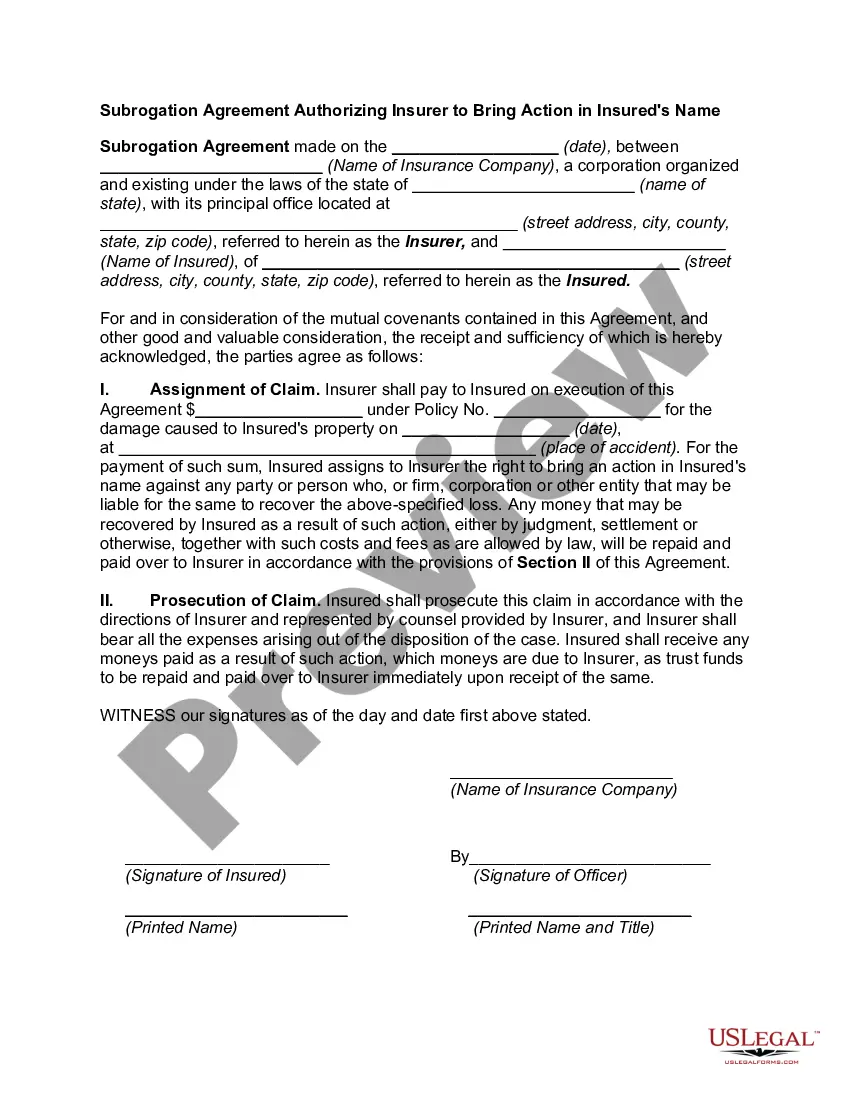

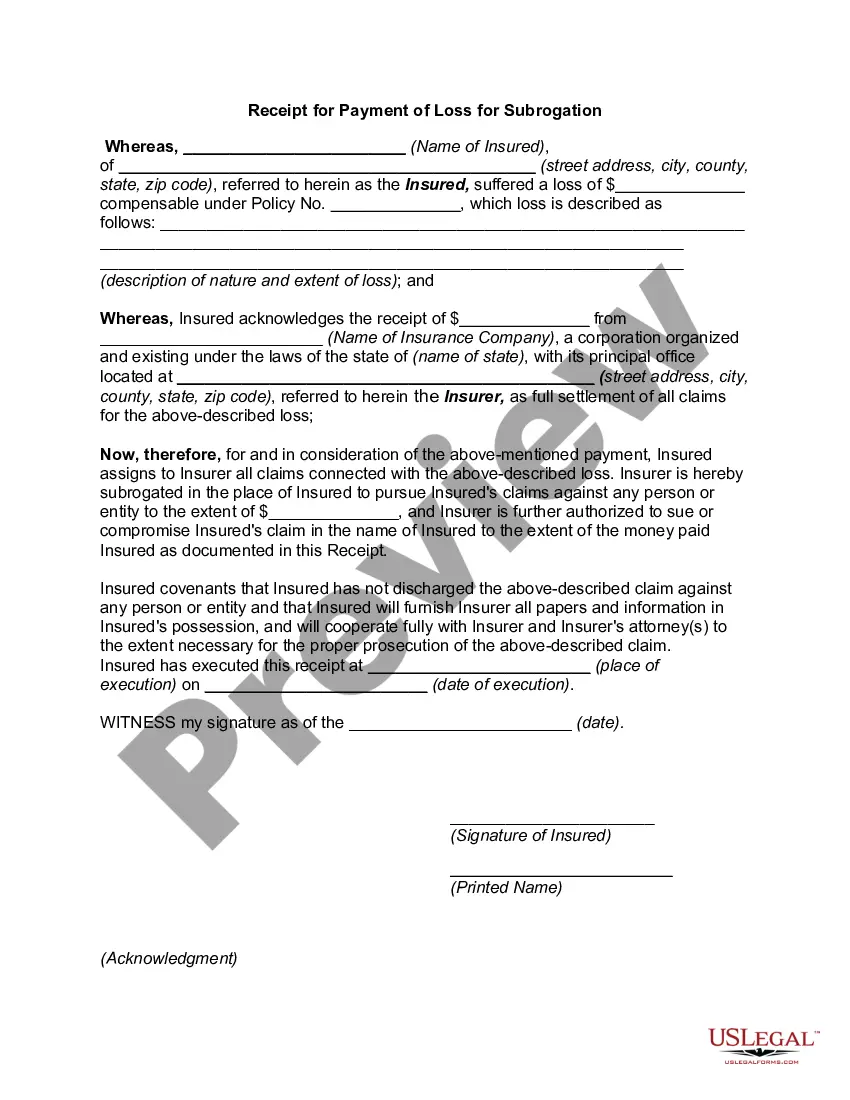

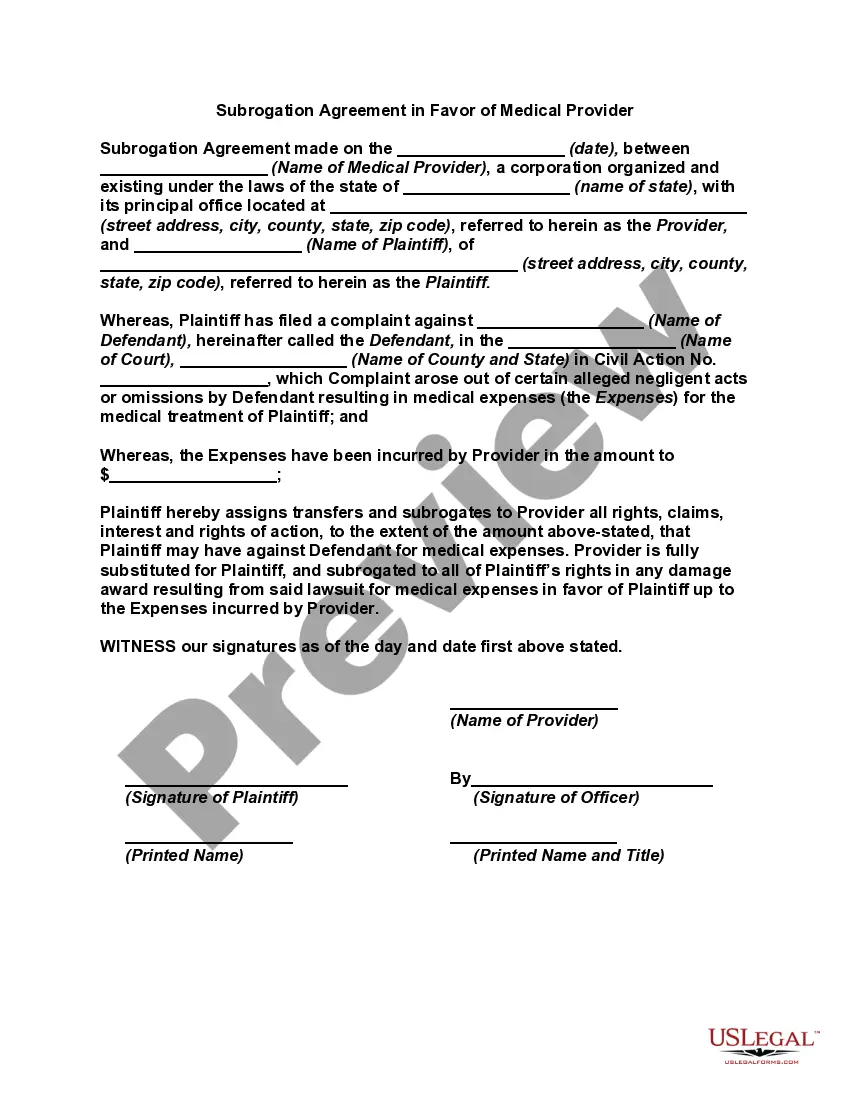

Mississippi Subrogation Agreement between Insurer and Insured

Description

How to fill out Subrogation Agreement Between Insurer And Insured?

You can devote hrs on the web trying to find the lawful file design that fits the state and federal demands you require. US Legal Forms offers thousands of lawful kinds that are examined by experts. You can easily acquire or print out the Mississippi Subrogation Agreement between Insurer and Insured from our services.

If you already possess a US Legal Forms account, it is possible to log in and click on the Down load switch. Afterward, it is possible to full, modify, print out, or sign the Mississippi Subrogation Agreement between Insurer and Insured. Every lawful file design you get is your own property permanently. To have yet another copy associated with a acquired form, check out the My Forms tab and click on the related switch.

If you work with the US Legal Forms site for the first time, stick to the simple instructions listed below:

- Initially, make certain you have selected the proper file design to the region/area of your liking. Look at the form explanation to make sure you have selected the proper form. If offered, make use of the Review switch to search through the file design also.

