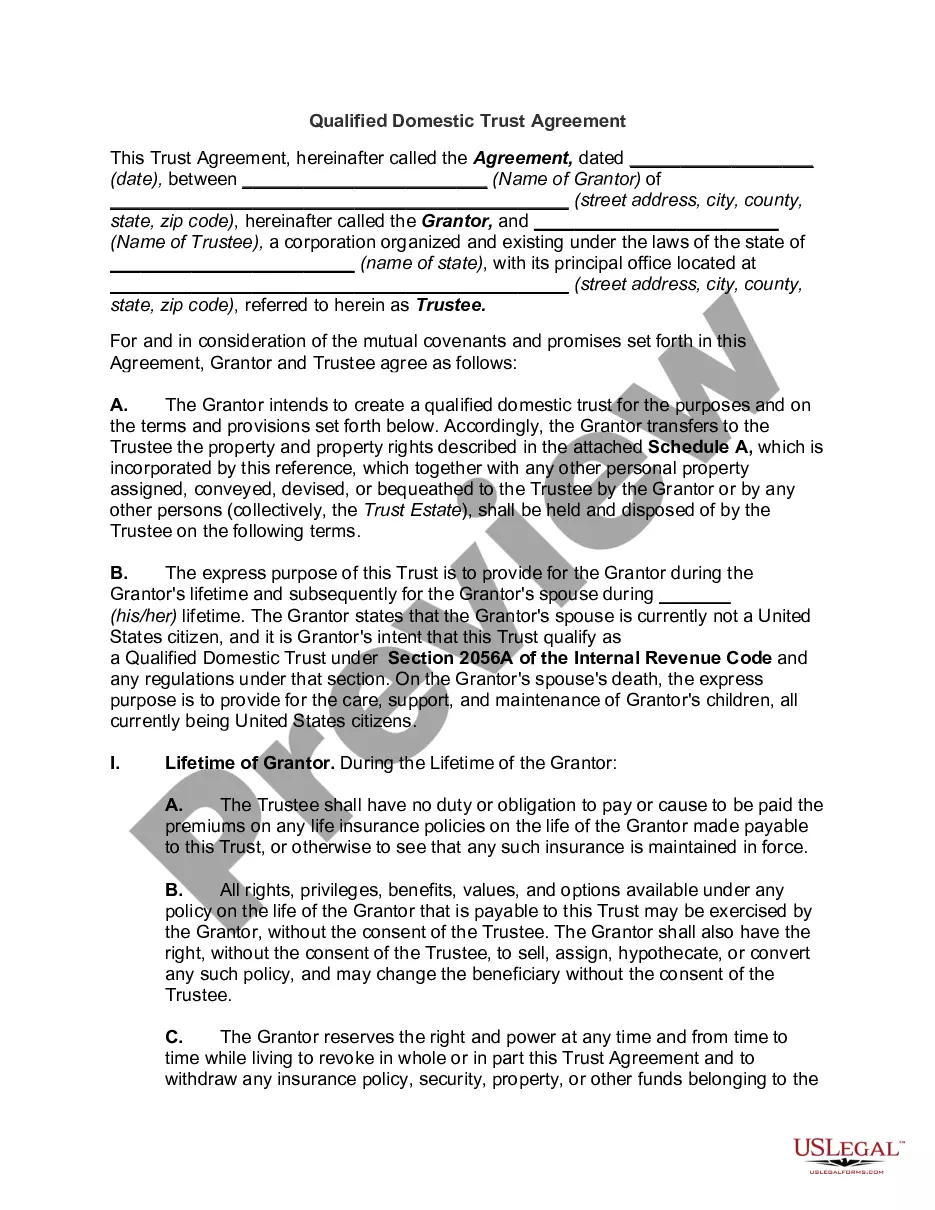

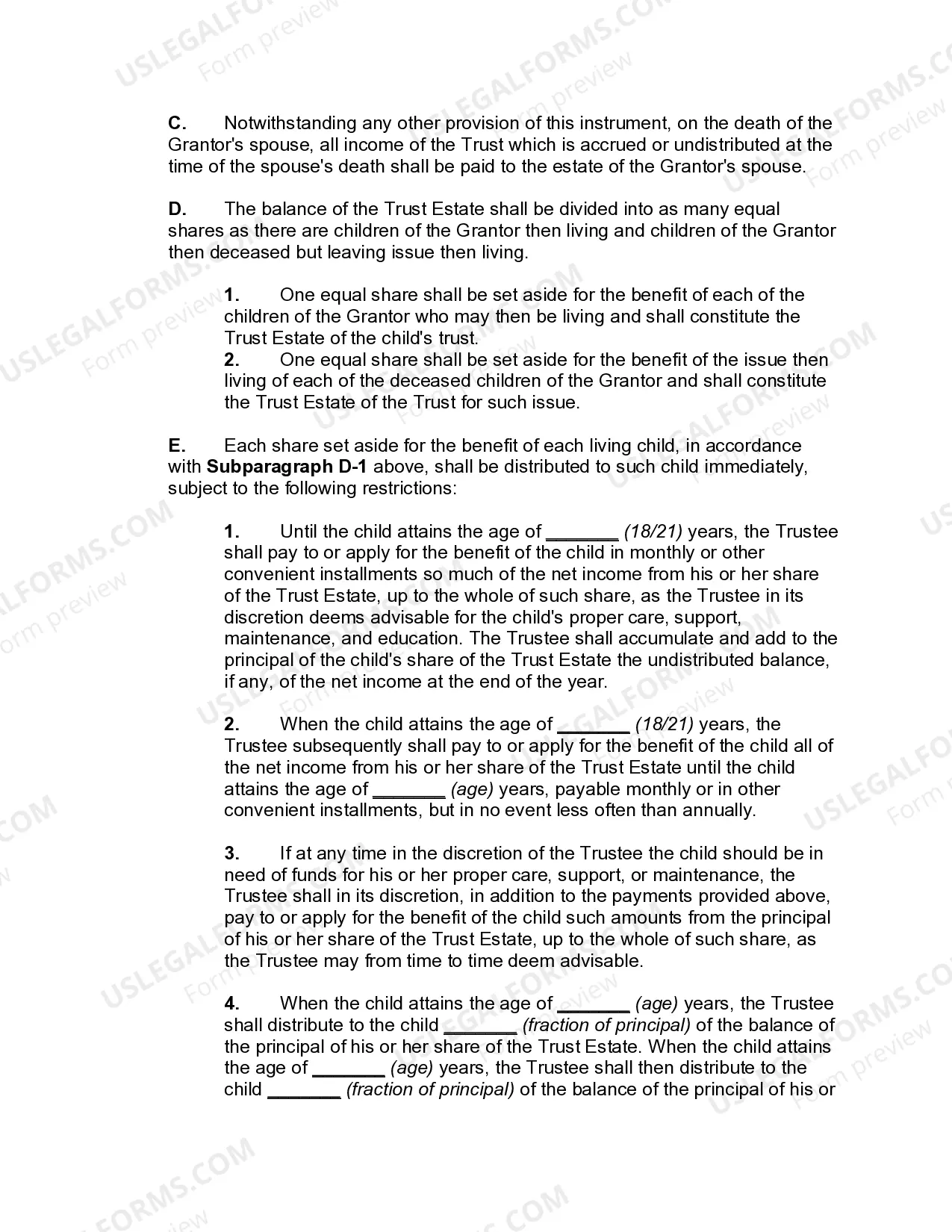

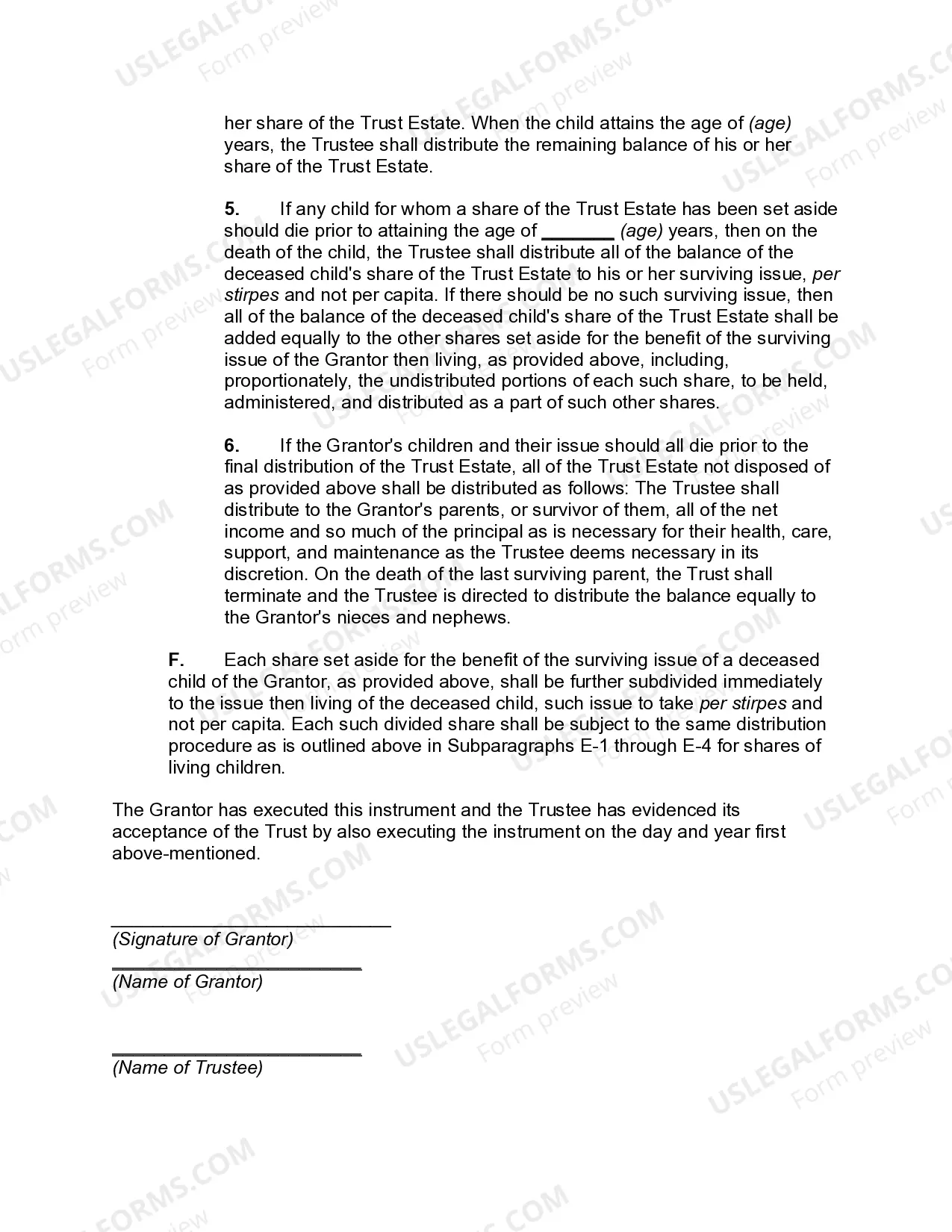

A Missouri Qualified Domestic Trust Agreement (MEDIA) is a legal document that allows a non-citizen surviving spouse to be the beneficiary of a trust while deferring the estate tax on assets transferred to the trust upon the death of the U.S. citizen spouse. Madras are specifically designed for couples where one spouse is a non-citizen and may not be eligible for the marital deduction, which normally allows for the tax-free transfer of assets between spouses. This trust agreement is governed by Missouri state laws and must meet certain requirements to qualify as a "Qualified Domestic Trust" under the Internal Revenue Code. The primary purpose of