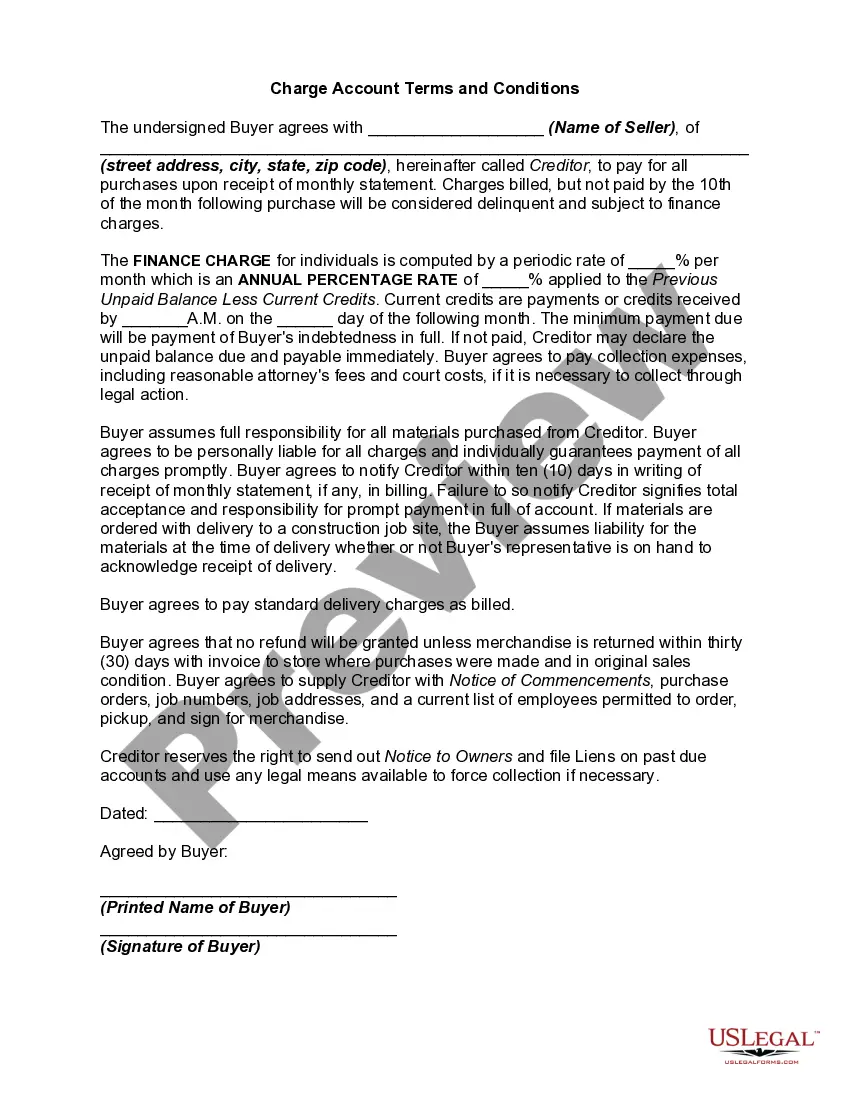

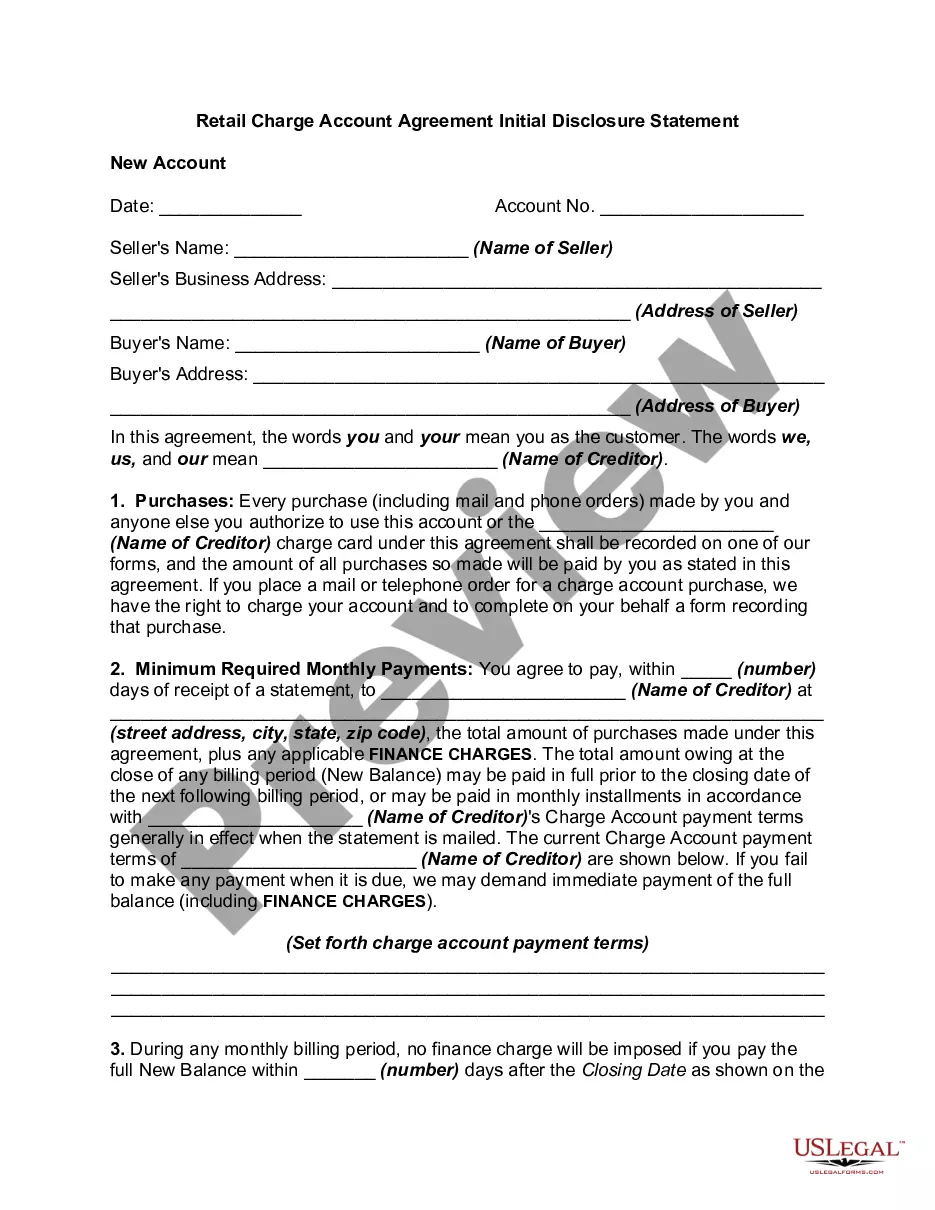

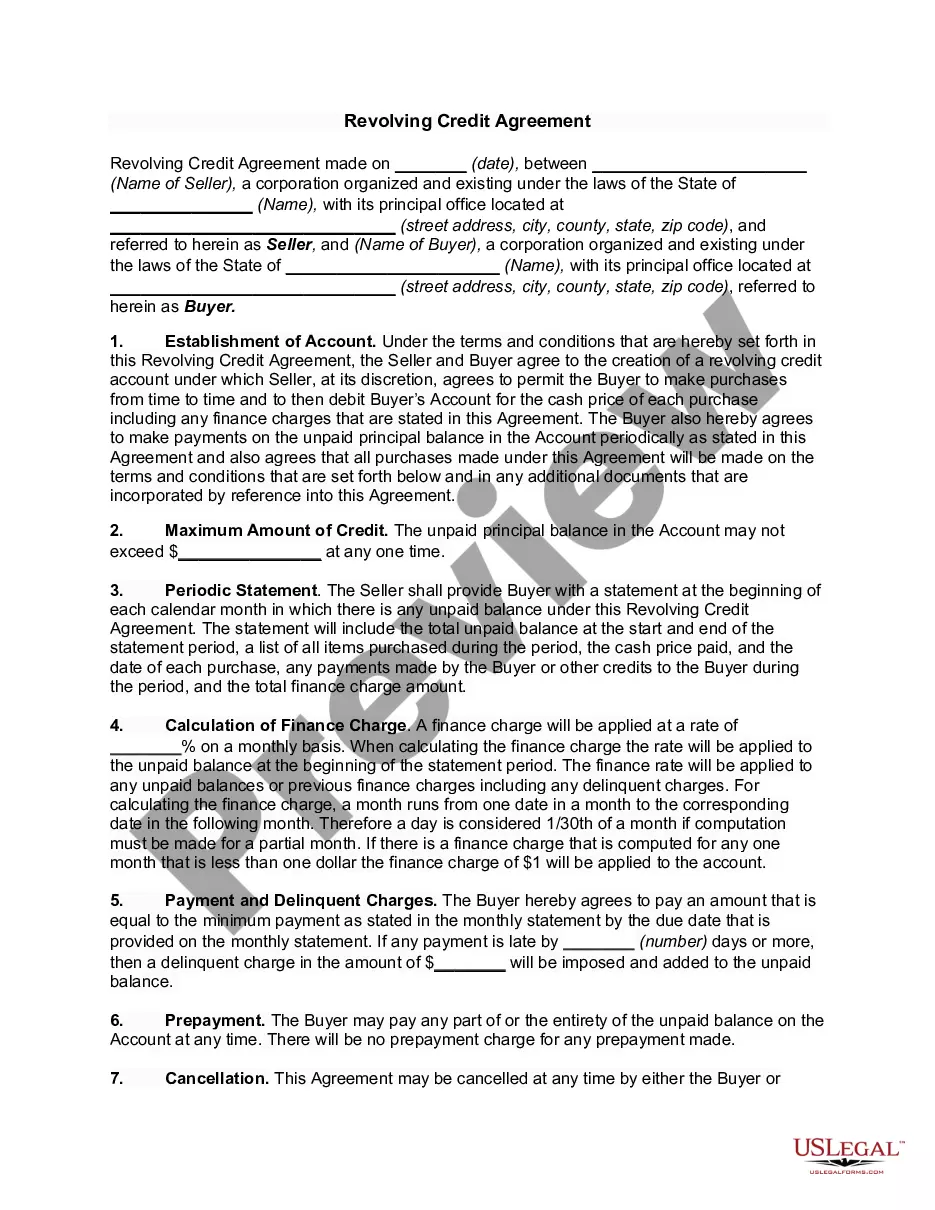

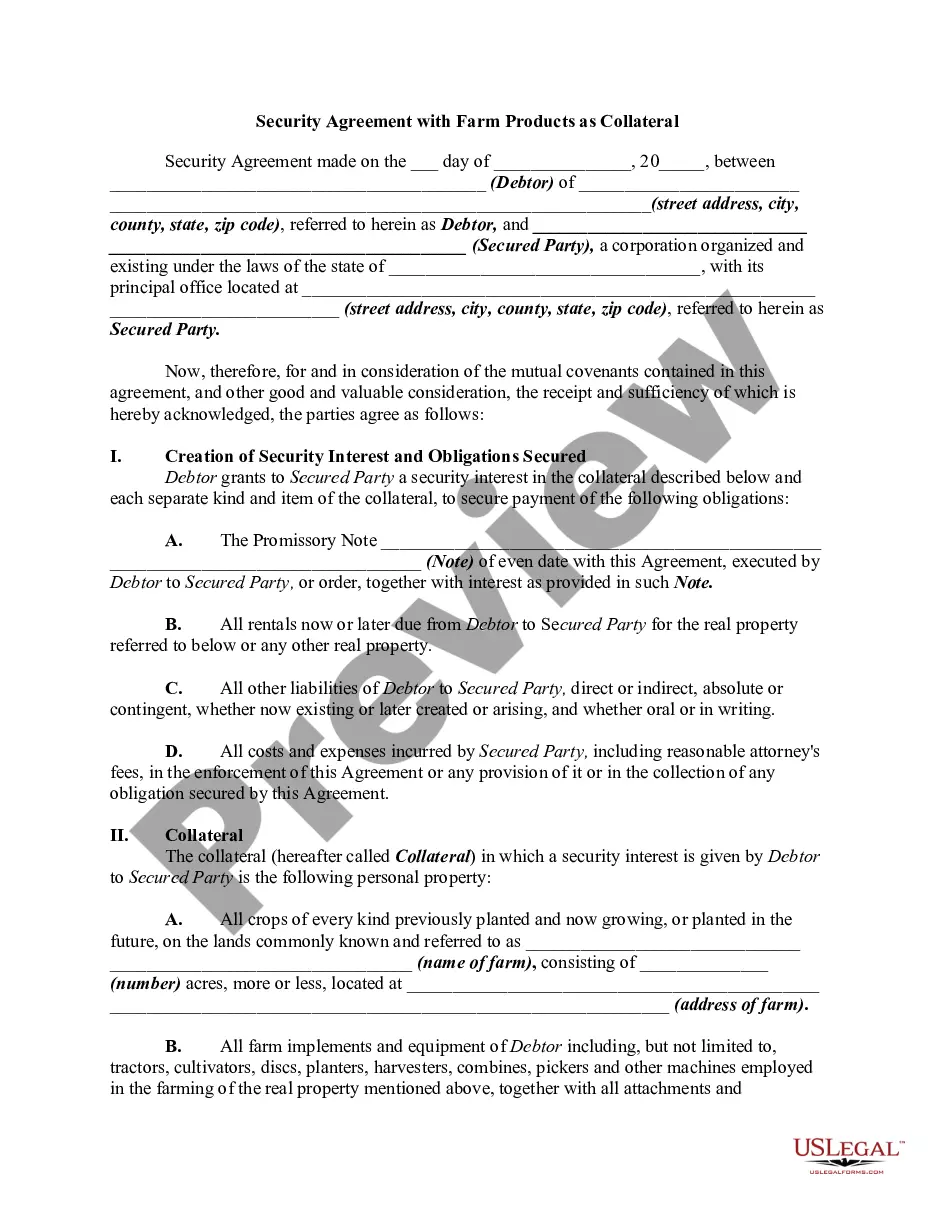

Mississippi Credit Card Agreement and Disclosure Statement

Description

How to fill out Credit Card Agreement And Disclosure Statement?

Are you within a place where you need to have documents for both company or personal purposes nearly every day? There are plenty of lawful document themes accessible on the Internet, but locating versions you can rely isn`t straightforward. US Legal Forms gives a large number of kind themes, like the Mississippi Credit Card Agreement and Disclosure Statement, that happen to be created to satisfy federal and state requirements.

Should you be currently informed about US Legal Forms internet site and possess a free account, just log in. After that, you can acquire the Mississippi Credit Card Agreement and Disclosure Statement format.

Should you not have an accounts and would like to begin using US Legal Forms, abide by these steps:

- Get the kind you want and ensure it is for that proper town/county.

- Use the Preview option to analyze the form.

- Look at the outline to actually have selected the correct kind.

- When the kind isn`t what you`re trying to find, make use of the Look for field to obtain the kind that fits your needs and requirements.

- Once you find the proper kind, simply click Get now.

- Opt for the prices strategy you would like, complete the desired details to generate your money, and pay money for an order making use of your PayPal or credit card.

- Select a convenient paper file format and acquire your version.

Find each of the document themes you have purchased in the My Forms food selection. You can obtain a further version of Mississippi Credit Card Agreement and Disclosure Statement anytime, if possible. Just go through the needed kind to acquire or printing the document format.

Use US Legal Forms, probably the most substantial selection of lawful kinds, to conserve efforts and stay away from blunders. The services gives professionally made lawful document themes that can be used for a range of purposes. Create a free account on US Legal Forms and commence producing your life a little easier.

Form popularity

FAQ

It is common for credit card companies to retain account information for up to seven years, although this is not necessarily the case. Depending on your card's issuer, you might be able to request statement copies over the phone, by visiting a branch or by mail.

Your credit card company must mail or deliver your credit card bill at least 21 days before your payment is due. In addition Your due date should be the same date each month (for example, your payment is always due on the 15th or always due on the last day of the month).

A credit card company doesn't have to send you a monthly statement if: The account is considered uncollectible ? There may be a number of circumstances where your account is uncollectable, including death, bankruptcy, failure to update your contact information, or the statute of limitations has expired for your debt.

The Cardholder Agreement details the terms and conditions of your credit card account and includes information such as the rate, fees, and other cost information associated with the account.

Definition. A credit card disclosure is a document that outlines all of the fees, costs, interest rates, and terms that a customer could experience while using the credit card. Institutions that offer credit cards are required by law to disclose this information.

Credit card companies and banks typically mail out your monthly statement after the end of your billing cycle. If you've signed up for paperless billing, you'll receive an email notification that your monthly statement is available.

You should be able to find pricing and terms information adjacent to any credit card application. If you can't locate this information, contact the issuer directly and request it. They are required by law to give it to you.

Credit card issuers must adopt reasonable procedures designed to ensure that they mail or electronically deliver statements at least 21 days before the payment due date. Review your account agreement for policies specific to your bank and your account.