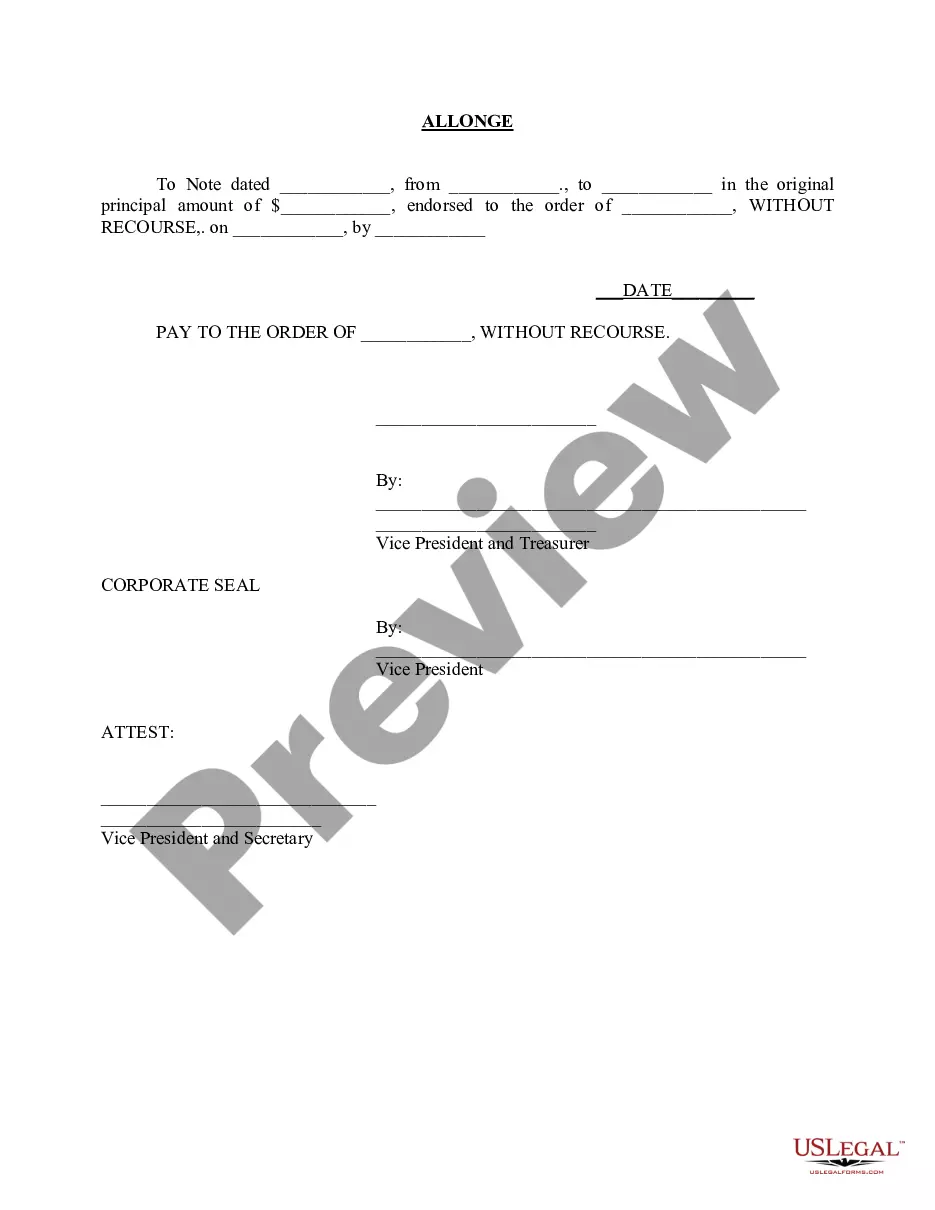

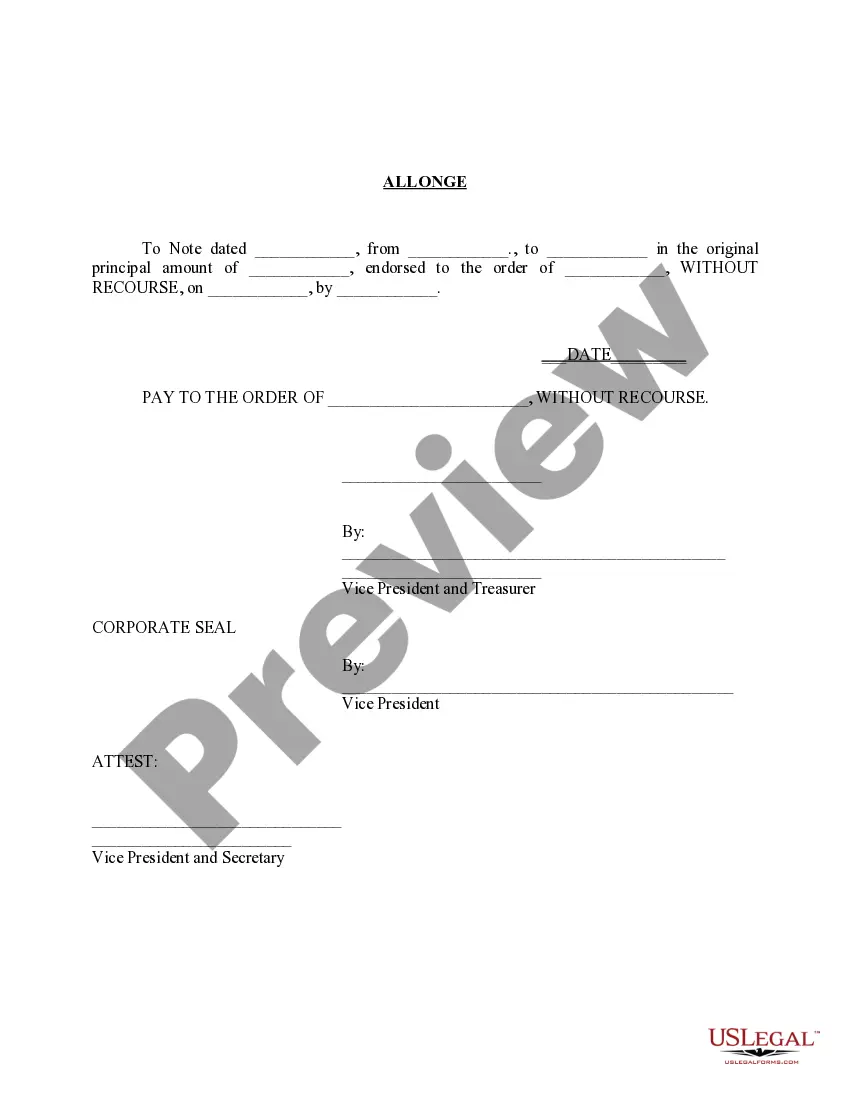

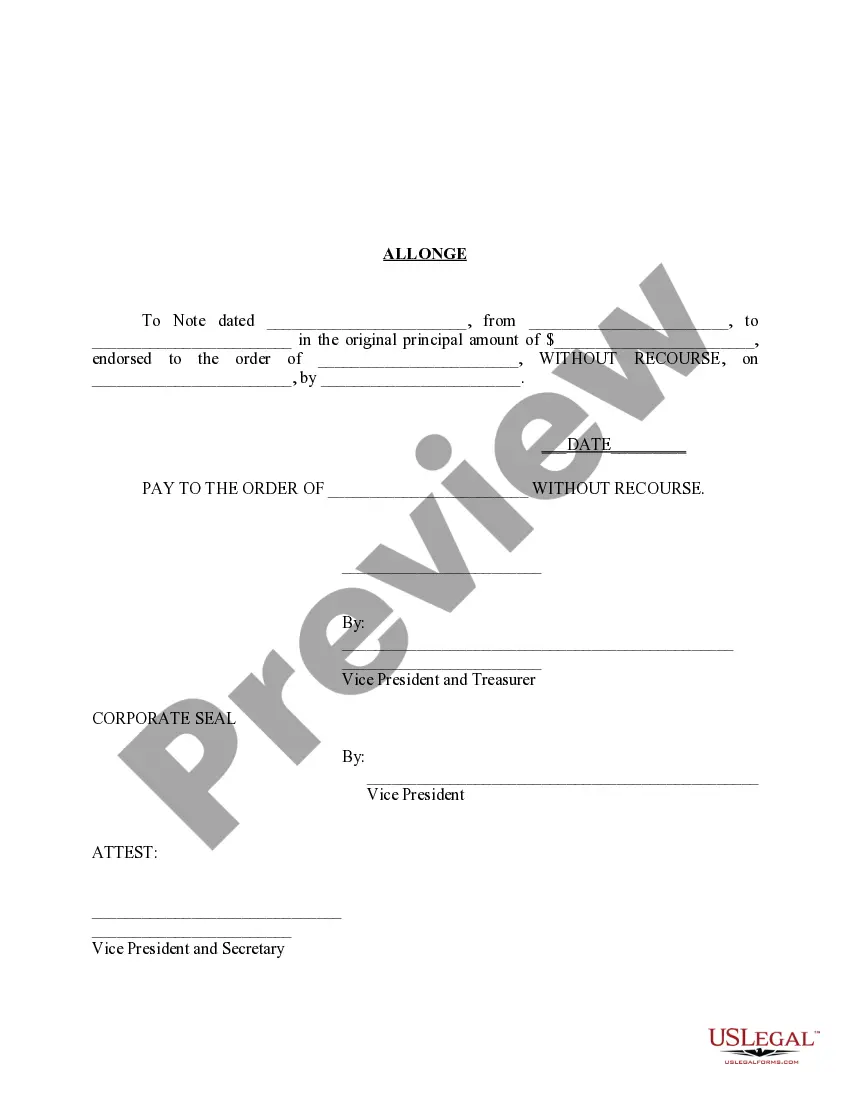

The Mississippi Along is a legal term referring to a specific type of document used in financial transactions, primarily in the context of promissory notes or bills of exchange. It serves as an endorsement or an attachment to the original instrument, adding information or altering its terms. It is a supplementary document that allows for the transfer or assignment of the instrument to another party, typically a lender or a financial institution. The Mississippi Along is commonly utilized in the mortgage industry when loans are sold or transferred between financial institutions. It ensures a smooth transfer of ownership and legal rights associated with the promissory note. The document usually contains details regarding the assignment, such as the original lender's name, the new lender's information, the date of transfer, and any specific conditions or limitations. There are several types or variations of Mississippi Alleges based on the specific purpose or conditions attached to the assignment. These include: 1. Blank Along: A blank endorsement where the Along does not contain the name of the new lender. This type allows for the note to be transferred to any subsequent holder or bearer. 2. Special Along: This type specifies the name of the new lender or assignee, providing a more restrictive transfer of ownership. 