this agreement is to preserve the marital deduction and defer estate tax until the non-citizen spouse's death or when the trust assets are distributed. There are several types of Missouri Qualified Domestic Trust Agreements: 1. Irrevocable Qualified Domestic Trust (IDT): This type of MEDIA is made irrevocable by the granter, meaning that the trust terms cannot be changed once the agreement is executed. 2. Revocable Qualified Domestic Trust (RDT): Unlike the IDT, a Revocable DDT allows the granter to modify or revoke the trust during their lifetime. However, the trust becomes irrevocable upon the granter's death. 3. Marital Qualified Domestic Trust (MDT): This type of MEDIA is specifically designed for the non-citizen surviving spouse to receive income generated by the trust during their lifetime. After the spouse's death, the trust assets may be distributed to other beneficiaries, such as children or other family members. 4. General Qualified Domestic Trust (GDT): A General DDT is a more flexible type of trust that allows both the non-citizen surviving spouse and other beneficiaries to receive income and principal distributions from the trust. This type of MEDIA provides greater control over the trust assets and their distribution. It is essential to consult with an experienced estate planning attorney familiar with Missouri laws when creating a Qualified Domestic Trust Agreement. This ensures compliance with the specific requirements, maximizes the tax benefits, and protects the interests of both the U.S. citizen and non-citizen spouses.

