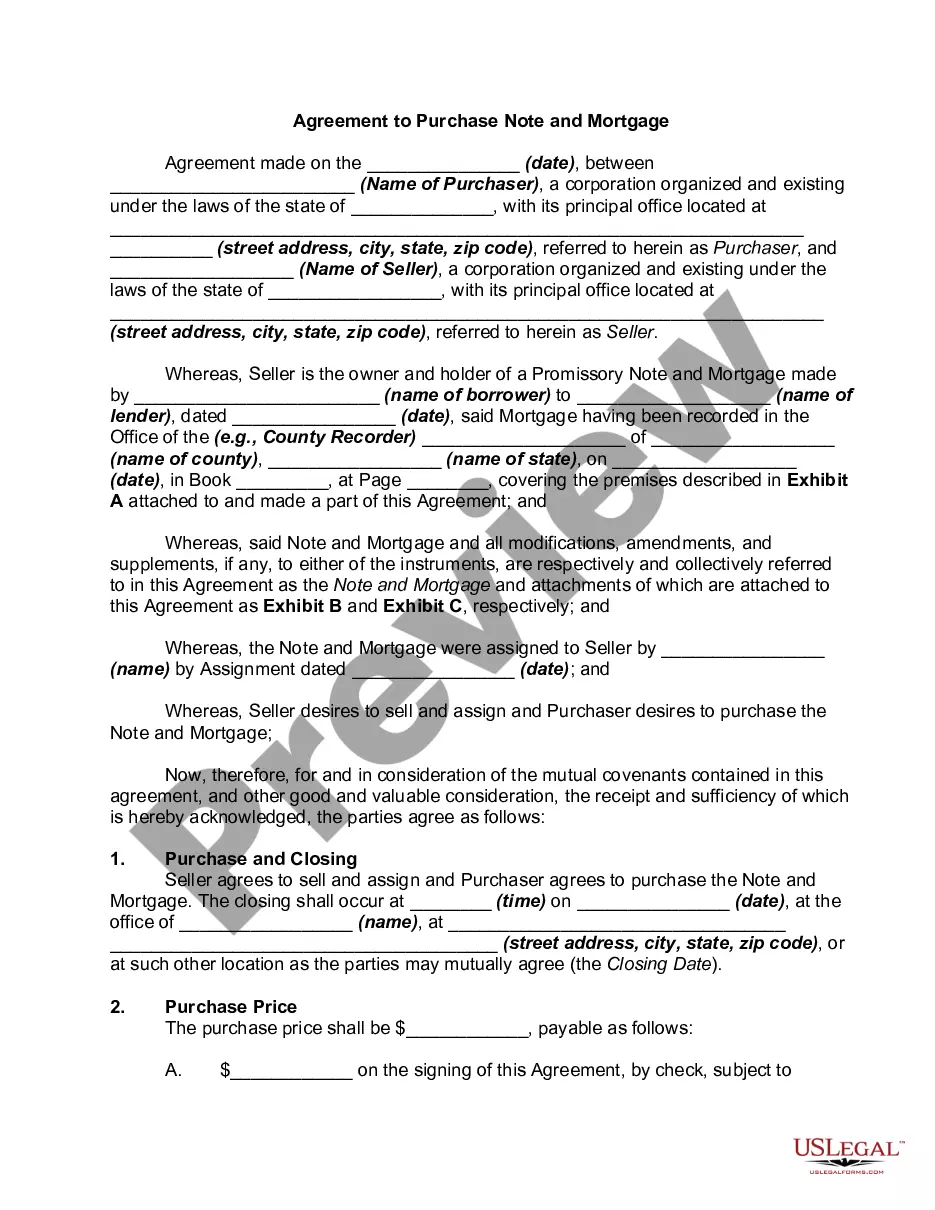

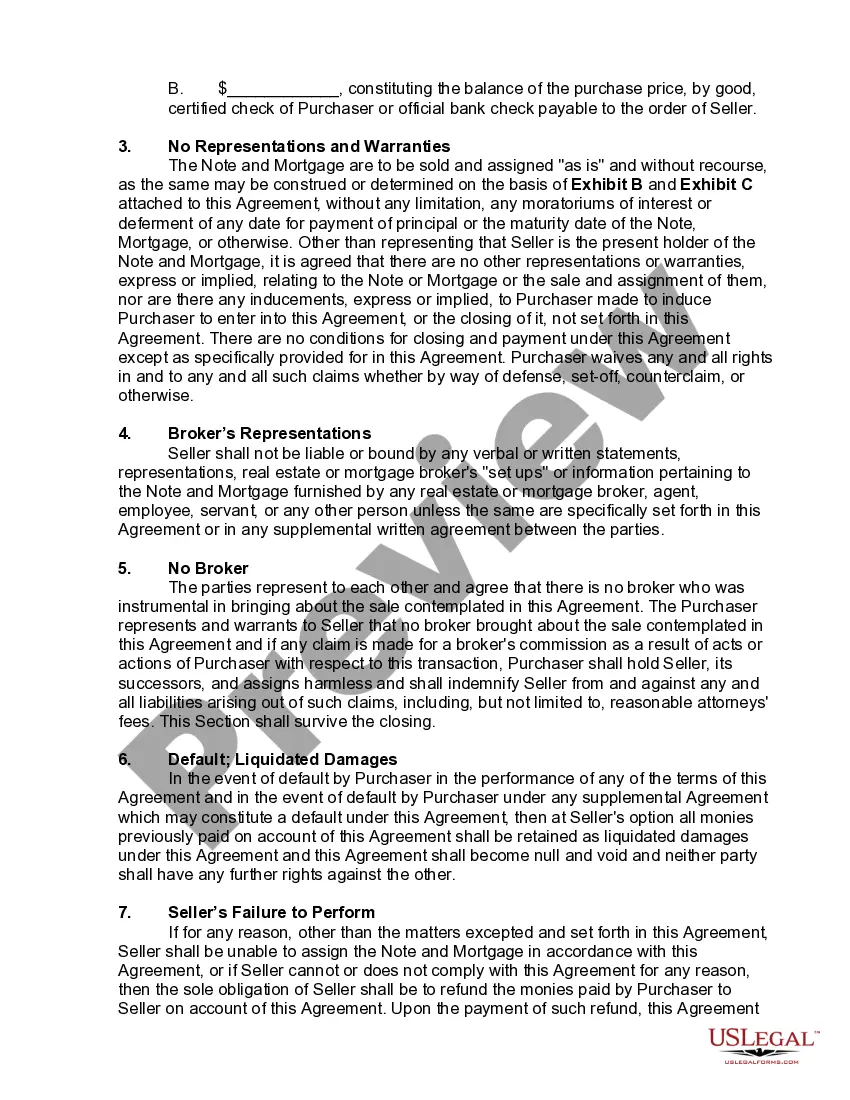

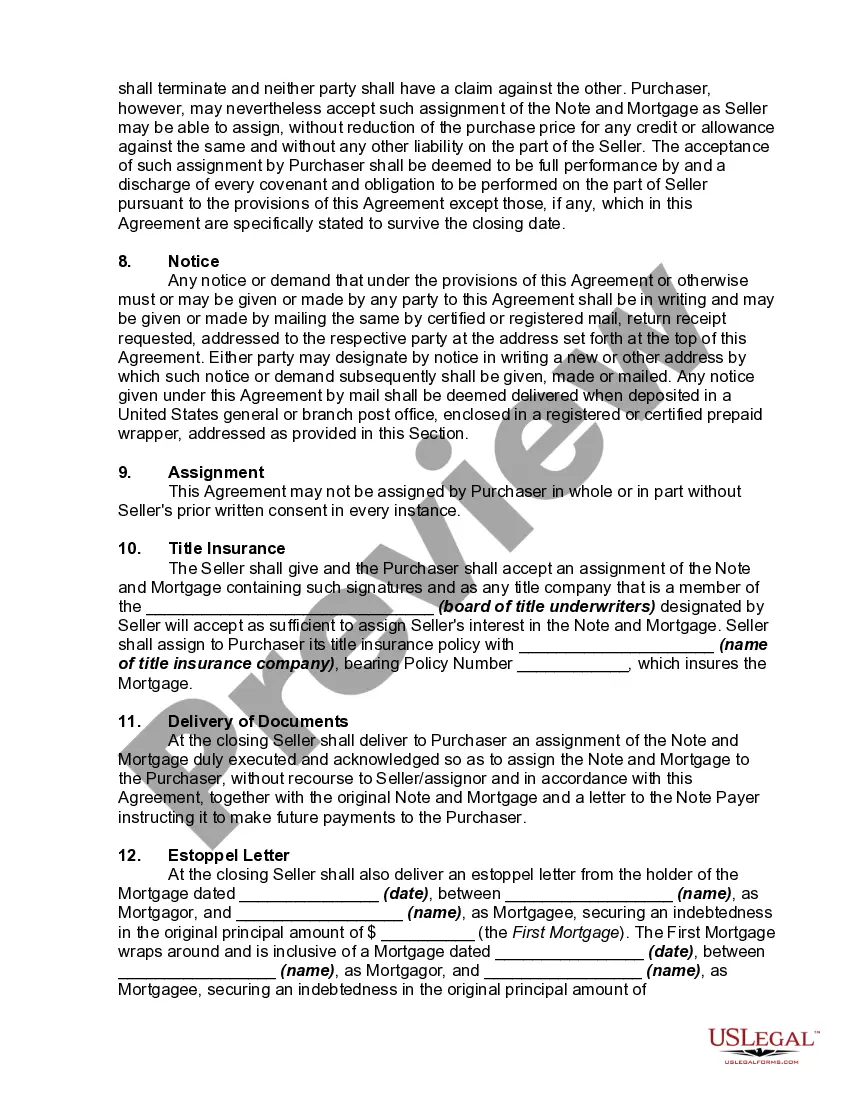

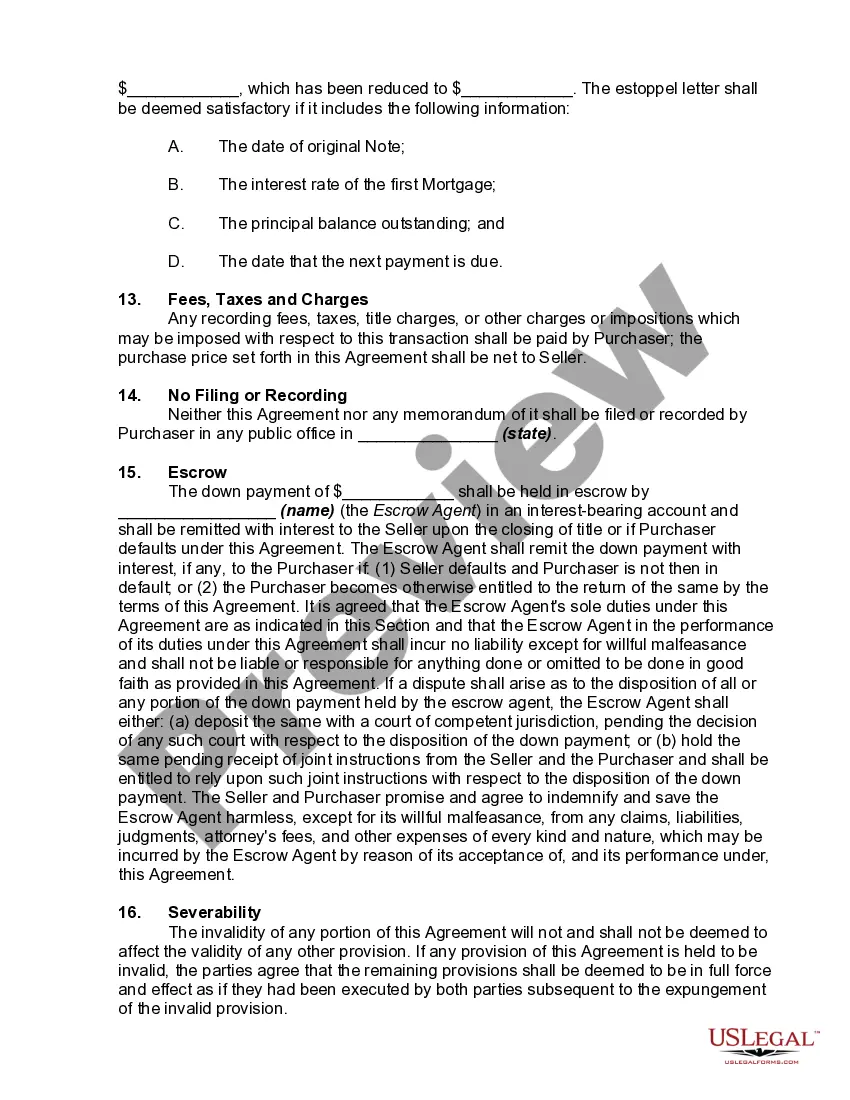

The Mississippi Agreement to Purchase Note and Mortgage is a legal document that outlines the terms and conditions of a real estate transaction in which a buyer agrees to purchase a property through a combination of a promissory note and a mortgage. It is a binding agreement between the buyer (also known as the mortgagor) and the seller (also known as the mortgagee). The Agreement to Purchase Note and Mortgage is an essential document in real estate transactions as it sets forth the obligations and rights of both parties involved. It ensures that both parties are protected and provides a clear understanding of the terms and conditions of the sale. The promissory note is a detailed written promise by the buyer to repay the amount borrowed over a specific period of time and at a predetermined interest rate. It serves as evidence of the buyer's debt to the seller and the terms under which the debt should be repaid. The mortgage, on the other hand, is a legal instrument that serves as security for the repayment of the promissory note. It involves the transfer of an interest in the property from the buyer to the seller, which acts as collateral in case of default on the loan. This means that if the buyer fails to make the agreed-upon payments, the seller has the right to foreclose on the property and recover the outstanding debt. In Mississippi, there are various types of Agreement to Purchase Note and Mortgage, including: 1. Fixed-rate Mortgage: A type of mortgage where the interest rate remains constant throughout the loan term. 2. Adjustable-rate Mortgage (ARM): A mortgage in which the interest rate is subject to adjustment based on a specified index or market conditions. The interest rate may change periodically, affecting the monthly payments. 