3. Restrictive Along: An Along that contains specific conditions or limitations on the transfer of the instrument. It may include provisions stating the note can only be transferred if certain criteria are met. 4. Qualified Along: This variation is used when the endorsement requires specific qualifications or qualifications of the entity accepting the transfer. For example, a bank may only accept the note if the assignee meets certain financial requirements. To summarize, a Mississippi Along is a legal document used in the transfer or assignment of promissory notes and bills of exchange, primarily in the mortgage industry. Various types of Alleges exist, including blank, special, restrictive, and qualified, each serving different purposes and containing unique conditions for endorsement. These documents play a crucial role in ensuring the smooth and lawful transfer of financial instruments between parties involved in the loan process.

Mississippi Allonge

Description

How to fill out Mississippi Allonge?

If you have to complete, obtain, or print out legitimate record templates, use US Legal Forms, the biggest selection of legitimate types, which can be found on the web. Make use of the site`s basic and hassle-free research to find the files you will need. A variety of templates for organization and specific uses are sorted by groups and suggests, or search phrases. Use US Legal Forms to find the Mississippi Allonge within a couple of mouse clicks.

If you are already a US Legal Forms buyer, log in for your bank account and click the Obtain option to get the Mississippi Allonge. You can also access types you formerly acquired in the My Forms tab of your own bank account.

Should you use US Legal Forms the first time, refer to the instructions beneath:

- Step 1. Be sure you have chosen the form to the appropriate area/country.

- Step 2. Utilize the Preview method to look over the form`s content material. Do not overlook to see the description.

- Step 3. If you are unsatisfied using the form, use the Look for area at the top of the screen to locate other versions in the legitimate form web template.

- Step 4. Once you have found the form you will need, click on the Get now option. Choose the rates prepare you like and put your qualifications to register on an bank account.

- Step 5. Process the transaction. You should use your charge card or PayPal bank account to perform the transaction.

- Step 6. Choose the structure in the legitimate form and obtain it in your product.

- Step 7. Complete, modify and print out or indication the Mississippi Allonge.

Each and every legitimate record web template you get is your own property forever. You possess acces to each form you acquired with your acccount. Click the My Forms area and choose a form to print out or obtain again.

Compete and obtain, and print out the Mississippi Allonge with US Legal Forms. There are thousands of professional and status-particular types you can use for the organization or specific requirements.