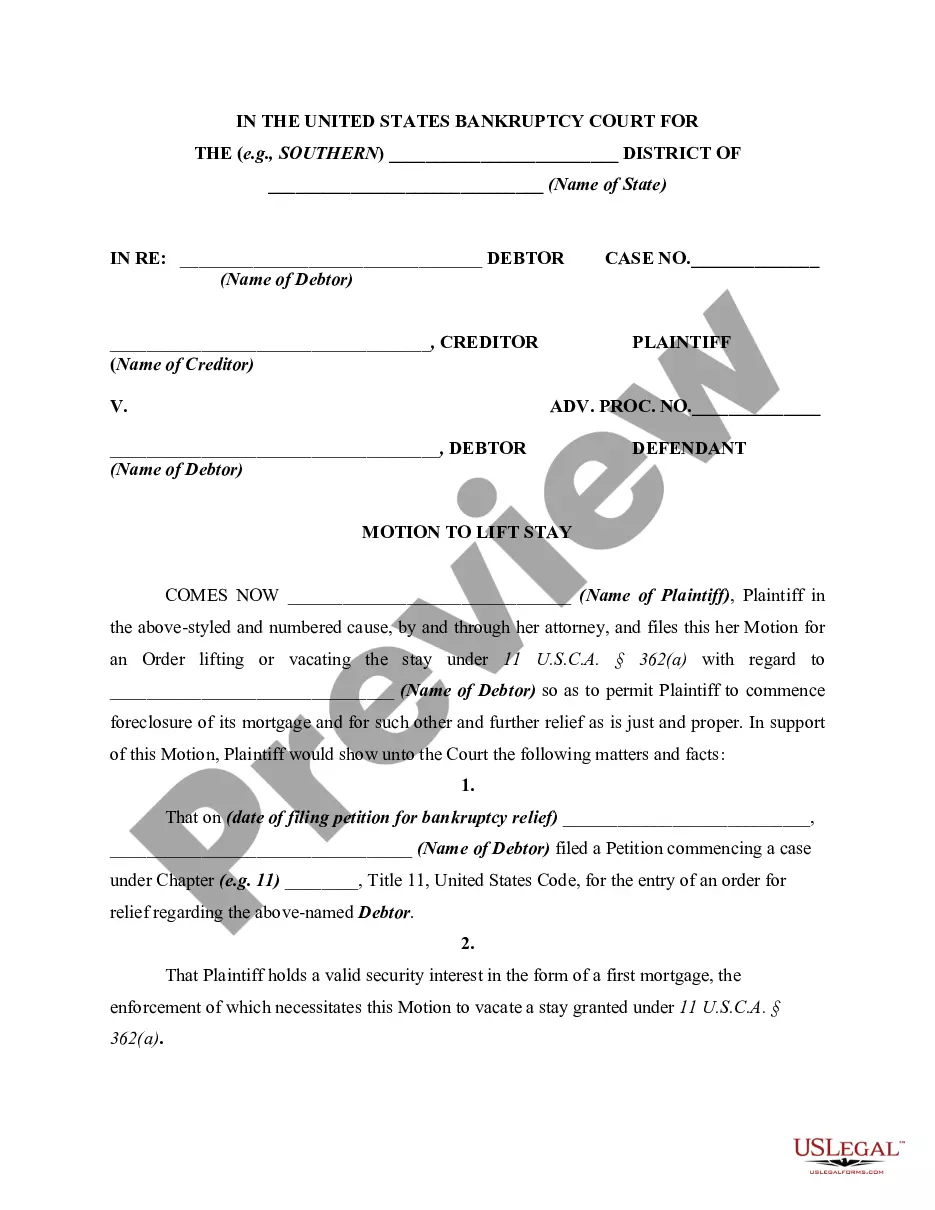

After the filing of the bankruptcy petition, the debtor needs protection from the collection efforts of its creditors. Therefore, the bankruptcy law provides that the filing of either a voluntary or involuntary petition operates as an automatic stay which prevents creditors from taking action against the debtor. This is similar to an injunction against the creditors of the debtor. The automatic stay ends when the bankruptcy case is closed or dismissed or when the debtor is granted a discharge.

