The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

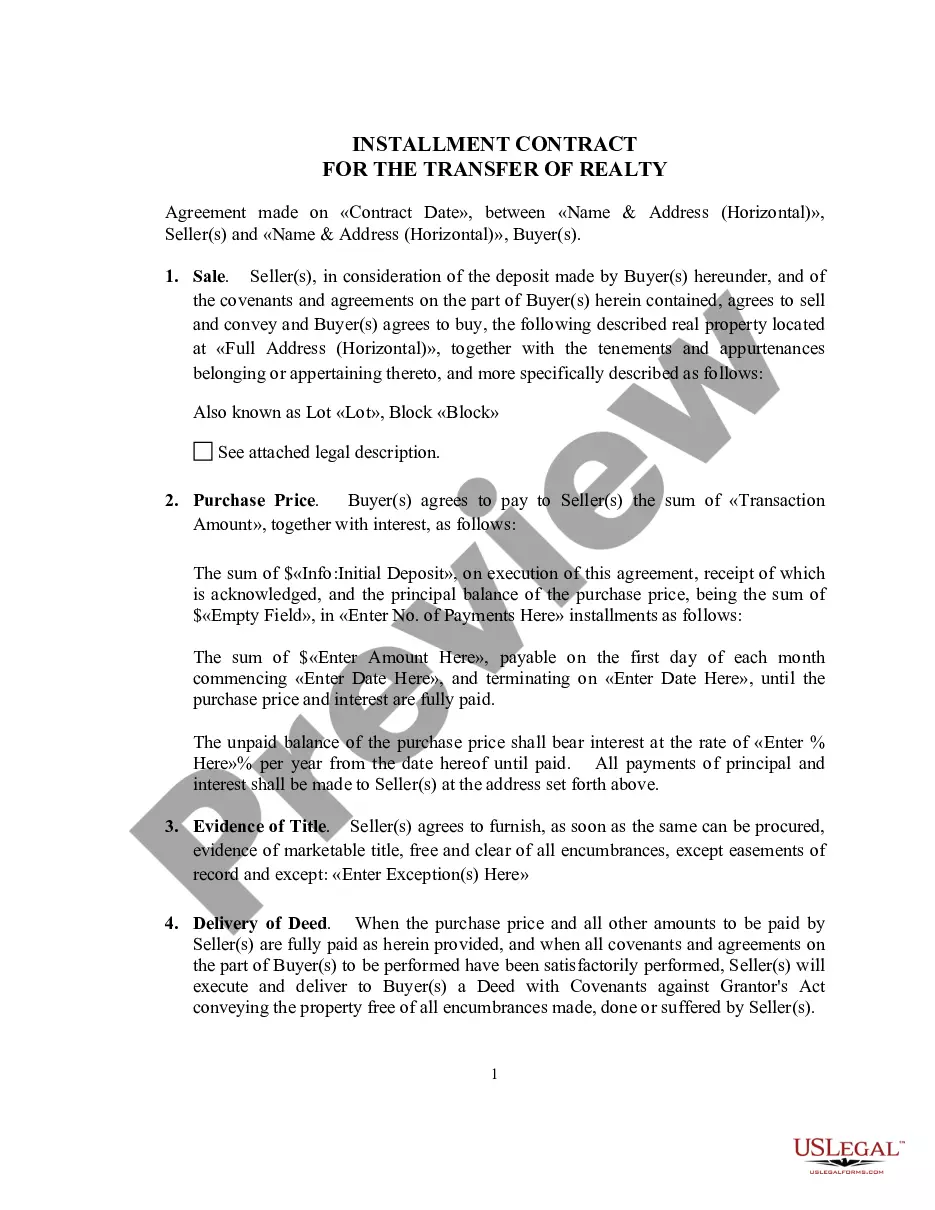

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Category:

State:

Multi-State

Control #:

US-02514BG

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures?

US Legal Forms - one of the topmost repositories of legal documents in the United States - offers a range of legal document templates that you can download or print.

By utilizing the website, you can discover thousands of forms for business and personal purposes, categorized by types, states, or keywords. You can quickly find the most recent templates such as the Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

If you have a monthly subscription, sign in and retrieve Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures from the US Legal Forms collection. The Download button will appear on each form you view. You can access all previously downloaded forms from the My documents tab of your account.

- Make sure you have selected the correct form for your city/county.

- Check the Review option to evaluate the form's content.

- Examine the form description to ensure you have selected the right document.

- If the document does not meet your requirements, use the Search field at the top of the screen to find the appropriate one.

- If you are satisfied with the form, confirm your choice by clicking the Purchase now button.

- Then, select the pricing plan you desire and provide your credentials to register for an account.

Form popularity

FAQ

In the Truth in Lending Disclosure, lenders must disclose items such as the total amount financed, finance charges, annual percentage rate, and total payment schedule. These disclosures are vital for allowing consumers to understand their borrowing costs clearly. The Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures ensures that borrowers receive accurate information for sound financial planning.

Contract disclosures must be provided to consumers before they sign any finance agreement. This ensures individuals have adequate time to review and understand the terms being presented. Utilizing the Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures allows consumers to make educated choices regarding their financial obligations.

Loans that are not covered by the Truth in Lending Act include student loans, loans secured by real estate, and certain business loans. Additionally, public utility loans and loans over certain thresholds may also be exempt. Familiarizing oneself with the Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures clarifies which loans require compliance and which do not.

Loans that do not require TILA disclosures typically include those outside the scope of consumer credit. For example, loans made for tax-exempt bonds or loans secured by a mortgage on a consumer's principal dwelling under specific conditions might be exempt. Understanding the nuances of the Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures is crucial for both lenders and borrowers.

Certain loans are exempt from the Truth in Lending Act requirements. These include loans made primarily for business, commercial, or agricultural purposes, as well as loans to high-net-worth individuals. Being aware of the Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures assists borrowers in navigating which loans require detailed disclosures.

The Truth in Lending Act applies to a wide range of credit transactions, including those related to the Mississippi General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures. It encompasses loans secured by property, credit cards, and retail installment contracts. The primary goal is to promote transparency and enable consumers to make informed financial decisions. Compliance with this Act is vital for both lenders and borrowers.

The Truth in Lending Act obligates retail businesses to provide detailed information about their credit terms clearly. This encompasses not only the total amount financed but also any additional fees and the annual percentage rate. Compliance with these disclosures aids consumers in making informed choices regarding their purchases. Companies can utilize uslegalforms to ensure they meet all necessary requirements and remain compliant.