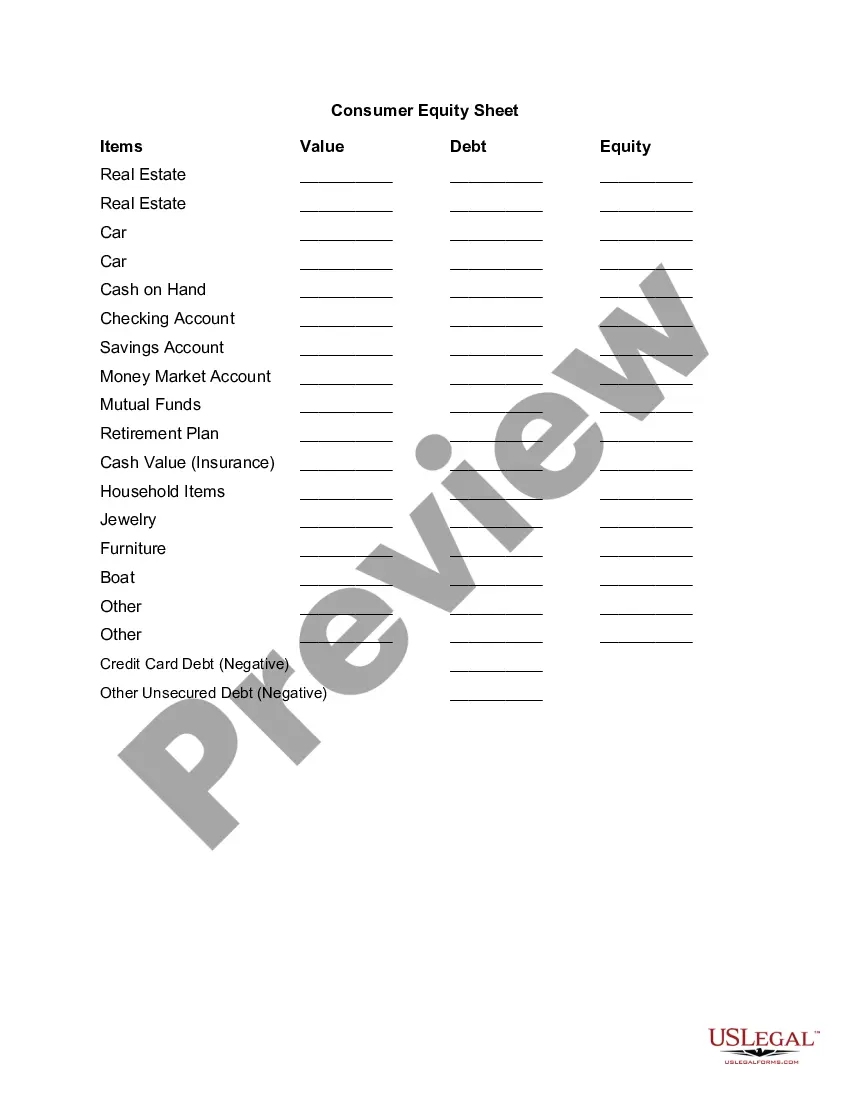

The Missouri Consumer Equity Sheet is a crucial financial document that provides a comprehensive overview of an individual's financial status and equity. It serves as a tool to assess one's net worth and evaluate their financial health. The Consumer Equity Sheet outlines the various assets, liabilities, and equity possessed by a consumer in the state of Missouri. It includes relevant financial information such as real estate holdings, vehicles owned, savings and investment accounts, retirement plans, and personal property of significant value. Furthermore, the Consumer Equity Sheet includes liabilities such as mortgages, loans, credit card debt, and any other outstanding financial obligations. By subtracting the total liabilities from the total assets, the net equity of an individual can be calculated, presenting an accurate representation of their financial position. The Missouri Consumer Equity Sheet plays a critical role in various financial situations, including mortgage applications, loan approvals, divorce proceedings, and bankruptcy cases. Lenders, creditors, and legal entities utilize this document to gauge the financial stability, creditworthiness, and ability to repay debts of an individual. Different types of Missouri Consumer Equity Sheets may exist depending on the specific purpose they serve. Some common variations include: 1. Real Estate Consumer Equity Sheet: This form focuses primarily on real estate assets and liabilities, including details about property ownership, mortgages, and rental income. 2. Automobile Consumer Equity Sheet: This type of equity sheet concentrates on vehicles owned by an individual, encompassing information such as make, model, year, outstanding car loans, and the market value of each vehicle. 3. Retirement Consumer Equity Sheet: This variation emphasizes the individual's retirement savings and investment accounts, retirement plans, and other pension benefits, providing insights into their long-term financial security. 4. Business Consumer Equity Sheet: This type of equity sheet is designed for entrepreneurs and small business owners, outlining the equity in their business, business assets, liabilities, and financial standing. Ultimately, the Missouri Consumer Equity Sheet acts as a comprehensive snapshot of an individual's financial position, aiding in financial decision-making and serving as evidence in various legal and credit-related scenarios. It is a powerful tool that assists both consumers and financial institutions in assessing financial stability, worthiness, and planning for the future.

Missouri Consumer Equity Sheet

Description

How to fill out Missouri Consumer Equity Sheet?

Discovering the right legitimate record template could be a battle. Needless to say, there are a variety of web templates available online, but how do you find the legitimate form you need? Use the US Legal Forms web site. The support provides 1000s of web templates, such as the Missouri Consumer Equity Sheet, that you can use for enterprise and personal needs. All the types are examined by professionals and satisfy federal and state needs.

Should you be previously listed, log in to the accounts and then click the Down load option to have the Missouri Consumer Equity Sheet. Utilize your accounts to check from the legitimate types you might have acquired formerly. Proceed to the My Forms tab of your accounts and have an additional backup of your record you need.

Should you be a fresh consumer of US Legal Forms, here are easy recommendations for you to comply with:

- Very first, be sure you have selected the right form for the town/region. You are able to look through the shape utilizing the Review option and browse the shape information to guarantee this is the best for you.

- In the event the form is not going to satisfy your needs, take advantage of the Seach industry to find the correct form.

- Once you are sure that the shape is acceptable, click on the Acquire now option to have the form.

- Opt for the costs strategy you want and enter in the necessary info. Create your accounts and purchase an order using your PayPal accounts or charge card.

- Pick the file formatting and download the legitimate record template to the system.

- Total, change and produce and indication the received Missouri Consumer Equity Sheet.

US Legal Forms is the biggest catalogue of legitimate types where you will find a variety of record web templates. Use the service to download appropriately-made paperwork that comply with status needs.