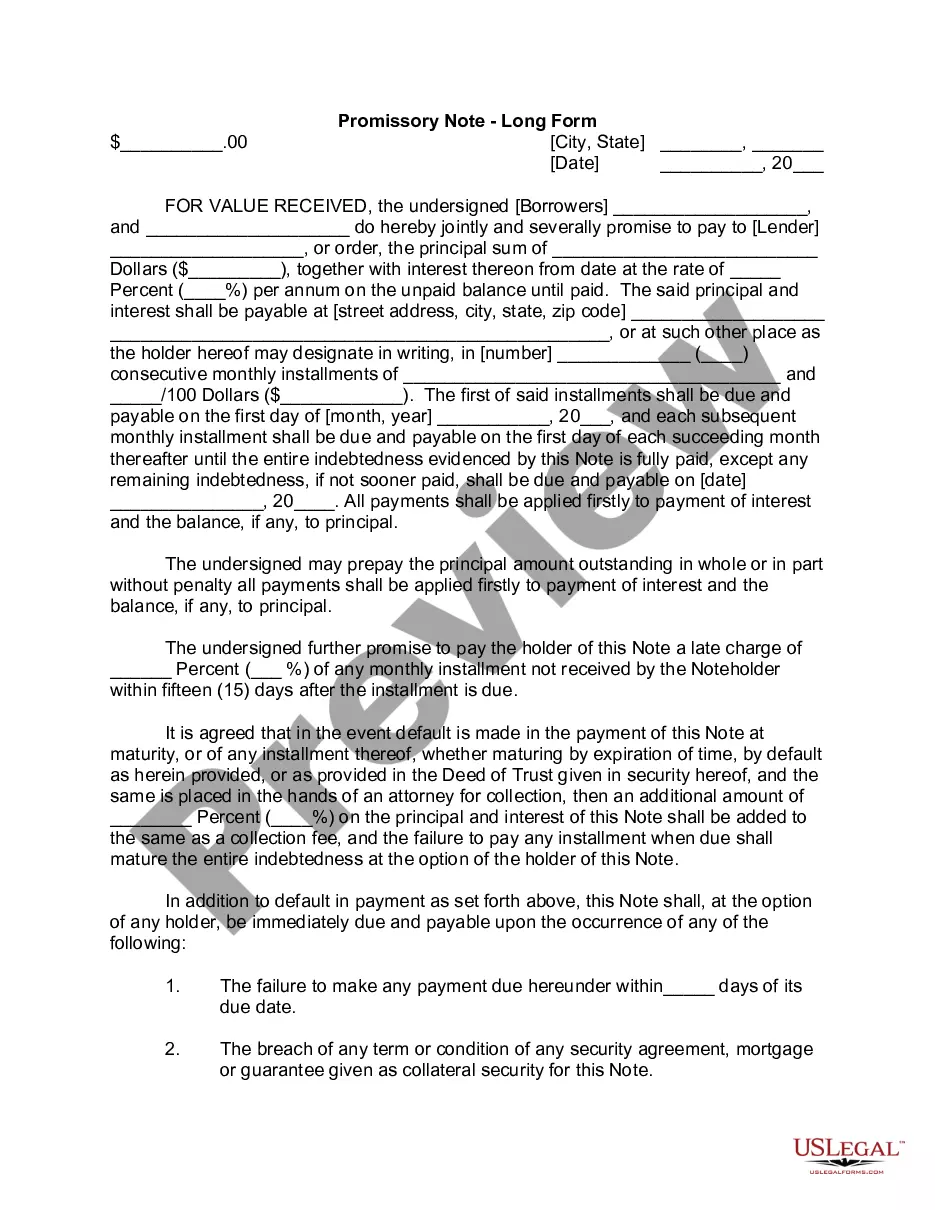

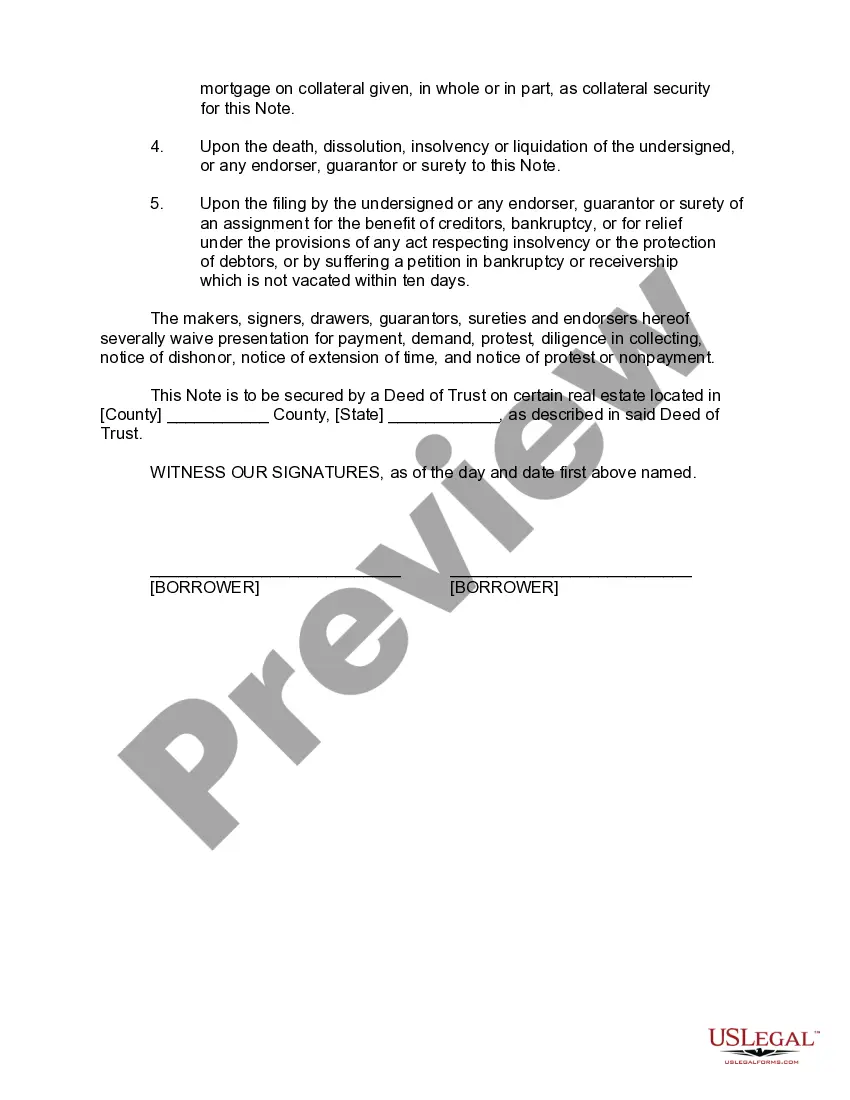

A Missouri Promissory Note — Long Form is a legally binding agreement that outlines the specific terms and conditions of a loan transaction between a lender and a borrower in the state of Missouri. This document serves as a written promise from the borrower to repay the lender a certain amount of money borrowed, along with any applicable interest or fees, within a specified time frame. Keywords: Missouri Promissory Note, long-form, legally binding, loan transaction, lender, borrower, written promise, repay, amount of money borrowed, interest, fees, specified time frame. There are various types of Missouri Promissory Note — Long Form, each designed to cater to different loan scenarios and borrower needs. Some common types include: 1. Personal Loan Promissory Note: This type of note is used for loans between individuals, such as friends or family members, where the money borrowed is typically for personal expenses or any other non-business-related purposes. 2. Business Loan Promissory Note: This note is utilized for loans between a lender and a business entity, be it a corporation, partnership, or sole proprietorship. Business loans may be used for operational expenses, expansion plans, or financing specific projects. 3. Real Estate Promissory Note: This type of note is commonly used in real estate transactions, where the borrower pledges a piece of property as collateral for the loan. It includes additional clauses to protect both parties and specifies the terms related to the property, such as foreclosure rights. 4. Student Loan Promissory Note: This note is specific to student loans, typically issued by educational institutions or private lenders, to finance higher education expenses. It outlines the terms and conditions of the loan, including repayment options, interest rates, and loan forgiveness programs. 5. Convertible Promissory Note: This note includes a provision that allows the lender to convert the loan amount into equity or ownership in the borrower's business at a later date. It is commonly used for startup companies who seek financing from angel investors or venture capitalists. It is crucial for both lenders and borrowers to carefully draft and review the terms within a Missouri Promissory Note — Long Form to ensure compliance with applicable laws and to prevent any misunderstandings or disputes in the future. Furthermore, it is highly recommended consulting a legal professional specializing in contract law to ensure that the note meets all state requirements and adequately protects the rights and interests of both parties involved.

