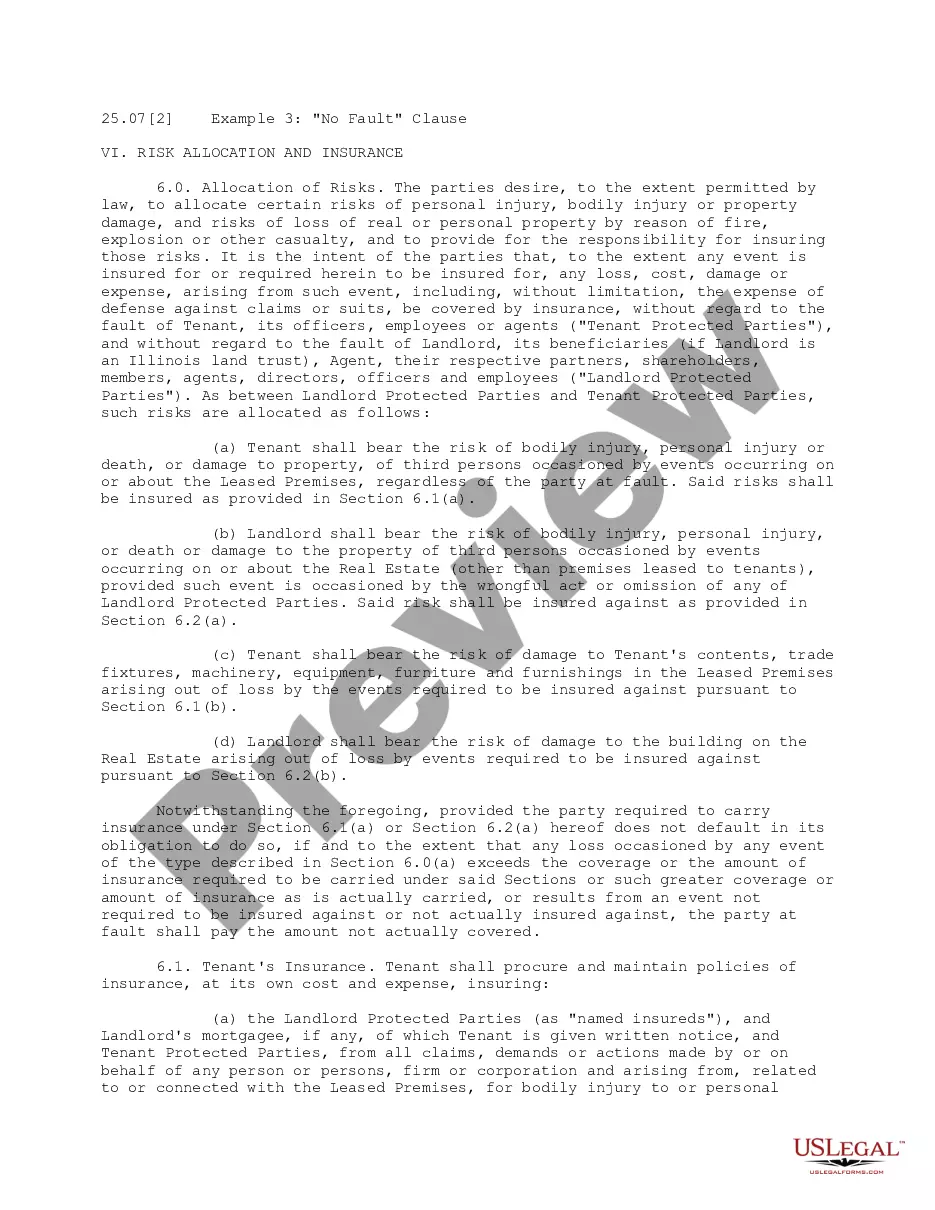

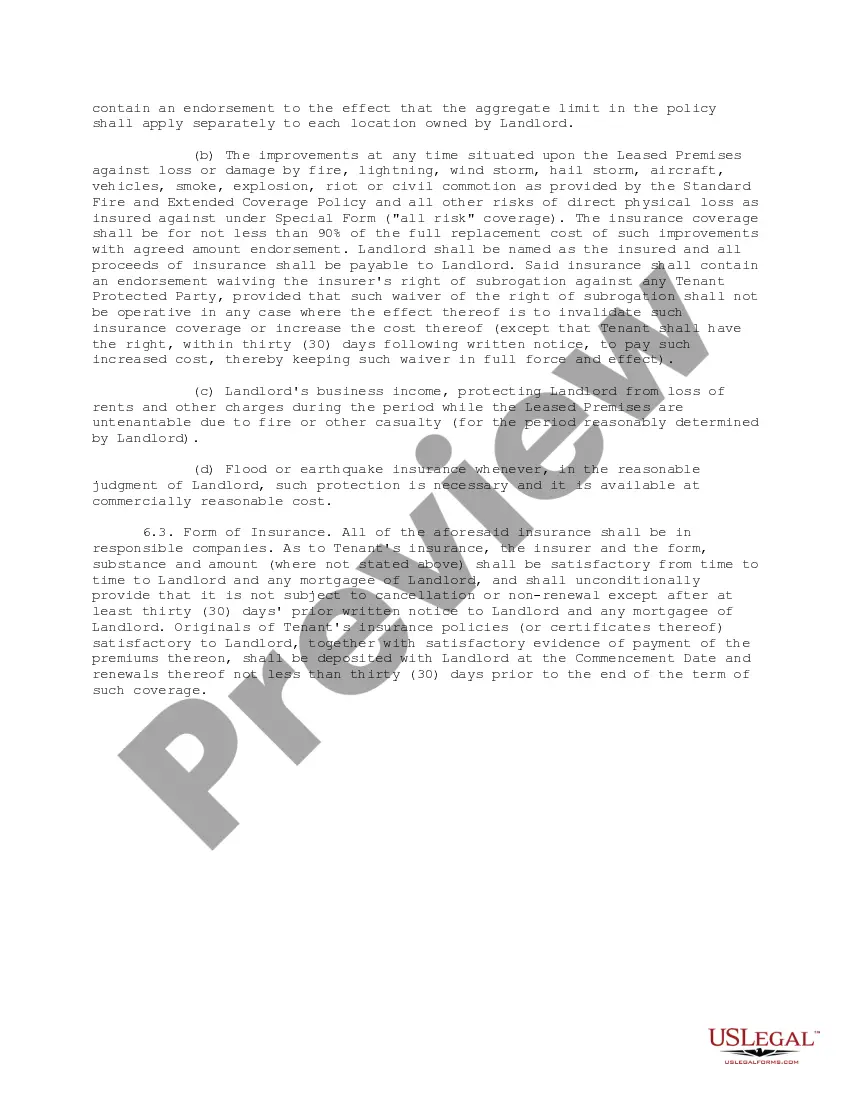

This office lease clause describes the allocation of risks. The parties desire to allocate certain risks of personal injury, bodily injury or property damage, and risks of loss of real or personal property by reason of fire, explosion or other casualty, and to provide for the responsibility for insuring those risks as permitted by law.