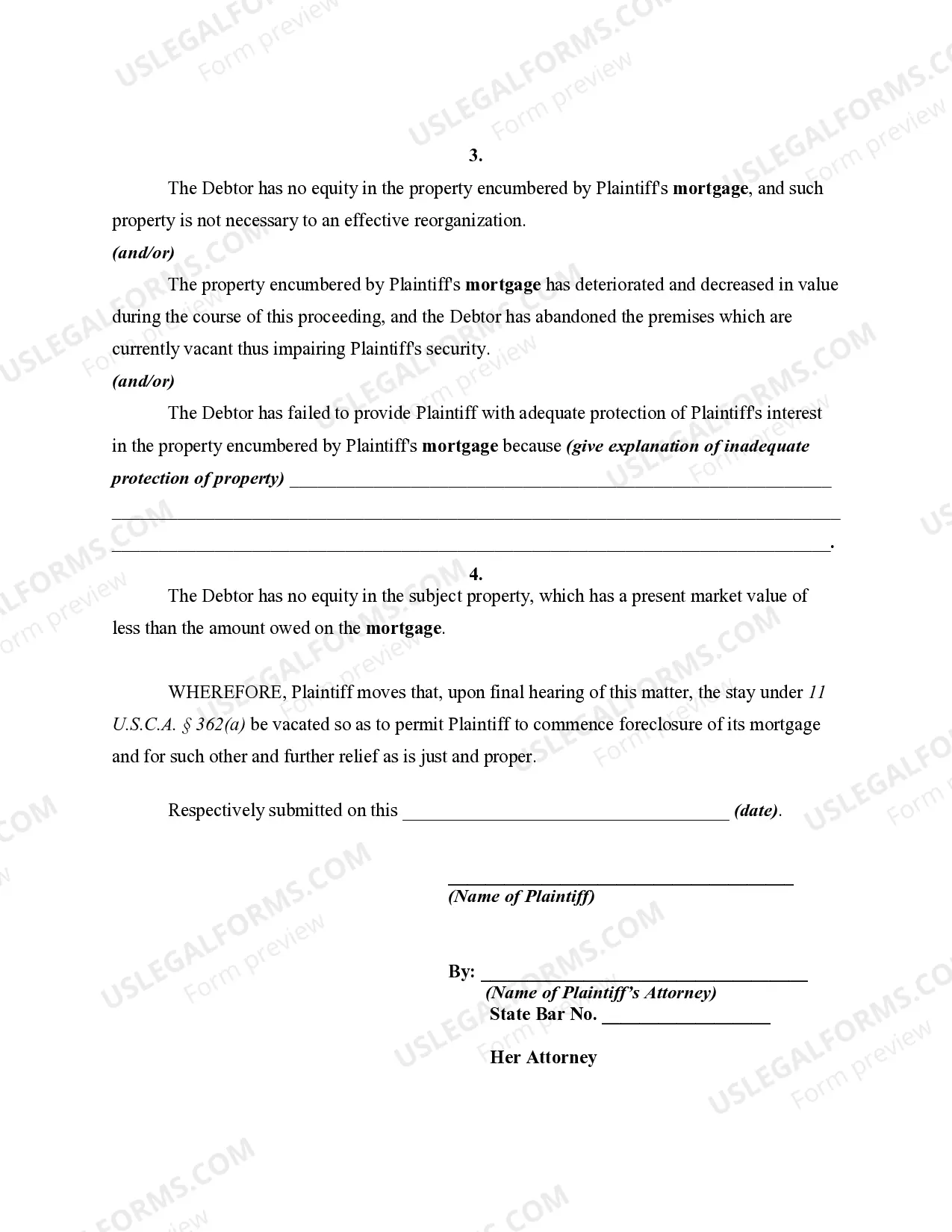

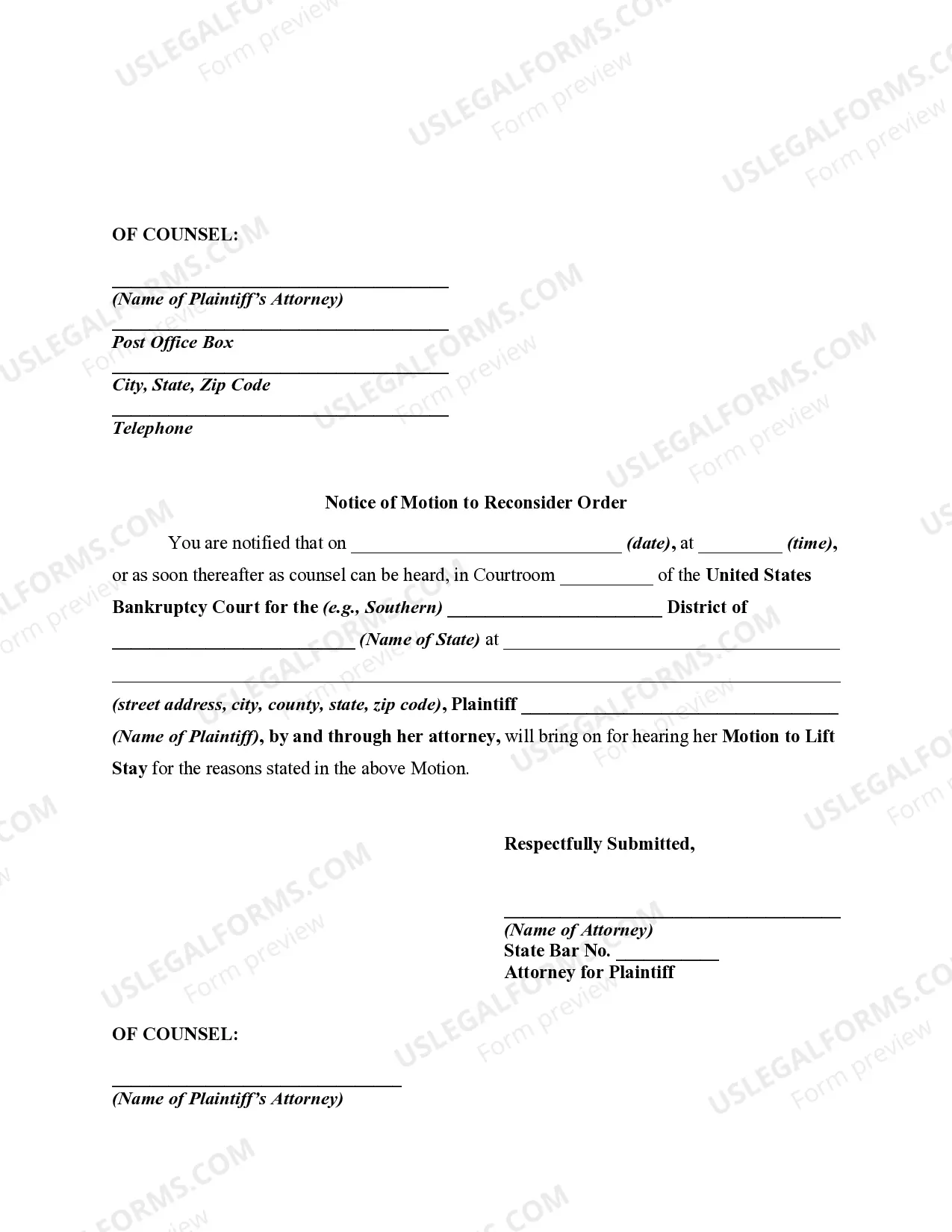

In the field of bankruptcy law, a Missouri Motion in Bankruptcy Court filed by a Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property plays a crucial role. This comprehensive motion empowers the mortgagee (the lender) to request the court's permission to proceed with foreclosure proceedings on a debtor's real property despite the automatic stay imposed by the bankruptcy case. Here is a detailed description of this motion, elaborating on its importance and potential variations: 1. Definition: A Motion in Bankruptcy Court by Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property is a formal legal document submitted to a bankruptcy court by a mortgage lender seeking authorization to proceed with foreclosure on a debtor's real estate property, which serves as collateral for a mortgage loan. 2. Purpose: The primary goal of this motion is to seek permission to bypass the automatic stay that is implemented when a debtor files for bankruptcy protection. The automatic stay prohibits creditors, including mortgagees, from pursuing collection or foreclosure actions against the debtor or their property while the bankruptcy case is ongoing. 3. Importance: A Motion in Bankruptcy Court by Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property enables the mortgagee to present compelling reasons to the court as to why they should be permitted to foreclose on the debtor's real estate despite the automatic stay. The outcome of this motion can significantly impact both the mortgagee and debtor's rights and financial situation. 4. Key Elements: This detailed motion typically comprises several crucial elements, including: — Identification: It provides the names and contact information of the mortgagee (lender), debtor (borrower), and their respective legal representatives. — Property Description: A detailed description of the property, including the address, legal description, and any associated liens or encumbrances. — Status of the Loan: A summary of the loan agreement, including the outstanding balance, default status, and any missed payments. — Justification for Vacating Stay: The motion must provide compelling grounds justifying the need to vacate the automatic stay, such as the debtor's inability to afford the mortgage payments, lack of equity in the property, non-exempt nature of the property, etc. — Financial Impact: The motion should outline the potential harm or financial burden faced by the mortgagee due to the continued delay in foreclosure. — Proposed Relief: The mortgagee should present the requested relief, which is the court's permission to proceed with foreclosure on the debtor's real property. 