In real estate, a short sale occurs when a bank or mortgage lender agrees to discount a loan balance due to an economic hardship on the part of the mortgagor (i.e., the seller). Circumstances determine whether or not banks will discount a loan balance. These circumstances are usually related to the current real estate market climate and the individual borrower's financial situation. A short sale typically is executed to prevent a home foreclosure. Often a bank will choose to allow a short sale if they believe that it will result in a smaller financial loss than foreclosing.

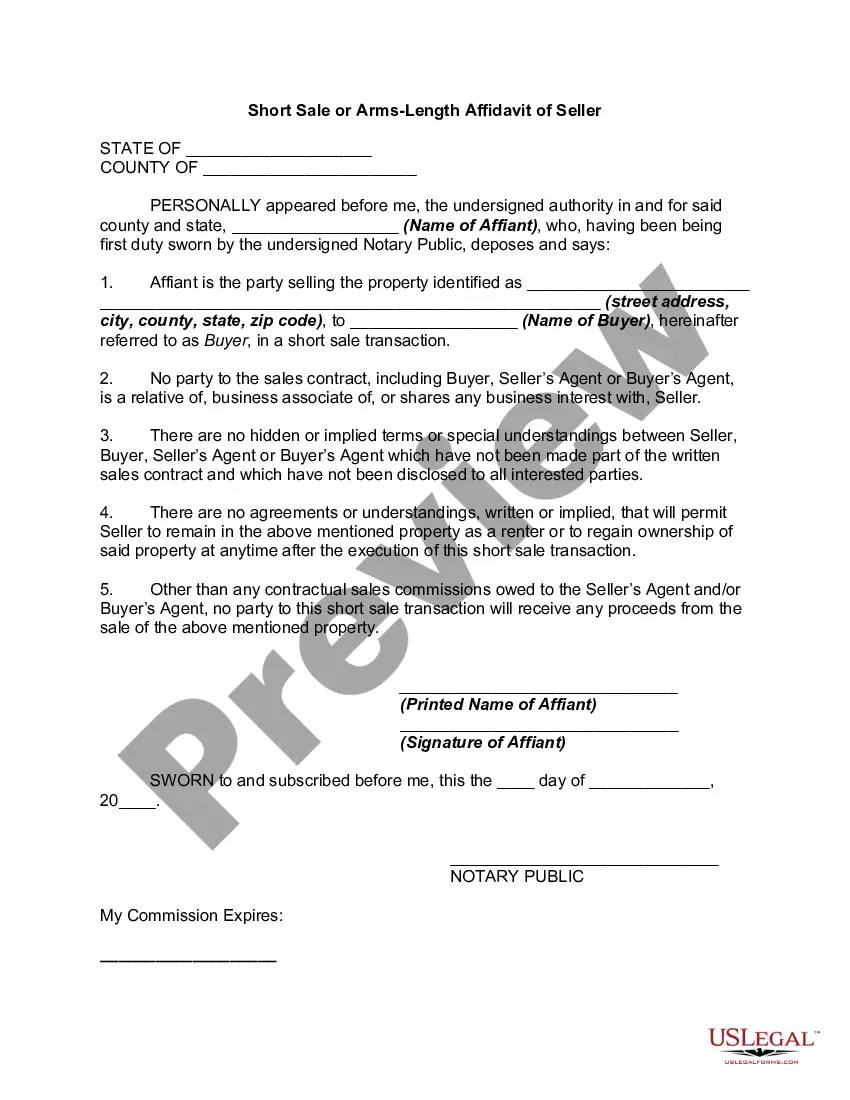

An arms-length or short sale affidavit is a document created by a bank in an attempt to prevent sellers from selling to relatives or friends to act as a straw buyer. Sometimes sellers make such side agreements. Then, after the transaction closes, the pretend buyers quickly transfer title back to the seller. This practice, in affect, means the sellers have repurchased their home at maybe half the cost, which greatly benefits those sellers.

A Mississippi Short Sale or Arms Length Affidavit is a legal document used in the state of Mississippi to ensure fair practices are followed during a property short sale transaction. This affidavit is typically required by lenders and serves as an acknowledgment from all parties involved, including the buyer, seller, and real estate agents, that the transaction is being conducted at arm's length. An arm's length transaction signifies that the buyer and seller have no existing relationship that could potentially influence the sale price or terms. It ensures that the market value is accurately represented, preventing any potential fraud or unethical practices in the transaction. This type of affidavit is crucial in maintaining transparency and preventing any conflicts of interest. The Mississippi Short Sale or Arms Length Affidavit may vary slightly in content from one lender or transaction to another. However, the main purpose of this document remains the same. It requires the parties involved to disclose any known relationships, financial interests, or affiliations that could influence the transaction. Some of the keywords that are relevant to this topic include "Mississippi short sale," "affidavit," "arms-length transaction," "property sale," "real estate transaction," "buyer," "seller," "lender," and "conflict of interest." It is important to note that the specific details and requirements of the Mississippi Short Sale or Arms Length Affidavit may vary, and it is advisable to consult with a real estate attorney or the lender for accurate and up-to-date information.A Mississippi Short Sale or Arms Length Affidavit is a legal document used in the state of Mississippi to ensure fair practices are followed during a property short sale transaction. This affidavit is typically required by lenders and serves as an acknowledgment from all parties involved, including the buyer, seller, and real estate agents, that the transaction is being conducted at arm's length. An arm's length transaction signifies that the buyer and seller have no existing relationship that could potentially influence the sale price or terms. It ensures that the market value is accurately represented, preventing any potential fraud or unethical practices in the transaction. This type of affidavit is crucial in maintaining transparency and preventing any conflicts of interest. The Mississippi Short Sale or Arms Length Affidavit may vary slightly in content from one lender or transaction to another. However, the main purpose of this document remains the same. It requires the parties involved to disclose any known relationships, financial interests, or affiliations that could influence the transaction. Some of the keywords that are relevant to this topic include "Mississippi short sale," "affidavit," "arms-length transaction," "property sale," "real estate transaction," "buyer," "seller," "lender," and "conflict of interest." It is important to note that the specific details and requirements of the Mississippi Short Sale or Arms Length Affidavit may vary, and it is advisable to consult with a real estate attorney or the lender for accurate and up-to-date information.