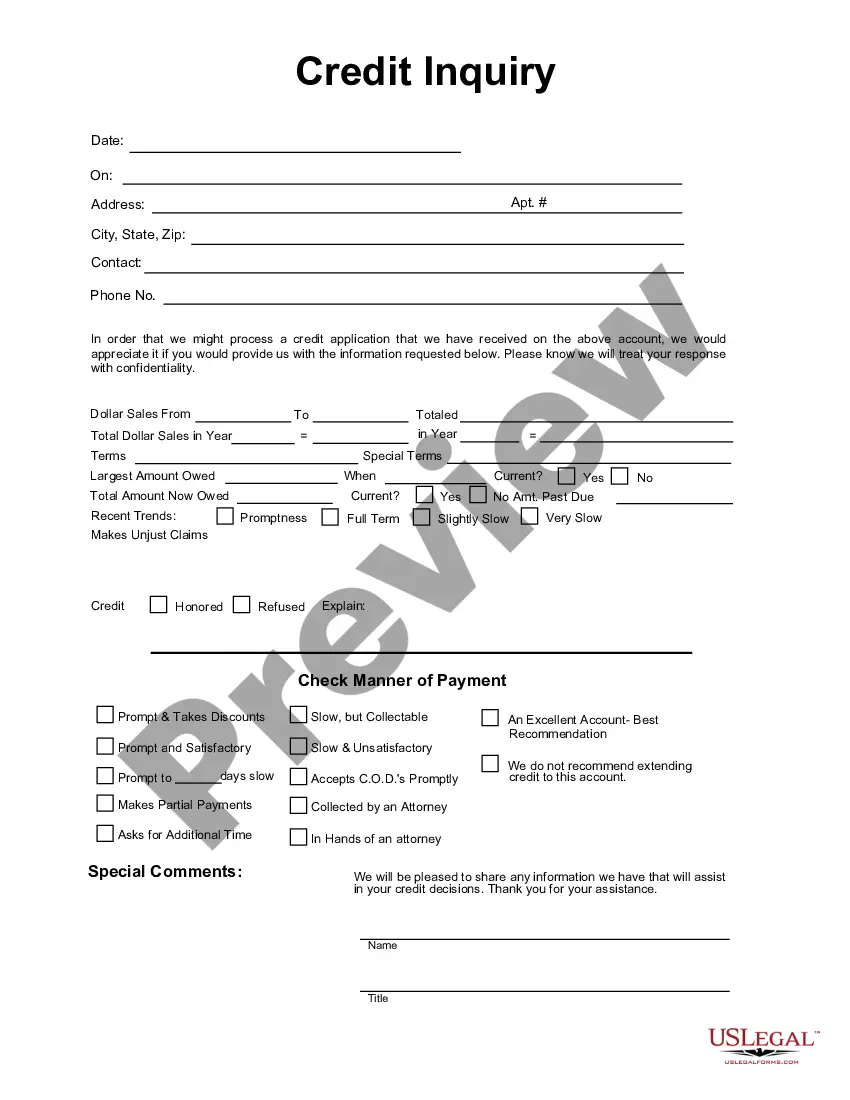

Missouri Credit Inquiry refers to the process in which individuals or organizations request access to someone's credit information in the state of Missouri. It allows potential creditors, lenders, or other authorized parties to assess an individual's creditworthiness before extending credit or entering into financial agreements. The credit inquiry provides essential details about the person's credit history, including their payment behavior, outstanding debts, and past credit performance. There are primarily two types of credit inquiries conducted in Missouri: 1. Hard Credit Inquiry: A hard credit inquiry is initiated when an individual applies for credit, such as a loan, credit card, or mortgage. These inquiries are typically conducted by financial institutions, landlords, employers, or other authorized entities seeking to evaluate the applicant's creditworthiness. Each hard inquiry is recorded on the individual's credit report and may slightly impact their credit score, particularly if multiple inquiries are made within a short period. 2. Soft Credit Inquiry: A soft credit inquiry is often performed for background checks, pre-approvals, or when individuals request their own credit report. Soft inquiries do not affect the credit score and are usually conducted by the individual themselves, potential employers, or companies offering promotional offers or credit monitoring services. Insurance companies may also conduct soft inquiries while determining premiums or eligibility. In Missouri, credit inquiries are governed by the Fair Credit Reporting Act (FCRA), which outlines the permissible purposes for which credit information can be accessed. The FCRA also ensures that individuals are aware of who has accessed their credit information and grants them the right to dispute any inaccurate or outdated information on their credit report. Missouri Credit Inquiry is essential for both individuals and businesses as it helps in making informed financial decisions, mitigating risks, and ensuring responsible lending practices. It enables lenders to evaluate an individual's creditworthiness, interest rates, and loan terms, while also allowing consumers to monitor and improve their credit health.

Missouri Credit Inquiry

Description

How to fill out Missouri Credit Inquiry?

Are you currently in the place in which you will need documents for both enterprise or person reasons just about every day? There are tons of legitimate file themes accessible on the Internet, but discovering types you can trust isn`t easy. US Legal Forms delivers thousands of type themes, much like the Missouri Credit Inquiry, that are written to fulfill federal and state requirements.

If you are already familiar with US Legal Forms website and also have your account, just log in. Following that, you may download the Missouri Credit Inquiry design.

Unless you provide an profile and need to begin using US Legal Forms, follow these steps:

- Discover the type you want and ensure it is for that proper city/area.

- Take advantage of the Review key to examine the shape.

- Look at the description to ensure that you have chosen the right type.

- When the type isn`t what you are seeking, use the Lookup discipline to obtain the type that suits you and requirements.

- Whenever you find the proper type, just click Get now.

- Pick the rates plan you need, fill out the required info to generate your account, and buy an order utilizing your PayPal or Visa or Mastercard.

- Pick a handy file format and download your version.

Get each of the file themes you may have purchased in the My Forms food list. You can obtain a extra version of Missouri Credit Inquiry whenever, if required. Just go through the required type to download or printing the file design.

Use US Legal Forms, by far the most substantial selection of legitimate types, to save some time and prevent mistakes. The service delivers expertly created legitimate file themes which you can use for an array of reasons. Generate your account on US Legal Forms and start creating your life a little easier.