5. Potential Variations: Although the core purpose remains the same, there may be variations of this motion depending on certain factors. These could include: PREre or Post-Confirmation: The motion may be filed before or after the bankruptcy case is confirmed, each having its own set of requirements and implications. — Chapter of Bankruptcy: The motion's specific requirements and procedures can vary depending on the chapter of bankruptcy under which the debtor filed (Chapter 7, 11, 13, etc.). — Debtor's Intention: If the debtor intends to surrender the property or proposes an alternative plan for handling the mortgage debt, it may impact the mortgagee's motion and subsequent court decisions. In summary, a Missouri Motion in Bankruptcy Court by Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property is a critical legal request enabling a mortgage lender to seek authorization to proceed with foreclosure on a debtor's real estate during bankruptcy proceedings. Understanding the key components of this motion and its potential variations is essential for both mortgagees and debtors involved in bankruptcy cases.In the field of bankruptcy law, a Missouri Motion in Bankruptcy Court filed by a Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property plays a crucial role. This comprehensive motion empowers the mortgagee (the lender) to request the court's permission to proceed with foreclosure proceedings on a debtor's real property despite the automatic stay imposed by the bankruptcy case. Here is a detailed description of this motion, elaborating on its importance and potential variations: 1. Definition: A Motion in Bankruptcy Court by Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property is a formal legal document submitted to a bankruptcy court by a mortgage lender seeking authorization to proceed with foreclosure on a debtor's real estate property, which serves as collateral for a mortgage loan. 2. Purpose: The primary goal of this motion is to seek permission to bypass the automatic stay that is implemented when a debtor files for bankruptcy protection. The automatic stay prohibits creditors, including mortgagees, from pursuing collection or foreclosure actions against the debtor or their property while the bankruptcy case is ongoing. 