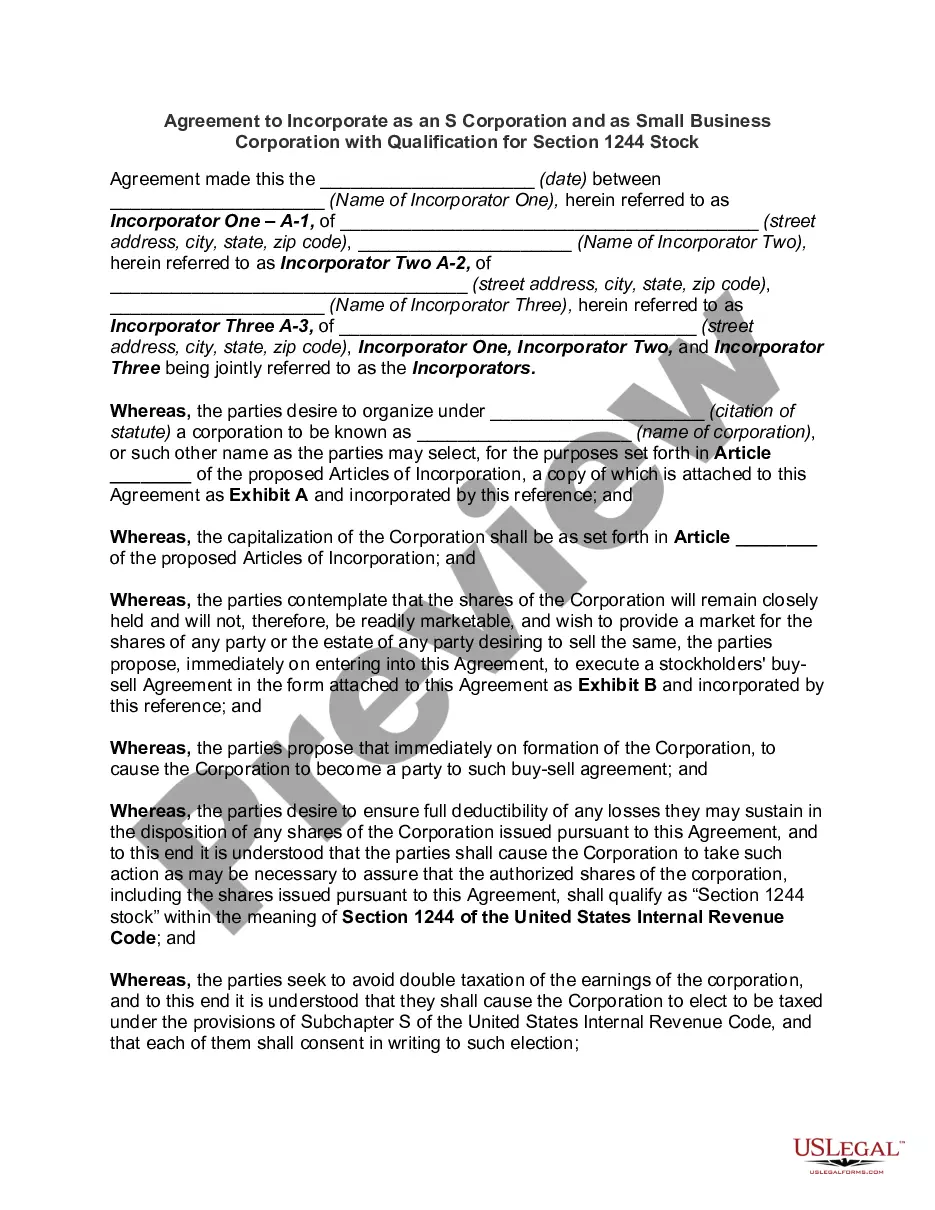

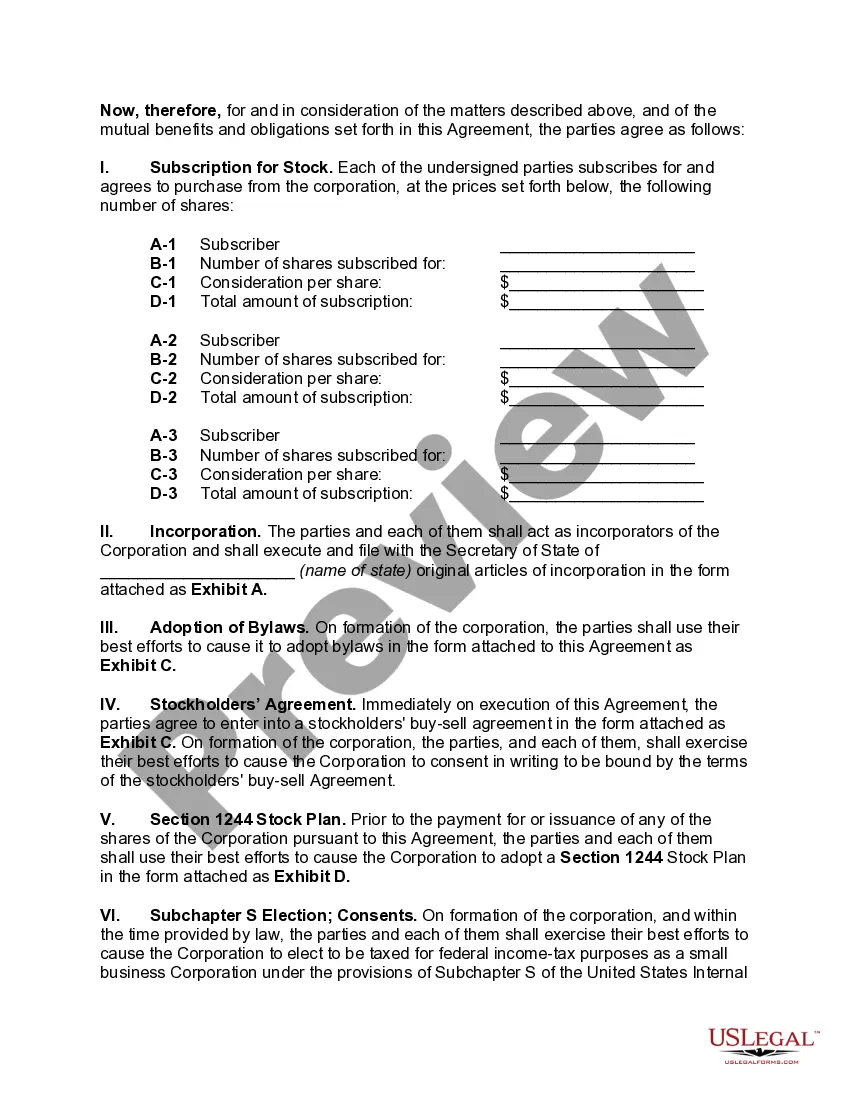

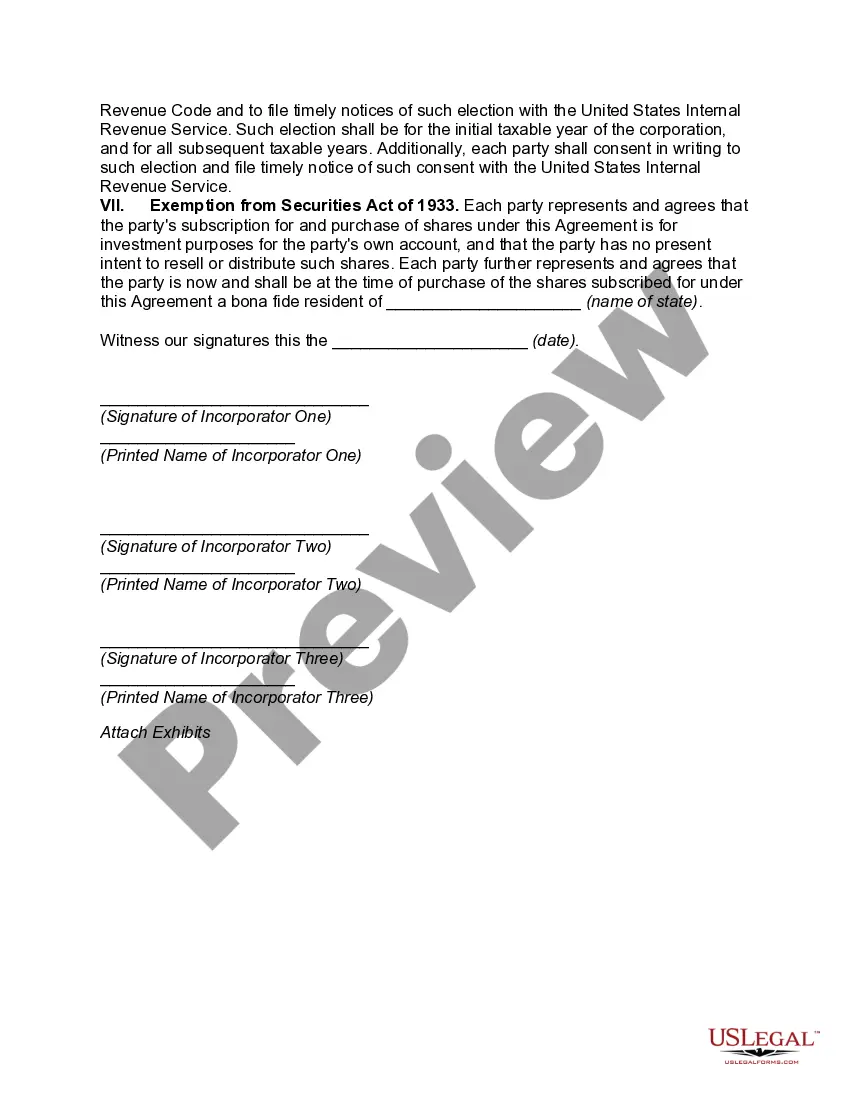

Missouri Agreement to Incorporate as an S Corp and as Small Business Corporation with Qualification for Section 1244 Stock provides a legal framework for businesses in Missouri to convert their existing structure into an S Corporation (S Corp) while simultaneously qualifying for the benefits offered by the Section 1244 Stock provision. This carefully crafted agreement ensures that the corporation meets the requirements and eligibility criteria prescribed by the state, the IRS, and the Section 1244 Stock provision. By incorporating as an S Corp, a company gains the advantage of limited liability protection while enjoying certain tax benefits. S Corporations, according to the regulations set forth by the Internal Revenue Service (IRS), are considered "pass-through" entities. This means that the corporation itself does not bear the brunt of federal income taxes, as the profits and losses pass through to the shareholders, who report them on their individual tax returns. This reduces the overall tax burden on the corporation and its shareholders, making it an attractive option for smaller businesses. Additionally, the Section 1244 Stock provision offers tax benefits specifically tailored for small businesses. This provision allows shareholders of small corporations, typically organized as C Corporations, to claim ordinary loss deductions on their tax returns when the corporation experiences a loss during the sale or disposition of their stock. This deduction is different from typical capital loss deductions, as it allows individuals to claim up to $50,000 ($100,000 if filing a joint return) of ordinary losses per year, rather than the regular $3,000 limitation. The Missouri Agreement to Incorporate as an S Corp and as Small Business Corporation with Qualification