Missouri Promissory Note - Long Form

Description

How to fill out Missouri Promissory Note - Long Form?

You are able to devote several hours on-line searching for the lawful file web template that fits the federal and state demands you want. US Legal Forms provides a huge number of lawful forms that happen to be examined by specialists. You can easily acquire or produce the Missouri Promissory Note - Long Form from the support.

If you already have a US Legal Forms profile, you may log in and then click the Acquire option. Following that, you may full, modify, produce, or indication the Missouri Promissory Note - Long Form. Every lawful file web template you acquire is your own property forever. To obtain one more copy of the obtained form, proceed to the My Forms tab and then click the related option.

Should you use the US Legal Forms web site initially, keep to the simple instructions below:

- Very first, make sure that you have selected the proper file web template for the county/metropolis of your liking. See the form explanation to make sure you have picked the right form. If readily available, take advantage of the Review option to look from the file web template at the same time.

- If you would like get one more edition of your form, take advantage of the Search field to find the web template that meets your requirements and demands.

- When you have discovered the web template you need, simply click Buy now to carry on.

- Pick the pricing prepare you need, type your accreditations, and register for your account on US Legal Forms.

- Comprehensive the deal. You can utilize your Visa or Mastercard or PayPal profile to fund the lawful form.

- Pick the formatting of your file and acquire it for your device.

- Make adjustments for your file if required. You are able to full, modify and indication and produce Missouri Promissory Note - Long Form.

Acquire and produce a huge number of file templates while using US Legal Forms web site, that offers the largest collection of lawful forms. Use specialist and state-distinct templates to deal with your small business or individual needs.