3. Balloon Mortgage: A mortgage that requires the borrower to make small monthly payments for a specified period, usually 5 or 7 years, followed by a large "balloon payment" to pay off the remaining principal. 4. Government-Backed Mortgages: Mississippi has various government-backed loan programs, such as FHA (Federal Housing Administration) and VA (Veterans Affairs) loans, which offer favorable terms and require less stringent qualifications. 5. Jumbo Mortgage: A mortgage that exceeds the loan limits set by the Federal Housing Finance Agency (FIFA). These mortgages are typically used for higher-value properties. It is crucial for both the buyer and seller to review the Agreement to Purchase Note and Mortgage carefully, understanding the terms, interest rates, repayment schedules, and any associated fees or penalties. Consulting with a real estate attorney or mortgage professional is highly recommended ensuring compliance with Mississippi state laws and regulations.

Mississippi Agreement to Purchase Note and Mortgage

Description

How to fill out Mississippi Agreement To Purchase Note And Mortgage?

If you want to full, down load, or print out authorized record layouts, use US Legal Forms, the greatest selection of authorized kinds, that can be found on the web. Use the site`s easy and practical lookup to obtain the documents you will need. Various layouts for enterprise and specific functions are sorted by categories and claims, or key phrases. Use US Legal Forms to obtain the Mississippi Agreement to Purchase Note and Mortgage within a few click throughs.

