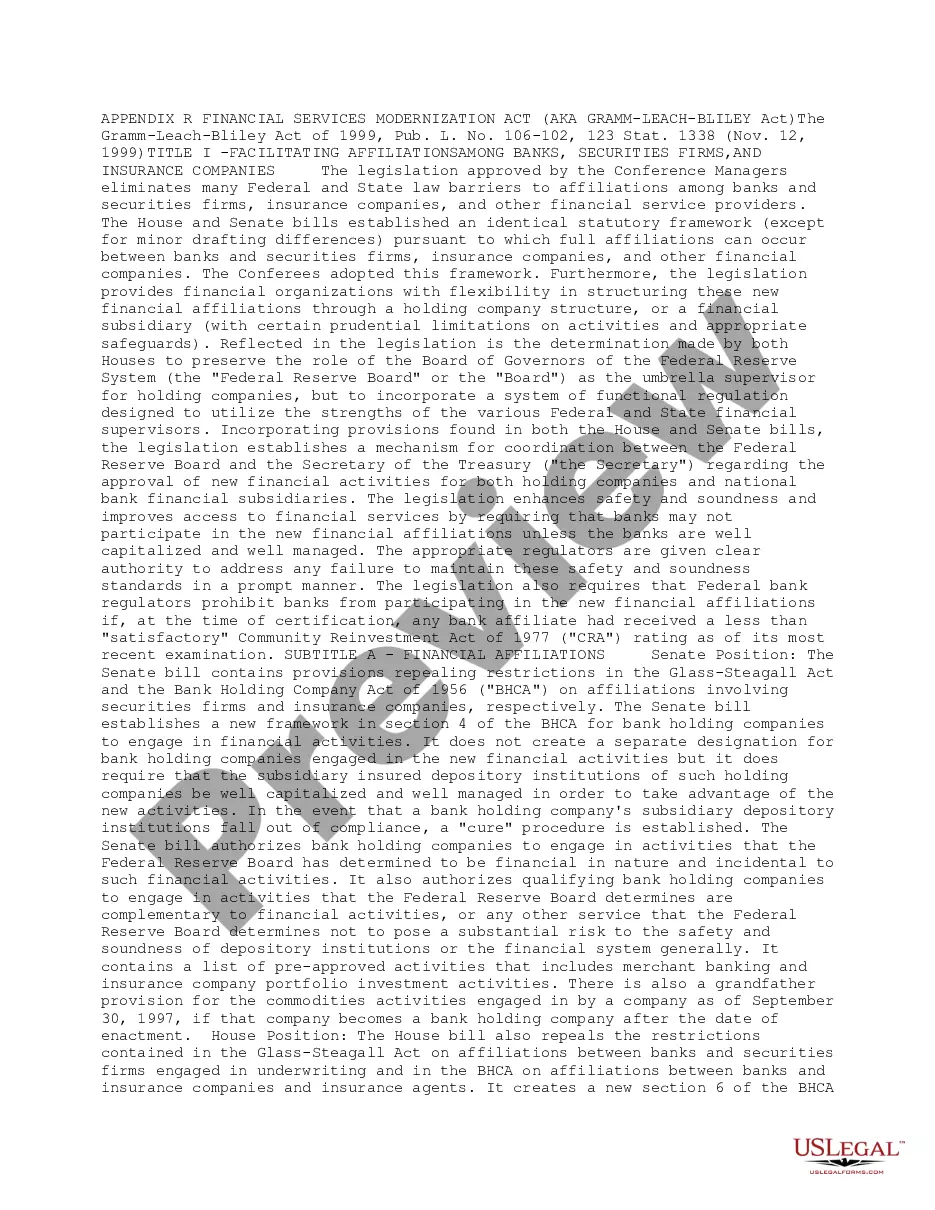

Full text and statutory guidelines for the Financial Services Modernization Act (Gramm-Leach-Bliley Act)

The Missouri Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant federal law that aims to protect consumers' financial privacy and facilitate competition among financial service providers. Enacted in 1999, this act has had a lasting impact on the financial services industry. The ALBA encompasses a wide range of regulations and provisions that affect institutions such as banks, securities firms, insurance companies, and other financial service providers. It consists of several key components designed to address various aspects of financial services and consumer privacy: 1. Privacy Requirements: Under the ALBA, financial institutions are required to inform customers about their privacy policies and how their personal information is collected, used, and shared. Customers must also be given the opportunity to opt out of sharing their information with non-affiliated third parties. 2. Disclosure Requirements: Financial institutions must provide customers with clear and accurate disclosures about their services, including terms and conditions, fees, and any potential risks associated with the financial products or services being offered. 3. Safeguards Provision: The ALBA mandates that financial institutions implement security measures to protect customers' personal information from unauthorized access or use. These measures include the development and implementation of comprehensive information security programs. 4. Pretexting Prohibition: The act makes it illegal for individuals to obtain financial information under false pretenses, a practice known as pretexting. This provision helps prevent fraudulent access to sensitive personal data. 5. Repealed Glass-Steagall Act's Separation: The ALBA repealed certain provisions of the Glass-Steagall Act of 1933, allowing banks to engage in a wider array of financial activities such as securities underwriting, mutual fund management, and insurance distributions. This contributed to the integration of different types of financial services within a single institution. While the ALBA is a federal law, it is applicable in Missouri as it applies to financial institutions operating within the state. There are no variations or specific types of the Missouri Financial Services Modernization Act; however, Missouri-based financial institutions must comply with the provisions outlined in the federal Gramm-Leach-Bliley Act to ensure the protection of consumer privacy rights and enhanced competition in the financial services sector. In summary, the Missouri Financial Services Modernization Act, commonly referred to as the Gramm-Leach-Bliley Act (ALBA), is a federal law aimed at safeguarding consumer privacy and promoting competition in the financial services industry. Its provisions encompass privacy requirements, disclosure requirements, safeguards provision, pretexting prohibition, and the elimination of certain restrictions on financial activities. Financial institutions operating in