Missouri Qualified Domestic Trust Agreement

Description

How to fill out Missouri Qualified Domestic Trust Agreement?

Are you in the place that you need documents for possibly company or personal purposes virtually every working day? There are plenty of legal file web templates accessible on the Internet, but getting types you can rely is not simple. US Legal Forms delivers thousands of kind web templates, much like the Missouri Qualified Domestic Trust Agreement, which can be written to satisfy state and federal demands.

In case you are already acquainted with US Legal Forms website and also have a free account, simply log in. Following that, you are able to acquire the Missouri Qualified Domestic Trust Agreement format.

If you do not come with an account and wish to begin using US Legal Forms, abide by these steps:

- Get the kind you will need and ensure it is for that correct metropolis/area.

- Utilize the Review option to check the form.

- Read the outline to actually have selected the proper kind.

- In case the kind is not what you are searching for, utilize the Look for industry to find the kind that meets your requirements and demands.

- When you obtain the correct kind, click Purchase now.

- Select the costs strategy you want, submit the desired information and facts to make your money, and purchase the order with your PayPal or credit card.

- Select a convenient document file format and acquire your copy.

Locate every one of the file web templates you may have bought in the My Forms menus. You can obtain a additional copy of Missouri Qualified Domestic Trust Agreement at any time, if possible. Just click on the needed kind to acquire or produce the file format.

Use US Legal Forms, by far the most substantial selection of legal forms, to conserve efforts and stay away from blunders. The support delivers skillfully made legal file web templates which you can use for a selection of purposes. Make a free account on US Legal Forms and begin producing your lifestyle easier.

Form popularity

FAQ

A qualified domestic trust (QDOT) is a special kind of trust that allows taxpayers who survive a deceased spouse to take the marital deduction on estate taxes, even if the surviving spouse is not a U.S. citizen.

The unlimited marital deduction is a provision in the U.S. Federal Estate and Gift Tax Law that allows an individual to transfer an unrestricted amount of assets to their spouse at any time, including at the death of the transferor, free from tax.

A domestic trust is any trust in which the following conditions are met: (1) A court within the U.S. must be able to exercise primary supervision over the administration of the trust. (2) One or more U.S. persons have the authority to control all substantial decisions of the trust.

For estates that are less than those amounts, no QDOT is needed since no federal estate tax would be due. However, for estates greater than those amounts, no marital deduction will be allowed if the surviving spouse is not a U.S. citizen and does not become a citizen by the time that the estate tax return is filed.

A QDOT (Qualified Domestic Trust) is a trust for the benefit of a surviving non-citizen spouse that defers the federal estate tax following the death of the first spouse. A Qualified Domestic Trust defers the federal estate tax because it qualifies for the unlimited marital deduction.

A Qualified Terminable Interest Property (QTIP) trust is a type of marital trust. They are often used when a grantor has children from different marriages. The surviving spouse still serves as the initial beneficiary.

Tax Consequences The QDOT is generally taxed as a simple trust for income tax purposes. This means that when the trust earns income, it MUST be distributed to the surviving spouse. The surviving spouse is then required to pay the income tax on that income based upon the surviving spouses own tax rates.

A Resident Estate or Trust is: 1) The estate of a decedent who at his or her death was domiciled in this state; or 2) A trust that was created by a will of a decedent who at his or her death was domiciled in this state, and has at least one income beneficiary who, on the last day of the taxable year, was a resident of