In case you are already a US Legal Forms consumer, log in for your accounts and click on the Obtain key to obtain the Mississippi Agreement to Purchase Note and Mortgage. You can also gain access to kinds you in the past downloaded in the My Forms tab of the accounts.

If you work with US Legal Forms for the first time, follow the instructions beneath:

- Step 1. Be sure you have selected the form for the proper city/country.

- Step 2. Take advantage of the Preview method to check out the form`s content material. Do not forget to read the outline.

- Step 3. In case you are unsatisfied using the develop, make use of the Research field towards the top of the display to find other versions in the authorized develop template.

- Step 4. After you have discovered the form you will need, go through the Buy now key. Choose the rates prepare you favor and put your references to sign up for an accounts.

- Step 5. Procedure the transaction. You may use your Мisa or Ьastercard or PayPal accounts to finish the transaction.

- Step 6. Choose the format in the authorized develop and down load it on your own device.

- Step 7. Total, modify and print out or sign the Mississippi Agreement to Purchase Note and Mortgage.

Each authorized record template you buy is your own property eternally. You possess acces to every single develop you downloaded within your acccount. Select the My Forms area and select a develop to print out or down load once more.

Remain competitive and down load, and print out the Mississippi Agreement to Purchase Note and Mortgage with US Legal Forms. There are thousands of professional and condition-specific kinds you may use for the enterprise or specific needs.

Form popularity

FAQ

An option to purchase is an agreement that gives a potential buyer (?optionee?) the right, but not the obligation, to buy property in the future.

