Missouri UCC-1 for Personal Credit

Description

How to fill out UCC-1 For Personal Credit?

You can spend time online searching for the legal document template that meets the federal and state requirements you will need.

US Legal Forms offers thousands of legal documents that are reviewed by experts.

You can obtain or print the Missouri UCC-1 for Personal Credit from this service.

If available, utilize the Review button to view the document template as well.

- If you already have a US Legal Forms account, you may Log In and click the Download button.

- Afterward, you can complete, edit, print, or sign the Missouri UCC-1 for Personal Credit.

- Every legal document template you acquire is your property for a long time.

- To get another copy of the purchased form, go to the My documents tab and click the corresponding button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the state/city of your choice.

- Check the form description to make sure you have chosen the correct form.

Form popularity

FAQ

1 filing in Missouri is generally valid for five years from the date of filing. After this period, the filing may lapse unless renewed. This timeline is important when considering the impact of the Missouri UCC1 for Personal Credit on your financial standing. For those seeking to maintain their credit position, uslegalforms can assist you in managing renewals and updates efficiently.

Conducting a UCC search in Missouri is straightforward. You can begin by accessing the Missouri Secretary of State's website, where you'll find resources to search for UCC filings. Alternatively, uslegalforms provides tools and services that simplify this search process, making it easier for you to find relevant information. Ensuring you have accurate data is crucial for managing your personal credit effectively.

Yes, filing a UCC-1 on an individual is permitted in Missouri, as long as you adhere to the procedural requirements. This step helps in securing your interests in any personal property owned by the debtor. If you're exploring a Missouri UCC-1 for Personal Credit, this option can be valuable for your financial security. Consider using uslegalforms to guide you through the filing process for accuracy and compliance.

A UCC filing can potentially show up on a personal credit report, depending on how the filing is recorded. It is important to understand that this can affect the individual’s credit score and borrowing ability. When filing a Missouri UCC-1 for Personal Credit, think about the long-term implications for the debtor's creditworthiness. Awareness and transparency are key when entering into these agreements.

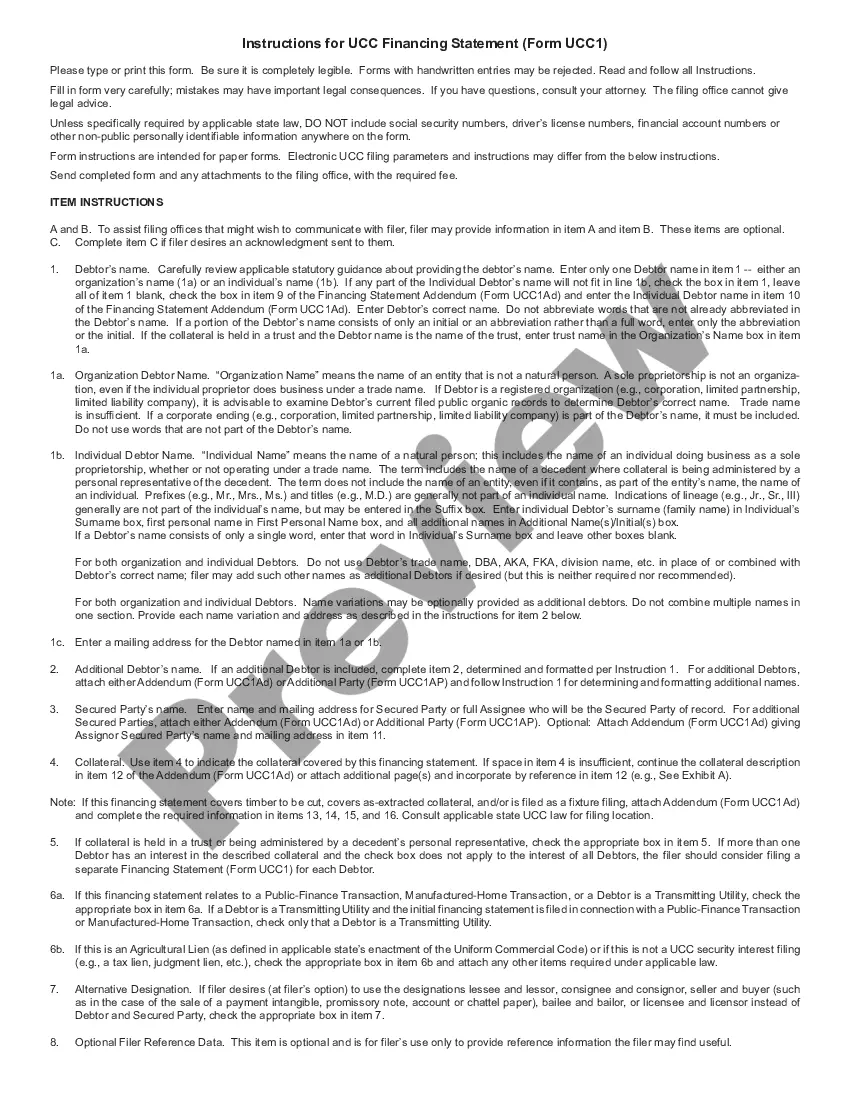

To file a UCC-1 in Missouri, you need specific information, such as the debtor's name and address, the secured party's name, and a description of the collateral. This ensures an accurate filing for your Missouri UCC-1 for Personal Credit. Proper documentation is crucial for the effectiveness of the filing, as any errors could compromise your security interest. Using platforms like uslegalforms can simplify this process.

Yes, the UCC applies to personal property, including goods, equipment, and even some intangible assets. This means that when you file a Missouri UCC-1 for Personal Credit, you can secure interests in these assets. Understanding how UCC filings relate to personal property is essential for effective credit management. It provides protection to lenders and ensures clarity in financial agreements.

Yes, you can file a UCC against an individual in Missouri. This filing can help secure your interest in an individual's personal property in relation to a debt. When considering a Missouri UCC-1 for Personal Credit, ensure you understand the implications of filing against an individual. This knowledge can safeguard your financial interests in personal lending or credit agreements.

Yes, Missouri is a UCC state, meaning it follows the Uniform Commercial Code regulations. This allows for the filing of UCC-1 forms for personal and commercial credit. If you are considering a Missouri UCC-1 for Personal Credit, you should become familiar with the process of filing and what it entails. This ensures that your interests are protected in your transactions.

Filing a Missouri UCC-1 for personal credit on yourself establishes a public record of your secured interest. This can provide you with protection against other creditors and enhance your ability to secure loans. Additionally, it demonstrates your financial responsibility, which benefits your creditworthiness.

Filling out a Missouri UCC-1 for personal credit can be broken down into simple steps. Begin with your name and address, followed by the name and address of the debtor. Next, accurately describe the collateral involved, and finally, review your information for precision before submitting the form.