3. Importance: A Motion in Bankruptcy Court by Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property enables the mortgagee to present compelling reasons to the court as to why they should be permitted to foreclose on the debtor's real estate despite the automatic stay. The outcome of this motion can significantly impact both the mortgagee and debtor's rights and financial situation. 4. Key Elements: This detailed motion typically comprises several crucial elements, including: — Identification: It provides the names and contact information of the mortgagee (lender), debtor (borrower), and their respective legal representatives. — Property Description: A detailed description of the property, including the address, legal description, and any associated liens or encumbrances. — Status of the Loan: A summary of the loan agreement, including the outstanding balance, default status, and any missed payments. — Justification for Vacating Stay: The motion must provide compelling grounds justifying the need to vacate the automatic stay, such as the debtor's inability to afford the mortgage payments, lack of equity in the property, non-exempt nature of the property, etc. — Financial Impact: The motion should outline the potential harm or financial burden faced by the mortgagee due to the continued delay in foreclosure. — Proposed Relief: The mortgagee should present the requested relief, which is the court's permission to proceed with foreclosure on the debtor's real property. 5. Potential Variations: Although the core purpose remains the same, there may be variations of this motion depending on certain factors. These could include: PREre or Post-Confirmation: The motion may be filed before or after the bankruptcy case is confirmed, each having its own set of requirements and implications. — Chapter of Bankruptcy: The motion's specific requirements and procedures can vary depending on the chapter of bankruptcy under which the debtor filed (Chapter 7, 11, 13, etc.). — Debtor's Intention: If the debtor intends to surrender the property or proposes an alternative plan for handling the mortgage debt, it may impact the mortgagee's motion and subsequent court decisions. In summary, a Missouri Motion in Bankruptcy Court by Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property is a critical legal request enabling a mortgage lender to seek authorization to proceed with foreclosure on a debtor's real estate during bankruptcy proceedings. Understanding the key components of this motion and its potential variations is essential for both mortgagees and debtors involved in bankruptcy cases.