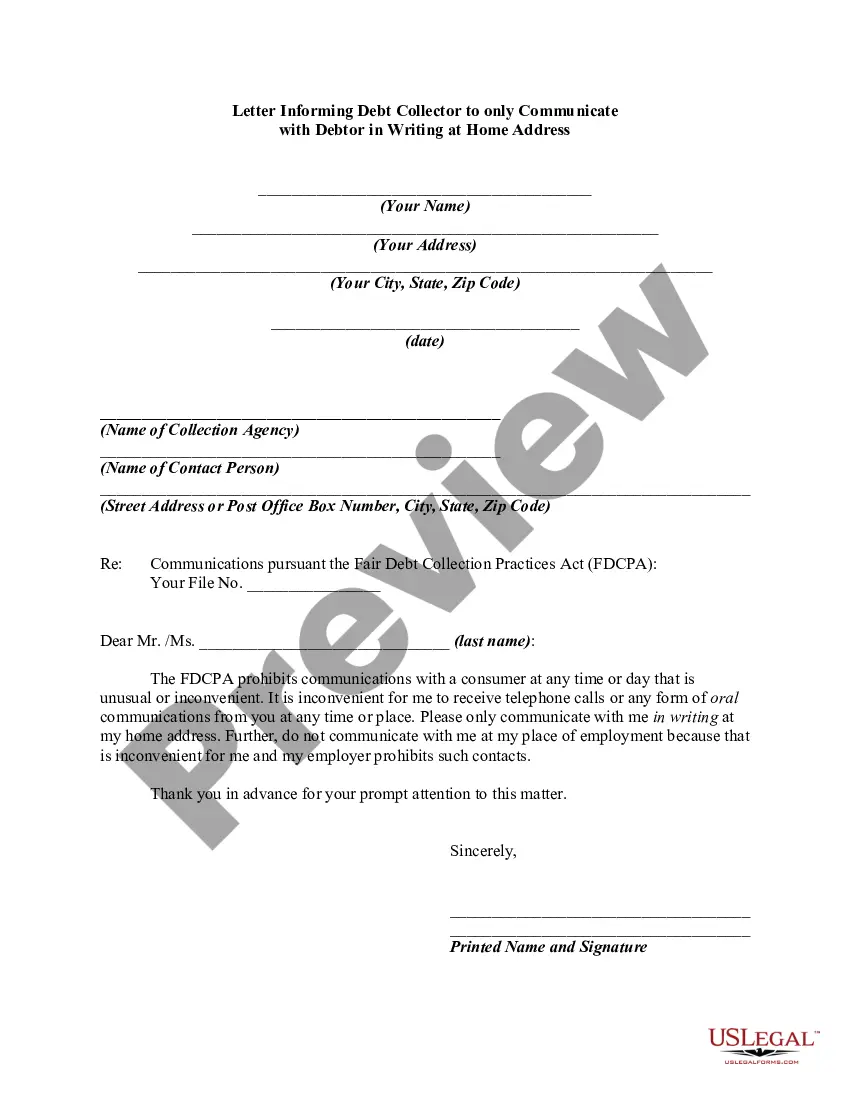

The Fair Debt Collection Practices Act (FDCPA) prohibits harassment or abuse in collecting a debt such as threatening violence, use of obscene or profane language, publishing lists of debtors who refuse to pay debts, or even harassing a debtor by repeatedly calling the debtor on the phone. This Act sets forth strict rules regarding communicating with the debtor.

The collector is restricted in the type of contact he can make with the debtor. He can't contact the debtor before 8:00 a.m. or after 9:00 p.m. He can contact the debtor at home, but cannot contact the debtor at the debtor's club or church or at a school meeting of some sort. The debtor cannot be contacted at work if his employer objects. If the debtor tells the creditor the name of his attorney, any future contacts must be made with the attorney and not with the debtor.

Title: Mississippi Letter Informing Debt Collector to Only Communicate with Debtor in Writing at Debtor's Home Address Introduction: In Mississippi, debtors have the right to control how and where debt collectors communicate with them. This letter serves as a written notice to inform debt collectors that the debtor wishes all communication to be in writing and delivered exclusively to their home address. This comprehensive guide explores the various types of letters debtors can use to assert their rights and specifies the relevant keywords to include for effective communication. Types of Mississippi Letters Informing Debt Collector to Only Communicate in Writing at Debtor's Home Address: 1. Standard Letter: Use this type when sending a general notice to debt collectors, requiring all communication to be in writing and delivered exclusively to the debtor's home address. State the debtor's full name, address, and contact information at the beginning of the letter for identification purposes. 2. Cease and Desist Letter: When debt collectors are engaging in aggressive or persistent contact, a cease and desist letter can be utilized. This type of letter states the debtor's request to stop all communication entirely, except in writing at their home address. Assert the debtor's legal rights and cite the Fair Debt Collection Practices Act (FD CPA) to build a strong case for compliance. 3. Verification Request Letter: Sometimes, debt collectors send letters demanding payment without providing adequate documentation to validate the debt. Use this type of letter to request the debt collector to prove the existence and validity of the debt. At the same time, specify that they should only communicate regarding this matter via written correspondence delivered to the debtor's home address. Keywords to Include in the Letter: 1. Mississippi's debt collection laws 2. Fair Debt Collection Practices Act (FD CPA) 3. Home address communication request 4. Written communication only 5. Cease and desist 6. Compliance 7. Validating debt 8. Debt collector's responsibilities 9. Legal rights 10. Verification of debt Conclusion: When dealing with debt collectors, Mississippi debtors hold specific rights to control communication methods. Drafting a well-structured letter is crucial in asserting these rights, specifying that all communication should only occur in writing at the debtor's home address. By utilizing appropriate keywords and selecting the appropriate type of letter, debtors can effectively communicate their preferences and ensure compliance with their requests. Remember to consult legal professionals or consumer protection agencies for further guidance to strengthen your case and protect your rights.