Missouri No Fault Clause, also known as the "Missouri Compulsory Insurance Law," refers to an essential provision in the state's auto insurance laws. This clause requires every vehicle owner to carry a minimum amount of insurance coverage in order to lawfully operate a motor vehicle in Missouri. The purpose of the Missouri No-Fault Clause is to ensure that individuals injured in automobile accidents receive prompt medical treatment and other necessary benefits, regardless of who is at fault. Under the Missouri No-Fault Clause, drivers must carry a minimum of $25,000 in bodily injury liability coverage per person, $50,000 in total bodily injury liability coverage per accident, and $10,000 in property damage liability coverage. This coverage is mandatory for all non-commercial motor vehicles and must be continuously maintained throughout the vehicle registration period. It is important to note that Missouri follows a "pure" comparative fault system. This means that when an accident occurs, fault can be assigned to multiple parties involved, and each party is responsible for their portion of liability. The Missouri No-Fault Clause does not eliminate the possibility of fault determination; rather, it ensures that immediate medical expenses and benefits are provided to injured parties, regardless of who caused the accident. While the Missouri No-Fault Clause primarily focuses on minimum liability insurance requirements, it does not mandate personal injury protection (PIP) coverage. PIP coverage provides medical expenses, rehabilitation costs, and other benefits to injured drivers and passengers, regardless of who caused the accident. However, PIP coverage is not required under the Missouri No-Fault Clause but can be purchased as an optional coverage. It is important to understand that the Missouri No-Fault Clause applies primarily to bodily injury and property damage liability coverage. Additional optional coverages, such as collision, comprehensive, uninsured/under insured motorist, and medical payments' coverage, can provide further financial protection in case of an accident. In summary, the Missouri No-Fault Clause is a crucial provision in Missouri's auto insurance laws. It requires all vehicle owners to carry minimum liability coverage, ensuring injured parties receive necessary benefits regardless of fault determination. While optional coverages exist to provide more extensive protection, the Missouri No-Fault Clause sets the foundation for maintaining a safer and more responsible driving environment in the state. Keywords: Missouri No Fault Clause, Missouri Compulsory Insurance Law, auto insurance laws, minimum liability coverage, bodily injury liability, property damage liability, fault determination, comparative fault system, personal injury protection (PIP), optional coverage, collision coverage, comprehensive coverage, uninsured/under insured motorist coverage, medical payments' coverage, Safer driving environment.Missouri No Fault Clause, also known as the "Missouri Compulsory Insurance Law," refers to an essential provision in the state's auto insurance laws. This clause requires every vehicle owner to carry a minimum amount of insurance coverage in order to lawfully operate a motor vehicle in Missouri. The purpose of the Missouri No-Fault Clause is to ensure that individuals injured in automobile accidents receive prompt medical treatment and other necessary benefits, regardless of who is at fault. Under the Missouri No-Fault Clause, drivers must carry a minimum of $25,000 in bodily injury liability coverage per person, $50,000 in total bodily injury liability coverage per accident, and $10,000 in property damage liability coverage. This coverage is mandatory for all non-commercial motor vehicles and must be continuously maintained throughout the vehicle registration period. It is important to note that Missouri follows a "pure" comparative fault system. This means that when an accident occurs, fault can be assigned to multiple parties involved, and each party is responsible for their portion of liability. The Missouri No-Fault Clause does not eliminate the possibility of fault determination; rather, it ensures that immediate medical expenses and benefits are provided to injured parties, regardless of who caused the accident. While the Missouri No-Fault Clause primarily focuses on minimum liability insurance requirements, it does not mandate personal injury protection (PIP) coverage. PIP coverage provides medical expenses, rehabilitation costs, and other benefits to injured drivers and passengers, regardless of who caused the accident. However, PIP coverage is not required under the Missouri No-Fault Clause but can be purchased as an optional coverage. It is important to understand that the Missouri No-Fault Clause applies primarily to bodily injury and property damage liability coverage. Additional optional coverages, such as collision, comprehensive, uninsured/under insured motorist, and medical payments' coverage, can provide further financial protection in case of an accident. In summary, the Missouri No-Fault Clause is a crucial provision in Missouri's auto insurance laws. It requires all vehicle owners to carry minimum liability coverage, ensuring injured parties receive necessary benefits regardless of fault determination. While optional coverages exist to provide more extensive protection, the Missouri No-Fault Clause sets the foundation for maintaining a safer and more responsible driving environment in the state. Keywords: Missouri No Fault Clause, Missouri Compulsory Insurance Law, auto insurance laws, minimum liability coverage, bodily injury liability, property damage liability, fault determination, comparative fault system, personal injury protection (PIP), optional coverage, collision coverage, comprehensive coverage, uninsured/under insured motorist coverage, medical payments' coverage, Safer driving environment.