A purchase and sale agreement, or PSA, is a document that is written up and signed after a buyer and seller mutually agree on the price and terms of a real estate transaction. Depending on state laws, either a real estate agent or a real estate attorney will prepare the PSA.

The Statute of Frauds dictates that a contract for the transfer of an interest in real estate must be in writing and must be signed by the party against whom the contract is being enforced.

The important difference is that an offer hasn't been agreed upon yet. A signed purchase agreement also usually contains the terms of the sale, spelling out what is required for the sale to be completed and that both parties have agreed to.

The purchase agreement usually is preceded in the process by a ?letter of intent? (referred to in this article as the ?LOI?). While certain terms in the LOI are legally binding, the LOI is not intended to bind the parties to do the sale itself. The LOI instead expresses the parties' intent to pursue the sale.

The Mississippi purchase agreement establishes the terms of a residential real estate transaction. A prospective buyer can use this form to submit an offer for the seller to accept or counter. The document must include the prospective purchase price, loan details, and amount of the earnest money payment.

How to write a real estate purchase agreement Identify the address of the property being purchased, including all required legal descriptions. Identify the names and addresses of both the buyer and the seller. Detail the price of the property and the terms of the purchase. Set the closing date and closing costs.

Mortgage. A mortgage is an agreement between you and a lender that allows you to borrow money to purchase or refinance a home and gives the lender the right to take your property if you fail to repay the money you've borrowed.