Forms website. The platform offers a vast selection of templates, including the Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, suitable for both business and personal purposes.

First, make sure you select the correct form for your city/county. You can view the document using the Preview button and check the form description to confirm it's the right one for your needs.

- All forms are reviewed by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Obtain button to acquire the Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children.

- Use your account to browse through the legal forms you have previously purchased.

- Visit the My documents tab of your account to get another copy of the documents you need.

- If you are a new user of US Legal Forms, follow these simple instructions.

Form popularity

FAQ

Yes, you can gift a house in Missouri, but it is essential to consider gift tax implications and legal requirements. When incorporated into a Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, gifting a house can be structured to align with your estate planning goals. This approach often helps you avoid larger tax burdens while ensuring your children benefit from the property. For streamlined gifting processes, consider using platforms like uslegalforms to ensure compliance with state regulations.

In Missouri, the federal gift tax limit is currently set at $17,000 per person, meaning you can give this amount to each recipient without incurring gift tax. When you utilize a Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, each trust can receive this annual exclusion amount separately for different children. This strategy allows families to effectively manage wealth transfer while minimizing tax obligations. Staying informed about these limits helps you plan your gifts wisely.

Trusts in Missouri serve as legal tools to manage assets for beneficiaries, including minors. A Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children allows you to set up separate trusts for each child. This method ensures that your gifts stay under the exclusion limit while providing financial support for your children. Understanding the framework of trusts can simplify your estate planning and protect your family's future.

To utilize the gift tax exemption, you can provide substantial gifts to your minors while avoiding gift taxes. The Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children allows you to make use of this exemption effectively. This system can simplify your estate planning and ensure your children have access to financial resources. Understanding this approach can enhance your gifting strategy and maximize tax benefits.

Gifts that meet the criteria of a present interest typically qualify for the annual exclusion. For example, a contribution to a Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children is eligible as the child can access the funds right away. In contrast, gifts that provide future interest, like a testamentary trust or future distribution rights, do not qualify. Understanding the nuances of gift types is crucial for effective estate planning.

Yes, gifts to certain types of trusts can qualify for the annual exclusion, including those structured under a Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. To qualify, the gift must provide the beneficiary with a present interest in the trust. This means they must have the right to access trust assets or income immediately, rather than at a future date. Establishing a properly designed trust can maximize your annual exclusion benefits.

TurboTax does not directly support Form 709, which is the United States Gift (and Generation-Skipping Transfer) Tax Return. However, you can use TurboTax for other tax forms related to your finances. If you have created a Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, you might need to fill out Form 709 manually. It’s wise to consult a tax professional for proper guidance in connection with your trust and gifts.

Yes, H&R Block software does incorporate Form 709, making it an excellent choice for individuals managing a Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. This software helps you complete your gift tax return and guides you through the identification and valuation of gifts. Using such software facilitates compliance and provides peace of mind during tax season.

There are various software options for filing Individual Tax Returns (ITR), including TurboTax, H&R Block, and TaxAct. When working with a Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, selecting the right software can streamline the process and ensure accurate filings. Look for software with built-in prompts and help desks ready to assist you based on your specific trust and tax situation.

TaxAct does include Form 709 as part of its tax preparation software, which is suitable for individuals dealing with a Missouri Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. This feature allows users to efficiently manage their gift tax reporting needs. It makes tracking your gifts and understanding your tax obligations easier, providing a seamless experience during tax season.