This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

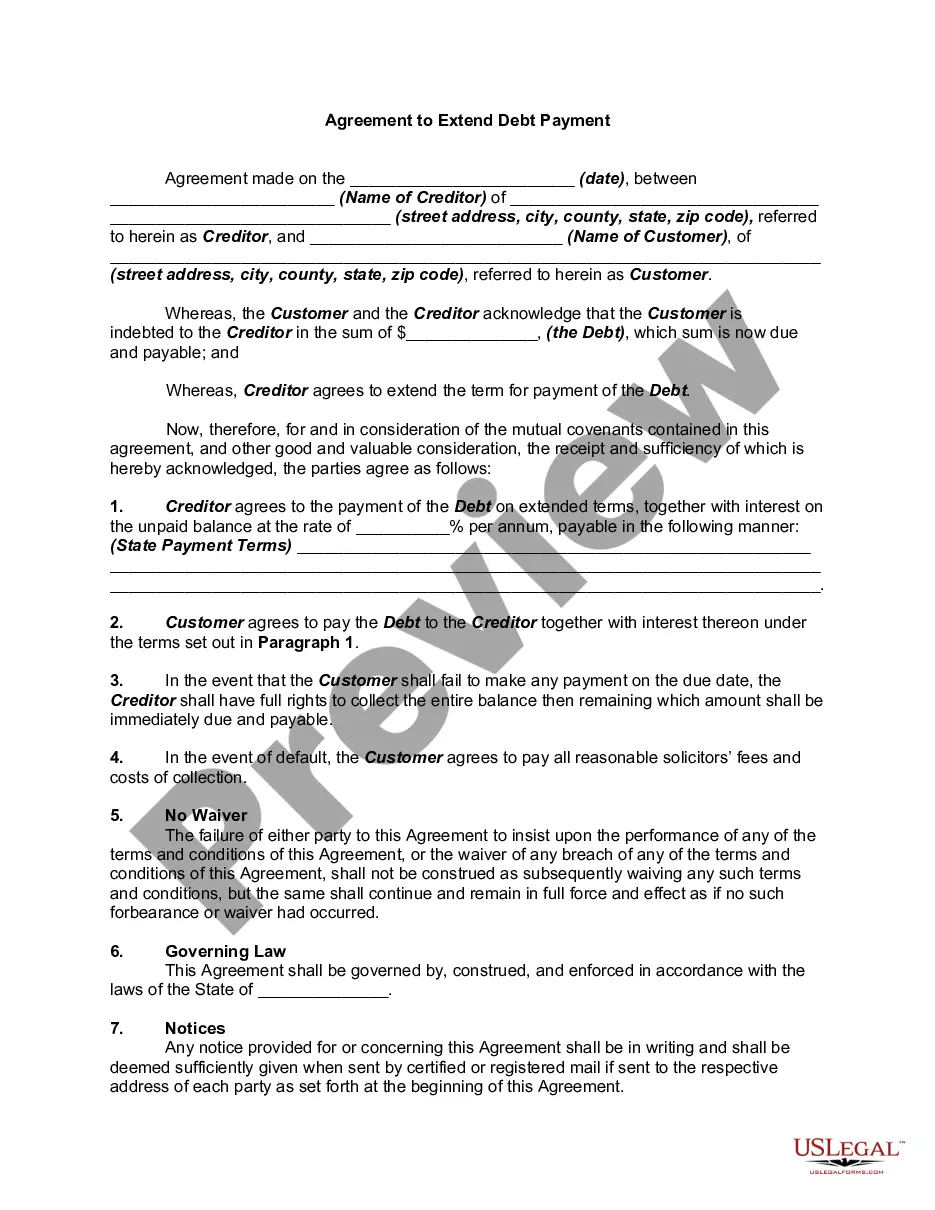

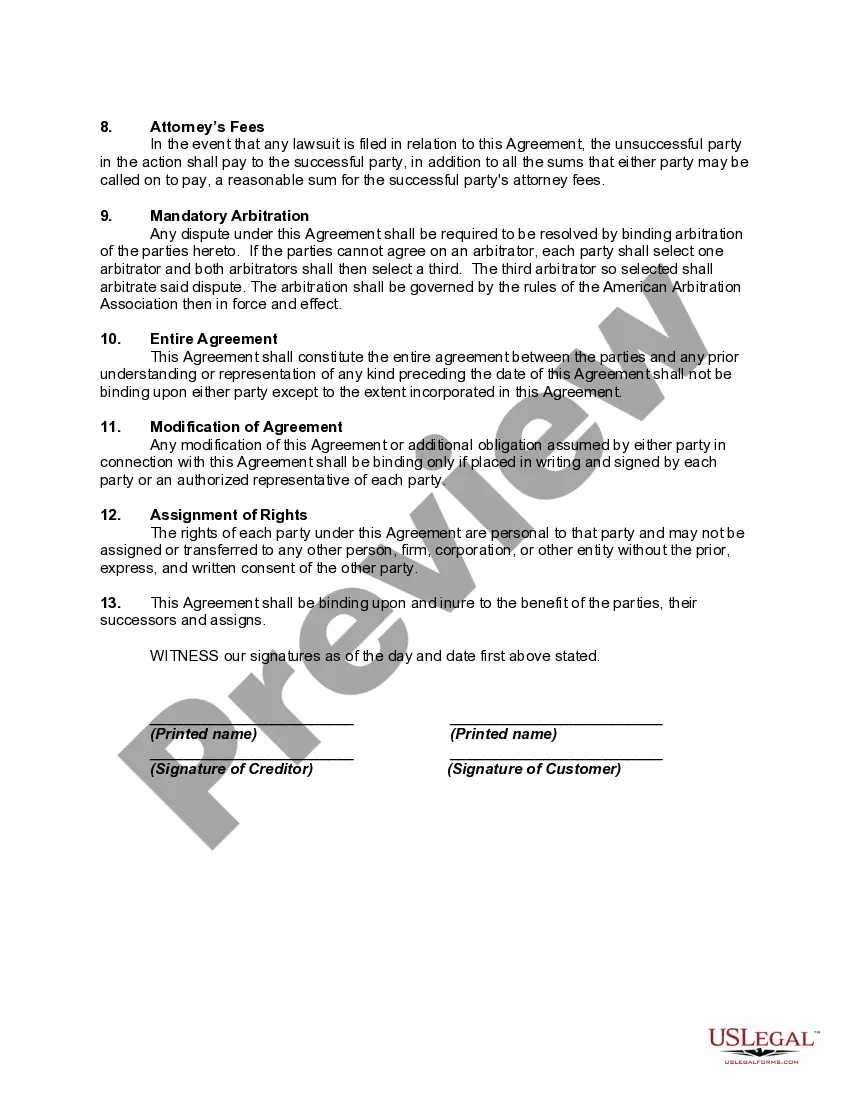

Missouri Agreement to Extend Debt Payment is a legally binding contract that allows debtors and creditors in the state of Missouri to extend the repayment period for an outstanding debt. This agreement offers parties involved a structured and mutually beneficial solution when the debtor is unable to make their scheduled debt payments on time. The purpose of a Missouri Agreement to Extend Debt Payment is to provide debtors with financial relief by granting them additional time to pay off their debts. This agreement can be vital in situations where unexpected financial hardships, such as job loss or medical emergencies, have hindered the debtor's ability to meet their financial obligations. There are various types of Missouri Agreement to Extend Debt Payment that cater to specific situations and parties involved. Some common types include: 1. Personal Debt Extension Agreement: This type of agreement is entered into between an individual debtor and a creditor, such as a credit card company or a personal loan lender. It allows for the rescheduling of payment terms, including adjusted due dates, interest rates, and installment amounts, to accommodate the debtor's financial circumstances. 2. Business Debt Extension Agreement: Primarily designed for small businesses or corporations facing financial difficulties, this agreement is made between a debtor company and its creditors. It outlines the terms of the debt extension, which may involve restructuring payment schedules and renegotiating interest rates to ease the burden on the company. 3. Mortgage Debt Extension Agreement: Specifically tailored for homeowners struggling to make their mortgage payments, this agreement is typically arranged between the borrower and the mortgage lender. It provides an opportunity to extend the repayment period, modify the interest rate, or adjust monthly installments to prevent foreclosure and allow the borrower to catch up on their payments. 4. Student Loan Debt Extension Agreement: Geared towards borrowers with outstanding student loans, this specific agreement entails negotiating with the loan service or lender to extend the loan term, revise interest rates, or modify the repayment plan. This helps borrowers who are unable to meet their monthly payments due to financial hardships, ensuring they can continue their education without defaulting on their loans. In every type of Missouri Agreement to Extend Debt Payment, the terms are laid out in detail, including the original debt amount, the extension period, any revised interest rates, and the new repayment schedule. The agreement seeks to provide a transparent and legally binding framework within which both creditors and debtors can negotiate and reach a fair and workable solution. Overall, a Missouri Agreement to Extend Debt Payment enables debtors to proactively address their financial challenges, while creditors have the opportunity to collect outstanding debts gradually, avoiding potential defaults and costly legal proceedings.