for Section 1244 Stock outlines the necessary steps, obligations, and responsibilities for a business to complete this conversion successfully. It includes provisions for amending the existing articles of incorporation or drafting new articles to incorporate as an S Corp. The agreement also details the process for shareholders to qualify their stock under the Section 1244 provision. Different variations of the Missouri Agreement to Incorporate as an S Corp and as Small Business Corporation with Qualification for Section 1244 Stock may exist depending on the specific needs and circumstances of different businesses. Some possible variations may include agreements designed for businesses operating in specialized industries, such as technology or healthcare, or for businesses with multiple shareholders. In conclusion, the Missouri Agreement to Incorporate as an S Corp and as Small Business Corporation with Qualification for Section 1244 Stock serves as a comprehensive legal document that enables businesses in Missouri to transform their structure into an S Corp while also capitalizing on the tax benefits offered by the Section 1244 Stock provision. Engaging in this conversion may provide businesses with significant advantages, ensuring limited liability protection, reduced tax burdens, and potential deductions for shareholders in the case of stock losses.

Missouri Agreement to Incorporate as an S Corp and as Small Business Corporation with Qualification for Section 1244 Stock

Description

How to fill out Missouri Agreement To Incorporate As An S Corp And As Small Business Corporation With Qualification For Section 1244 Stock?

