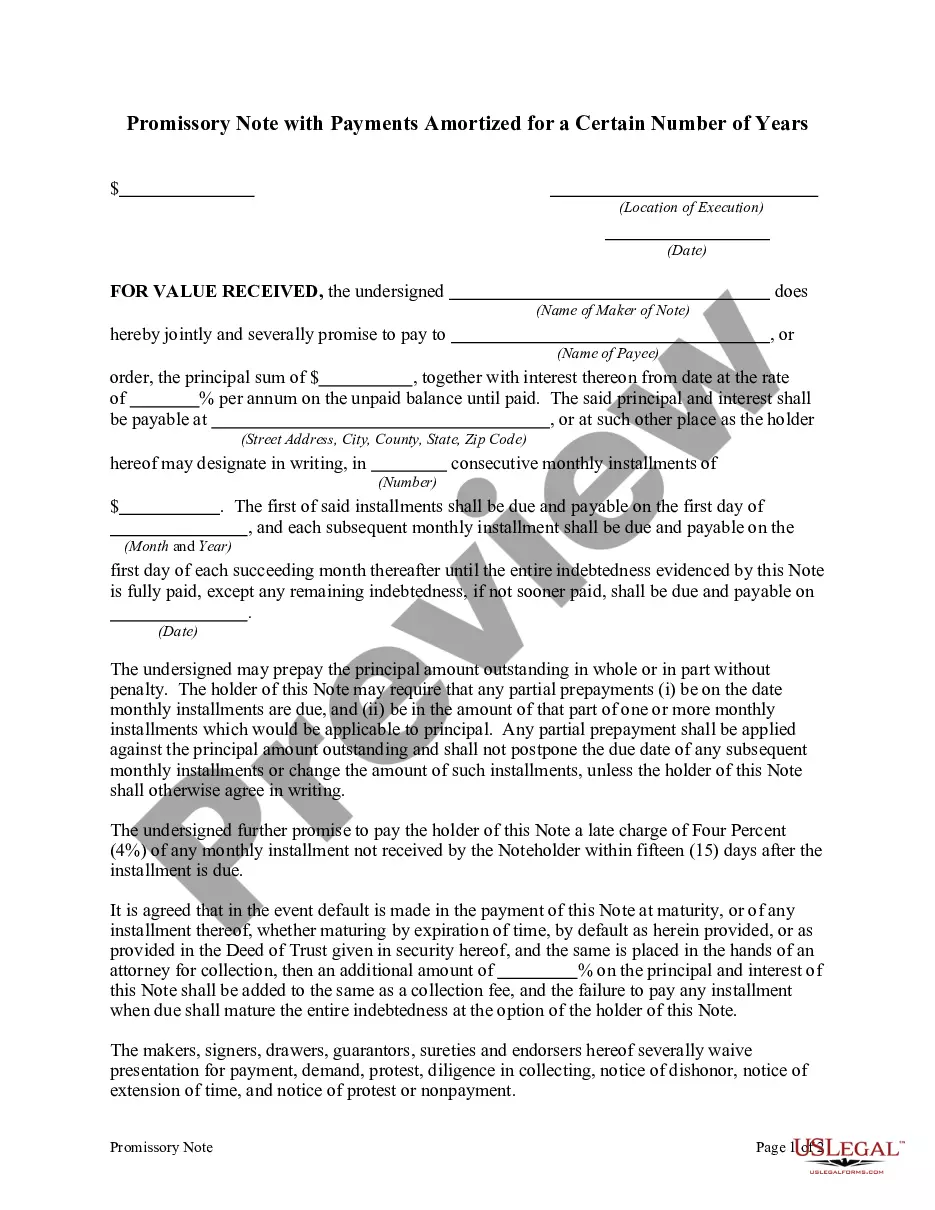

A Missouri Promissory Note with Payments Amortized for a Certain Number of Years is a legal document that outlines a borrower's promise to repay a specified amount of money borrowed from a lender, with the payments being amortized over a predetermined period. This type of promissory note is commonly used in Missouri for various financial transactions such as personal loans, business loans, or real estate transactions. In this particular type of promissory note, the loan amount, interest rate, and repayment terms are clearly defined. The loan amount refers to the principal sum borrowed by the borrower, while the interest rate determines the cost of borrowing over the amortization period. The repayment terms specify the periodic payments, typically on a monthly basis, to be made by the borrower to the lender. There are several types of Missouri Promissory Notes with Payments Amortized for a Certain Number of Years, each tailored to specific circumstances. These include: 1. Fixed-Rate Promissory Note: This type of note provides a fixed interest rate for the entire duration of the loan term. It ensures that the borrower's payments remain consistent throughout the amortization period. 2. Adjustable-Rate Promissory Note: Unlike a fixed-rate note, an adjustable-rate note has an interest rate that may fluctuate over time. The interest rate is usually tied to an index, such as the prime rate, and can be adjusted periodically based on market conditions. 3. Balloon Promissory Note: A balloon note is structured in a way that allows the borrower to make smaller regular payments for a certain period, usually followed by a larger final payment called a balloon payment. This type of note is useful when the borrower expects to have an increased cash flow in the future. 4. Installment Promissory Note: An installment note divides the repayment of the loan into equal periodic payments over the amortization period. This ensures both the principal and interest are gradually repaid over time. 5. Interest-Only Promissory Note: An interest-only note requires the borrower to make payments only towards the accrued interest for a specified period. After this period, the borrower may be required to make larger payments to cover both principal and interest. 6. Demand Promissory Note: This type of note allows the lender to demand full repayment at any time. It does not have a specific amortization period established, providing both flexibility and potential risks for the borrower. It is crucial to customize the terms of the promissory note, including the repayment schedule, interest rate, and any additional provisions, to accurately reflect the agreement between both parties. Seeking legal advice and consulting with a professional financial advisor is strongly recommended ensuring compliance with Missouri laws and to protect the interests of both the borrower and the lender.

Missouri Promissory Note with Payments Amortized for a Certain Number of Years

Description

How to fill out Missouri Promissory Note With Payments Amortized For A Certain Number Of Years?

Finding the right legitimate file format can be a battle. Of course, there are a lot of layouts available online, but how can you obtain the legitimate type you require? Make use of the US Legal Forms website. The support gives a huge number of layouts, including the Missouri Promissory Note with Payments Amortized for a Certain Number of Years, that you can use for organization and personal requirements. Every one of the forms are checked by pros and meet up with state and federal specifications.

Should you be previously signed up, log in in your profile and then click the Obtain key to have the Missouri Promissory Note with Payments Amortized for a Certain Number of Years. Make use of your profile to check through the legitimate forms you might have purchased previously. Proceed to the My Forms tab of the profile and acquire another duplicate of your file you require.

Should you be a new consumer of US Legal Forms, listed here are straightforward recommendations so that you can stick to:

- Very first, ensure you have chosen the correct type for your personal city/region. It is possible to examine the form using the Review key and read the form description to make sure this is basically the best for you.

- When the type fails to meet up with your expectations, use the Seach industry to discover the right type.

- When you are positive that the form would work, select the Purchase now key to have the type.

- Select the costs program you desire and enter the essential details. Build your profile and pay for the transaction using your PayPal profile or credit card.

- Pick the data file file format and acquire the legitimate file format in your system.

- Comprehensive, modify and print and signal the attained Missouri Promissory Note with Payments Amortized for a Certain Number of Years.

US Legal Forms may be the largest collection of legitimate forms that you will find a variety of file layouts. Make use of the service to acquire skillfully-produced paperwork that stick to state specifications.