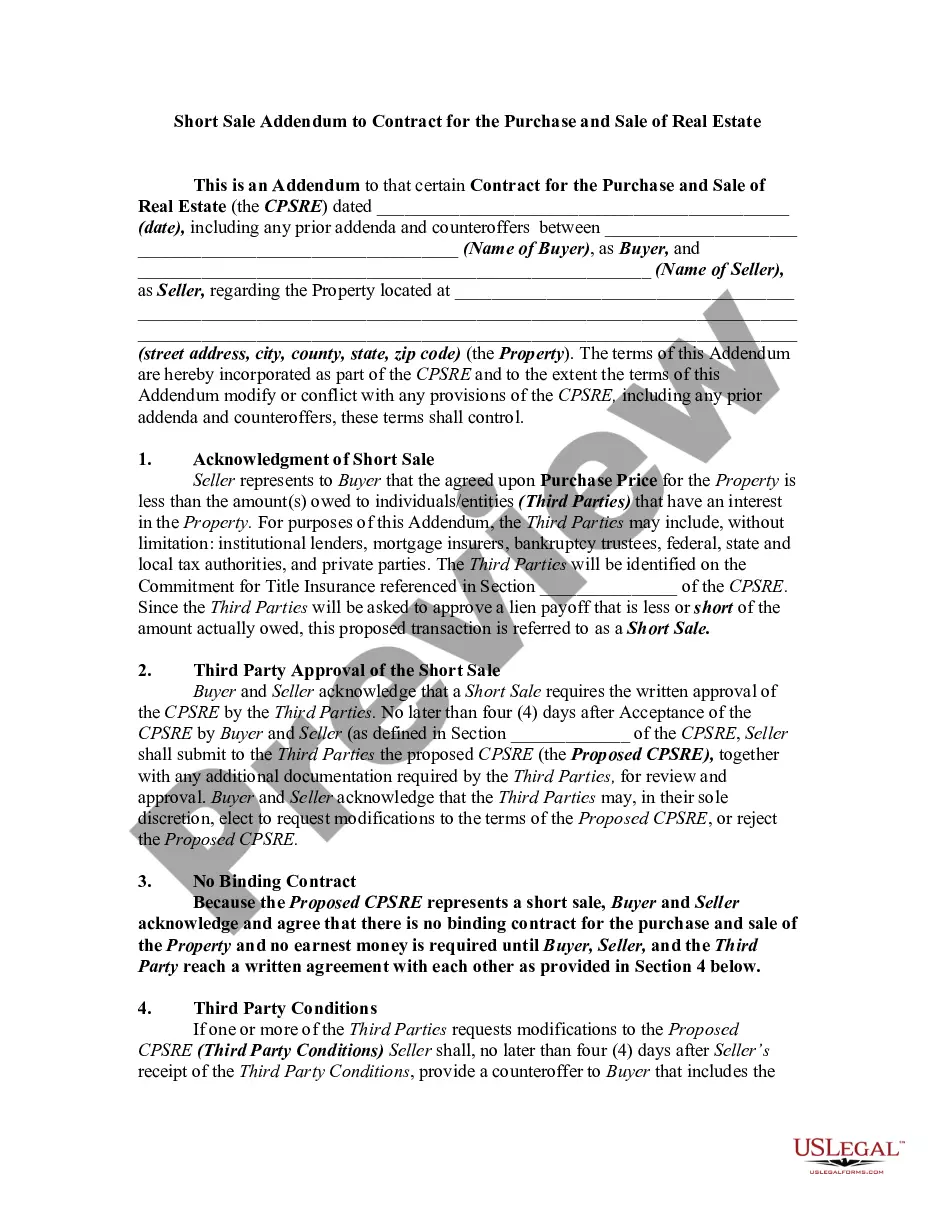

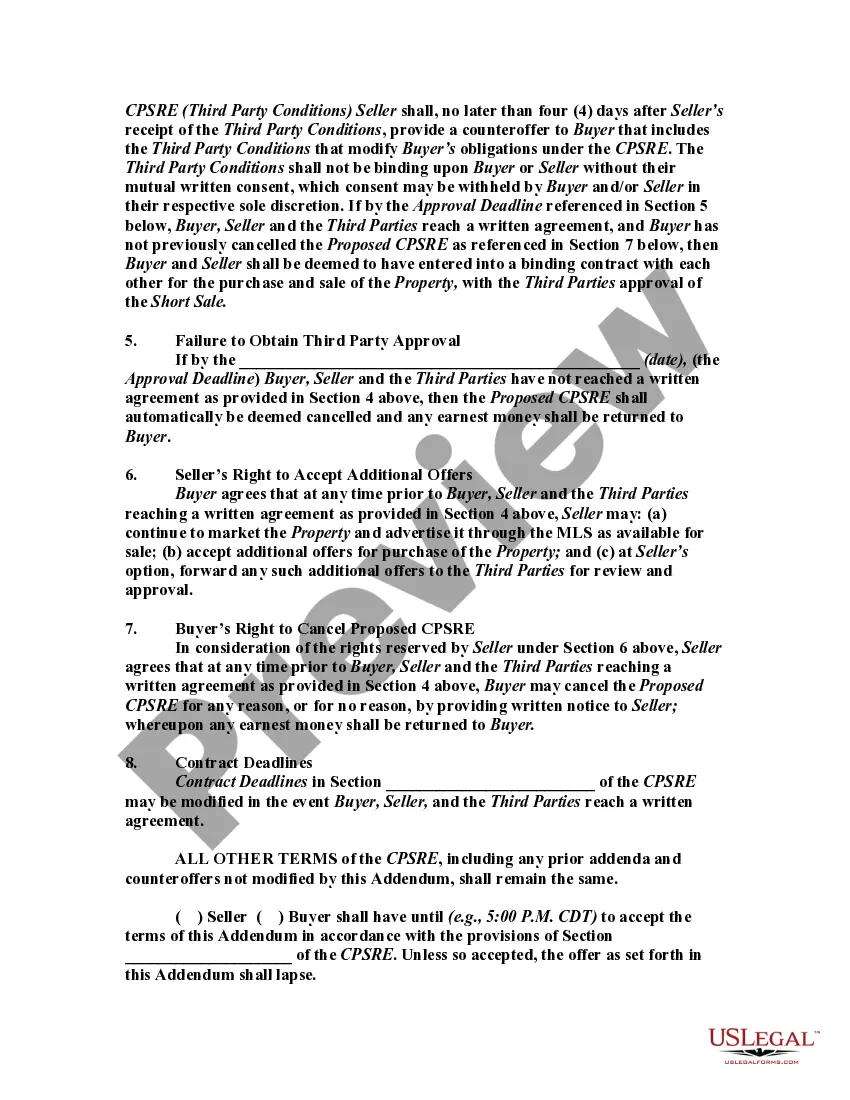

In real estate, a short sale occurs when a bank or mortgage lender agrees to discount a loan balance due to an economic hardship on the part of the mortgagor (i.e., the seller). Circumstances determine whether or not banks will discount a loan balance. These circumstances are usually related to the current real estate market climate and the individual borrower's financial situation. A short sale typically is executed to prevent a home foreclosure. Often a bank will choose to allow a short sale if they believe that it will result in a smaller financial loss than foreclosing.

This form is a sample of an Addendum to a standard real estate sales contract in order to incorporate the short sales provisions. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Mississippi Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate is a legal document that is used in real estate transactions involving short sales in the state of Mississippi. A short sale occurs when a homeowner sells their property for a price that is less than the amount owed on their mortgage. This addendum is required to be used in conjunction with the standard contract for the purchase and sale of real estate. The purpose of the Mississippi Short Sale Addendum is to outline the specific terms and conditions that apply to a short sale transaction. It provides protection for both the buyer and the seller, as it sets forth the rights and responsibilities of each party. Some key components covered in the Mississippi Short Sale Addendum include: 1. Purchase Price: This section details the agreed-upon purchase price for the property, which is generally less than the outstanding mortgage balance. 2. Mortgage Approval: The addendum stipulates that the transaction is contingent upon the seller obtaining approval from their mortgage lender to proceed with the short sale. 3. Timeframes: The document specifies the timeframe in which the lender must respond to the short sale request and whether the buyer has the right to terminate the contract if the response is not received within the given timeframe. 4. Seller Contributions: The addendum addresses whether the seller is required to contribute any funds towards the closing costs or unpaid mortgage balance. 5. Property Condition: This section outlines the buyer's rights to inspect the property and specifies that it is sold "as-is" with no warranties, unless otherwise agreed upon. 6. Non-Assignable: The addendum typically includes a provision stating that the contract is non-assignable without the written consent of all parties involved. 7. Contingencies: The document may include any additional contingencies that are specific to the short sale transaction, such as the release of any liens or judgments against the property. There may be different types or versions of the Mississippi Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate depending on the specific requirements of the parties involved or any amendments made by the Mississippi Real Estate Commission or other governing bodies. It is essential for both buyers and sellers to consult with a qualified real estate attorney or agent to ensure they are utilizing the most current and relevant version of the addendum.