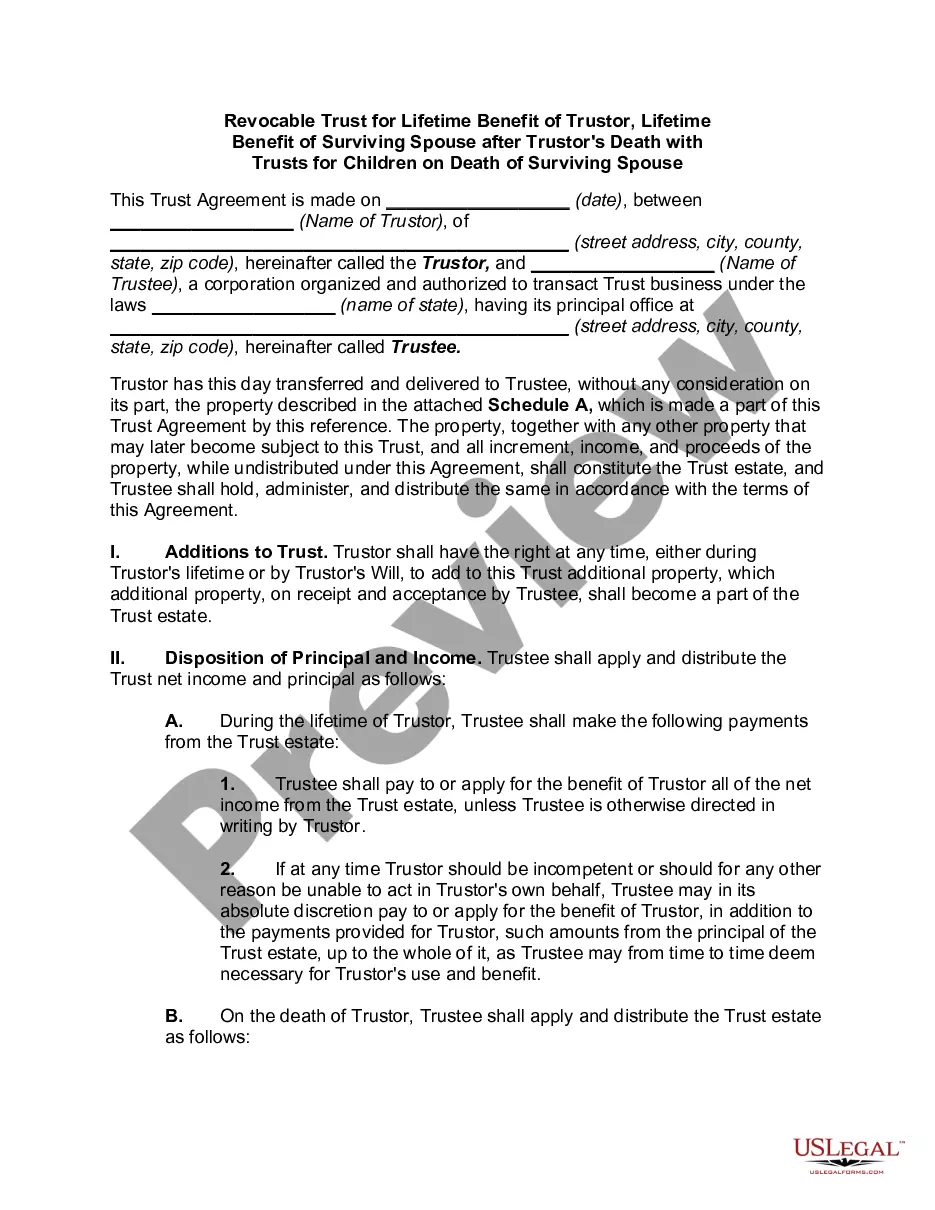

Mississippi Revocable Trust for Lifetime Benefit of Trustor for Lifetime Benefit of Surviving Spouse after Death of Trustor's with Annuity

Description

How to fill out Revocable Trust For Lifetime Benefit Of Trustor For Lifetime Benefit Of Surviving Spouse After Death Of Trustor's With Annuity?

You might spend time online trying to locate the legal document template that meets the federal and state requirements you are looking for.

US Legal Forms offers thousands of legal templates that have been reviewed by experts.

You can easily download or print the Mississippi Revocable Trust for Lifetime Benefit of Trustor for Lifetime Benefit of Surviving Spouse after the Trustor's Death with Annuity from my assistance.

If available, utilize the Preview feature to view the document format as well.

- If you already possess a US Legal Forms account, you can sign in and then click the Download button.

- Subsequently, you can fill out, modify, print, or sign the Mississippi Revocable Trust for Lifetime Benefit of Trustor for Lifetime Benefit of Surviving Spouse after the Trustor's Death with Annuity.

- Every legal document template you purchase is yours forever.

- To obtain another copy of any purchased form, visit the My documents section and click the appropriate link.

- If you are using the US Legal Forms website for the first time, follow the simple directions below.

- First, ensure that you have selected the correct document template for your location/region of your choice.

- Review the form description to confirm that you have chosen the correct template.

Form popularity

FAQ

After the death of the grantorThe income earned by trust assets after your passing will be listed on the trust's own, separate income tax return. The trust will need to file an annual fiduciary income tax return (on Form 1041).

A revocable living trust becomes irrevocable once the sole grantor or dies or becomes mentally incapacitated. If you have a joint trust for you and your spouse, then a portion of the joint trust can become irrevocable when the first spouse dies and will become irrevocable when the last spouse dies.

A revocable trust is a trust whereby provisions can be altered or canceled dependent on the grantor or the originator of the trust. During the life of the trust, income earned is distributed to the grantor, and only after death does property transfer to the beneficiaries of the trust.

But when the Trustee of a Revocable Trust dies, it is up to their Successor to settle their loved one's affairs and close the Trust. The Successor Trustee follows what the Trust lays out for all assets, property, and heirlooms, as well as any special instructions.

After one spouse dies, the surviving spouse is free to amend the terms of the trust document that deal with his or her property, but can't change the parts that determine what happens to the deceased spouse's trust property. You can make a valid living trust online, quickly and easily, with Nolo's Online Living Trust.

What happens in this type of trust is that the trust is a joint revocable trust when both spouses are alive. When one of the spouses dies, the trust will then split into two trusts automatically. Each trust will have half the assets of the trust along with the separate property of the spouse.

Under typical circumstances, the surviving spouse would become the sole trustee after the death of one spouse. The surviving spouse would control the shared property, and the personal property of the deceased spouse would be distributed to the beneficiaries.

Trust beneficiaries must pay taxes on income and other distributions that they receive from the trust. Trust beneficiaries don't have to pay taxes on returned principal from the trust's assets. IRS forms K-1 and 1041 are required for filing tax returns that receive trust disbursements.

Upon the death of the grantor, grantor trust status terminates, and all pre-death trust activity must be reported on the grantor's final income tax return. As mentioned earlier, the once-revocable grantor trust will now be considered a separate taxpayer, with its own income tax reporting responsibility.

What Happens When One Spouse Dies. While both spouses are alive, they typically act as co-trustees and manage the trust together. Upon the death of the first spousealso known as the decedent spousethe surviving spouse generally becomes the sole grantor/trustee and continues to manage the trust based on its terms.