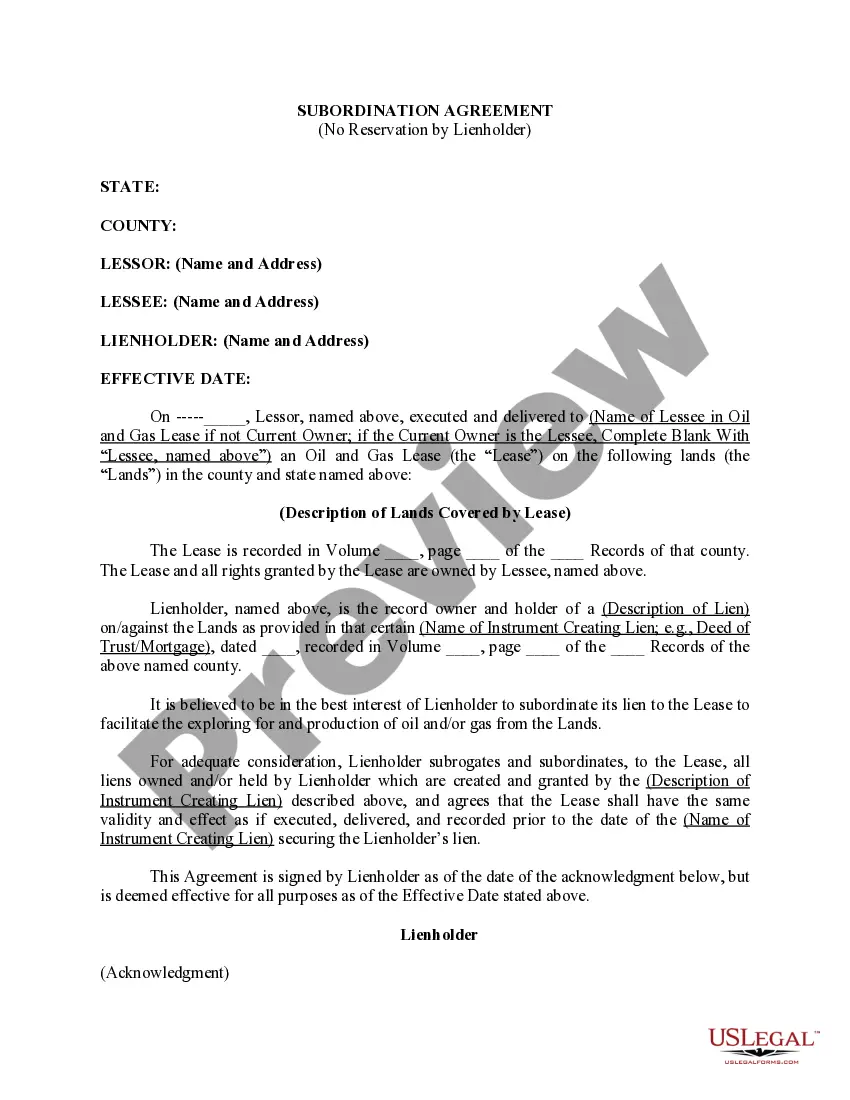

A Missouri Subordination Agreement with no Reservation by Lien holder is a legal document that outlines the relationship between two parties — liesoldererean borrowedewerewe— - in regards to the priority of their claims on a property. In this agreement, the lien holder agrees to subordinate or place their claim or lien on the property in a lower priority position compared to another lien or mortgage. The purpose of this agreement is to facilitate the refinancing or financing of a property with a new loan or mortgage, without hindrance from the existing lien holder. Keywords: Missouri, subordination agreement, reservation, lien holder, priority, property, borrower, claim, refinancing, financing There are several types of Missouri Subordination Agreement with no Reservation by Lien holder, including: 1. First Mortgage Subordination Agreement: This type of agreement occurs when the lien holder, who holds the first mortgage lien on a property, agrees to subordinate their claim to a new loan or mortgage. The new loan or mortgage takes priority over the existing lien. 2. Second Mortgage Subordination Agreement: In this scenario, the lien holder with a second mortgage on a property agrees to subordinate their claim to a new loan or mortgage. This agreement allows the new loan to take priority over the existing second mortgage. 3. Home Equity Line of Credit (HELOT) Subordination Agreement: This agreement involves a lien holder who holds a home equity line of credit on a property. They agree to subordinate their claim to a new loan or mortgage, allowing the new financing to take priority over the existing HELOT. 4. Subordinated Lien Agreement: This type of agreement refers to a lien holder who holds a subordinate lien on a property. They agree to subordinate their claim to a new loan or mortgage, allowing the new financing to take precedence over their existing subordinate lien. In all of these cases, the Missouri Subordination Agreement with no Reservation by Lien holder is a vital legal tool used to coordinate the rights and priorities of different lien holders or mortgage holders on a property. It ensures smooth financing transactions and protects the interests of all parties involved.

Missouri Subordination Agreement with no Reservation by Lienholder

Description

How to fill out Missouri Subordination Agreement With No Reservation By Lienholder?

US Legal Forms - among the greatest libraries of authorized forms in America - offers a variety of authorized record templates it is possible to obtain or printing. Utilizing the site, you can find thousands of forms for organization and personal purposes, sorted by classes, says, or search phrases.You will discover the latest versions of forms like the Missouri Subordination Agreement with no Reservation by Lienholder within minutes.

If you already have a membership, log in and obtain Missouri Subordination Agreement with no Reservation by Lienholder from the US Legal Forms local library. The Download key will appear on each and every type you view. You have access to all previously downloaded forms within the My Forms tab of your account.

If you wish to use US Legal Forms for the first time, listed below are straightforward recommendations to obtain started:

- Be sure you have selected the proper type for your personal city/county. Click the Preview key to examine the form`s content material. Look at the type description to ensure that you have selected the appropriate type.

- In case the type doesn`t fit your needs, take advantage of the Search discipline at the top of the monitor to discover the one that does.

- When you are happy with the shape, affirm your decision by clicking the Purchase now key. Then, opt for the pricing plan you prefer and give your accreditations to register for an account.

- Method the transaction. Utilize your charge card or PayPal account to perform the transaction.

- Select the structure and obtain the shape on the device.

- Make changes. Fill out, change and printing and indicator the downloaded Missouri Subordination Agreement with no Reservation by Lienholder.

Each and every design you included with your account lacks an expiration day and is also the one you have forever. So, if you want to obtain or printing another backup, just proceed to the My Forms area and click around the type you want.

Obtain access to the Missouri Subordination Agreement with no Reservation by Lienholder with US Legal Forms, probably the most substantial local library of authorized record templates. Use thousands of skilled and state-particular templates that meet up with your small business or personal needs and needs.