Choosing the right lawful record web template might be a struggle. Obviously, there are a variety of layouts available online, but how will you obtain the lawful type you require? Use the US Legal Forms site. The service provides a huge number of layouts, like the Missouri Agreement to Incorporate as an S Corp and as Small Business Corporation with Qualification for Section 1244 Stock, which you can use for company and personal requires. Every one of the varieties are examined by professionals and meet up with state and federal needs.

If you are previously signed up, log in to your bank account and click on the Obtain key to have the Missouri Agreement to Incorporate as an S Corp and as Small Business Corporation with Qualification for Section 1244 Stock. Make use of your bank account to appear through the lawful varieties you may have ordered earlier. Go to the My Forms tab of the bank account and acquire an additional backup in the record you require.

If you are a new customer of US Legal Forms, listed below are simple guidelines so that you can stick to:

- Very first, make certain you have selected the right type to your city/county. You are able to examine the shape using the Preview key and look at the shape information to ensure it is the best for you.

- When the type is not going to meet up with your expectations, make use of the Seach industry to discover the correct type.

- When you are positive that the shape is proper, click on the Buy now key to have the type.

- Select the rates prepare you would like and type in the required information and facts. Create your bank account and pay for your order making use of your PayPal bank account or charge card.

- Opt for the submit structure and down load the lawful record web template to your product.

- Comprehensive, edit and print and indicator the acquired Missouri Agreement to Incorporate as an S Corp and as Small Business Corporation with Qualification for Section 1244 Stock.

US Legal Forms is definitely the largest catalogue of lawful varieties that you will find numerous record layouts. Use the company to down load skillfully-produced papers that stick to status needs.