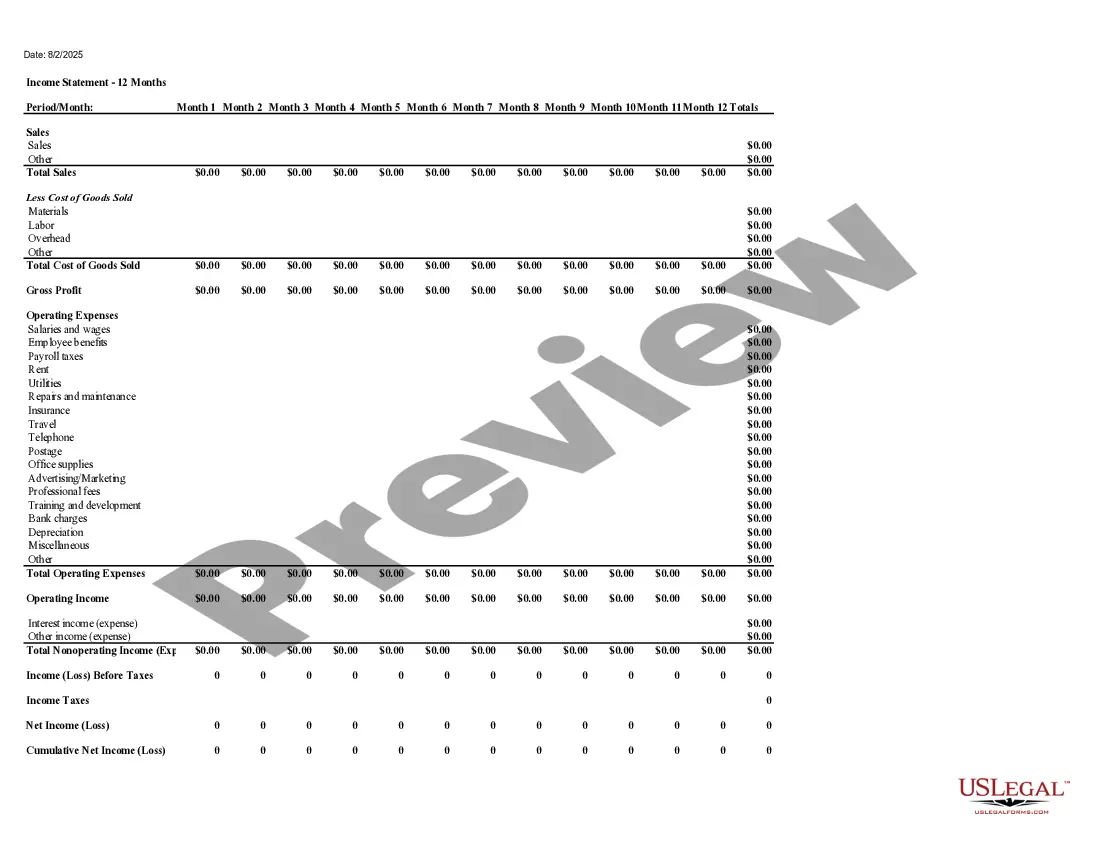

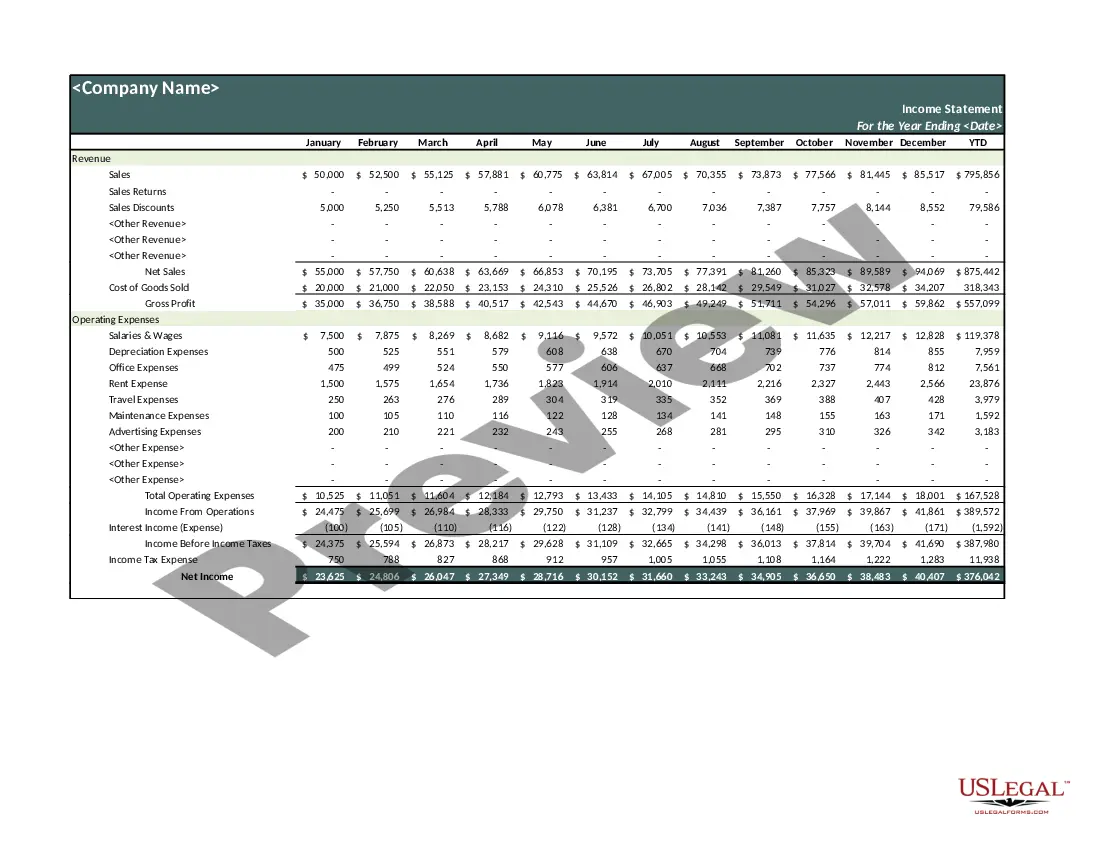

An income statement (sometimes called a profit and loss statement) lists your revenues and expenses, and tells you the profit or loss of your business for a given period of time. You can use this income statement form as a starting point to create one yourself.

Mississippi Income Statement

Category:

State:

Multi-State

Control #:

US-03600BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Income Statement?

You can spend hours online trying to locate the legal document template that complies with the federal and state requirements you need.

US Legal Forms offers a vast array of legal forms that are reviewed by experts.

It is easy to download or print the Mississippi Income Statement from our service.

If available, use the Preview option to inspect the document template as well.

- If you possess a US Legal Forms account, you can Log In and select the Download option.

- After that, you may complete, modify, print, or sign the Mississippi Income Statement.

- Every legal document template you purchase belongs to you indefinitely.

- To obtain another copy of a purchased form, navigate to the My documents tab and click on the appropriate option.

- If it's your first time using the US Legal Forms website, follow the straightforward instructions below.

- First, ensure you have chosen the correct document template for the area/city of your choice.

- Review the form description to confirm that you have selected the right form.

Form popularity

FAQ

Writing an income statement can be straightforward with the right approach. Start by documenting your total revenue and costs associated with goods sold. Next, itemize your operating expenses. Finally, present the net income, summarizing your financial performance effectively. This method ensures clarity in your Mississippi Income Statement.

To calculate an income statement, first, gather all income sources to determine total revenue. Then, deduct expenses related to goods sold to find gross profit. Following this, subtract operating expenses and other costs to arrive at your net income. These clear calculations will help you accurately present your Mississippi Income Statement.

Calculating an income statement involves a systematic approach. Start with total revenue, and deduct direct costs to find gross profit. Next, subtract operating expenses and any taxes. This will give you your net income, clearly reflecting your financial situation in the Mississippi Income Statement.