- In order to locate yet another model from the form, make use of the Lookup field to get the design that fits your needs and demands.

- After you have identified the design you need, click Acquire now to carry on.

- Find the prices program you need, type your qualifications, and register for an account on US Legal Forms.

- Complete the purchase. You may use your charge card or PayPal account to purchase the lawful form.

- Find the formatting from the file and acquire it to the device.

- Make alterations to the file if necessary. You can full, modify and sign and print out Mississippi Subrogation Agreement between Insurer and Insured.

Down load and print out thousands of file web templates using the US Legal Forms web site, which offers the greatest collection of lawful kinds. Use expert and status-distinct web templates to handle your company or personal needs.

Form popularity

FAQ

Subrogation refers to the right of an insurance company to recover money it paid to or on behalf of its insureds due to the actions of at-fault third parties.

What is Subrogation? Subrogation in insurance is a legal right of the insurance company to legally pursue a third-party responsible for the damages/insurance loss caused to the insured. Subrogation is done to recover the claim amount insurance company pays to the insured for the damages.

When you file a claim, your insurer can try to recover costs from the person responsible for your injury or property damage. This is known as subrogation. For example: Your insurance company pays your doctor for your treatment following an auto accident that someone else caused.

"Subrogation," or "subro" for short, refers to the right your insurance company holds under your policy ? after they've paid a covered claim ? to request reimbursement from the at-fault party. This reimbursement often comes from the at-fault party's insurance company.

Generally, in most subrogation cases, an individual's insurance company pays its client's claim for losses directly, then seeks reimbursement from the other party's insurance company. Subrogation is most common in an auto insurance policy but also occurs in property/casualty and healthcare policy claims.

An insurer may attempt to subrogate against an additional insured for completed operations injuries caused by the insured if the additional insured endorsement provides coverage only for ongoing operations injuries.

An insurance company may not subrogate against its own insured or a co-insured. However, when a party claiming to be a co-insured is merely a loss payee to which no liability coverage is afforded, subrogation is permissible.