Missouri must abide by the ALBA to ensure compliance with the federal law.The Missouri Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant federal law that aims to protect consumers' financial privacy and facilitate competition among financial service providers. Enacted in 1999, this act has had a lasting impact on the financial services industry. The ALBA encompasses a wide range of regulations and provisions that affect institutions such as banks, securities firms, insurance companies, and other financial service providers. It consists of several key components designed to address various aspects of financial services and consumer privacy: 1. Privacy Requirements: Under the ALBA, financial institutions are required to inform customers about their privacy policies and how their personal information is collected, used, and shared. Customers must also be given the opportunity to opt out of sharing their information with non-affiliated third parties. 2. Disclosure Requirements: Financial institutions must provide customers with clear and accurate disclosures about their services, including terms and conditions, fees, and any potential risks associated with the financial products or services being offered. 3. Safeguards Provision: The ALBA mandates that financial institutions implement security measures to protect customers' personal information from unauthorized access or use. These measures include the development and implementation of comprehensive information security programs. 4. Pretexting Prohibition: The act makes it illegal for individuals to obtain financial information under false pretenses, a practice known as pretexting. This provision helps prevent fraudulent access to sensitive personal data. 5. Repealed Glass-Steagall Act's Separation: The ALBA repealed certain provisions of the Glass-Steagall Act of 1933, allowing banks to engage in a wider array of financial activities such as securities underwriting, mutual fund management, and insurance distributions. This contributed to the integration of different types of financial services within a single institution. While the ALBA is a federal law, it is applicable in Missouri as it applies to financial institutions operating within the state. There are no variations or specific types of the Missouri Financial Services Modernization Act; however, Missouri-based financial institutions must comply with the provisions outlined in the federal Gramm-Leach-Bliley Act to ensure the protection of consumer privacy rights and enhanced competition in the financial services sector. In summary, the Missouri Financial Services Modernization Act, commonly referred to as the Gramm-Leach-Bliley Act (ALBA), is a federal law aimed at safeguarding consumer privacy and promoting competition in the financial services industry. Its provisions encompass privacy requirements, disclosure requirements, safeguards provision, pretexting prohibition, and the elimination of certain restrictions on financial activities. Financial institutions operating in Missouri must abide by the ALBA to ensure compliance with the federal law.