Filling out an income statement requires accurate data entry. Begin with total revenue and followed by deducting the costs associated with goods sold. Then, list your operating expenses and subtract them to calculate your net income. This process ensures proper documentation, essential for a reliable Mississippi Income Statement.

To fill out Mississippi employee's withholding exemption, start with the Employee's Withholding Exemption Certificate (Form 89-250). Provide your personal information, such as your name, address, and Social Security number. Next, indicate the number of exemptions you claim based on your situation. Lastly, submit the completed form to your employer to ensure accurate tax withholding based on your Mississippi Income Statement.

Individuals who do not meet the income thresholds set by the state are not required to file taxes in Mississippi. Also, some individuals may be exempt if they have no taxable income, such as those relying solely on Social Security. To ensure you understand your obligations, consider using tools like the Mississippi Income Statement to find comprehensive guidance.

In Mississippi, the income threshold that requires you to file taxes changes according to your filing status and age. Generally, if you earn more than a certain amount, you will need to submit a Mississippi Income Statement. To avoid any confusion, review the income levels each tax year or consult with an experienced tax professional.

To file your income tax statement in Mississippi, you can either complete the forms manually or use an online platform like uslegalforms. An online solution can guide you through the process step by step, reducing the risk of errors. Make sure to gather all necessary documents before you begin, so you can efficiently complete your Mississippi Income Statement.

You must file a Mississippi income tax return if you are a resident or part-year resident with an income exceeding the state’s filing threshold. This requirement applies to various income levels, so it’s essential to review the specifics of your financial situation. Using the Mississippi Income Statement makes filing your taxes more straightforward and helps ensure compliance with state laws.

In Mississippi, certain types of income may be exempt from state income tax. Common exemptions include Social Security benefits, unemployment benefits, and certain retirement income. These income sources do not need to be reported on your Mississippi Income Statement, which can simplify your tax filing process.