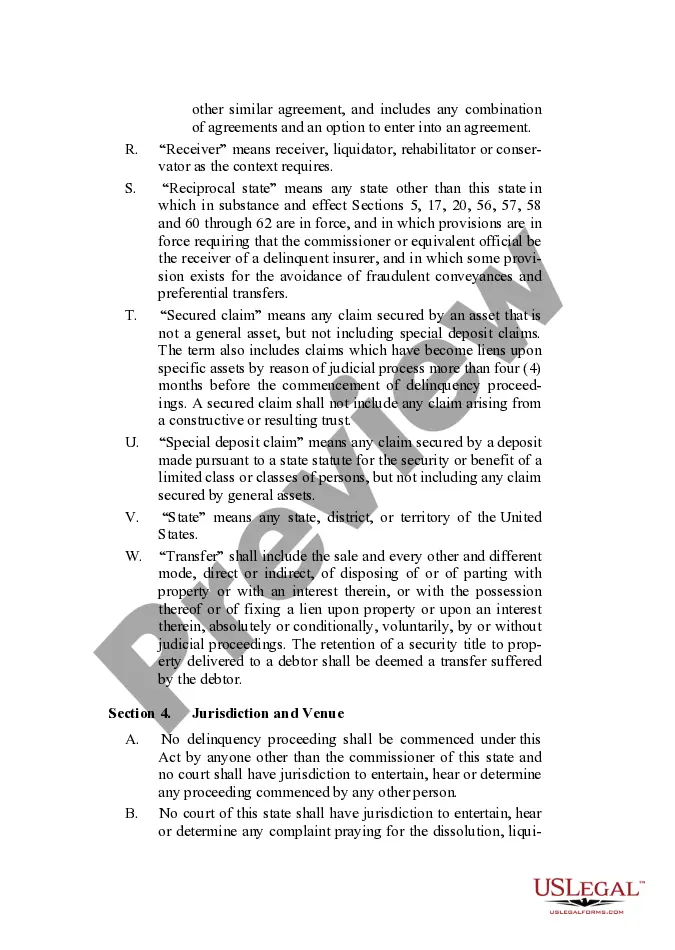

Full text and statutory guidelines for the Insurers Rehabilitation and Liquidation Model Act.

The Mississippi Insurers Rehabilitation and Liquidation Model Act (MIRA) is a legal framework that governs the rehabilitation and eventual liquidation of financially troubled insurance companies in the state of Mississippi. This act aims to protect the interests of policyholders and ensure the orderly and fair resolution of insolvent insurance companies. Under the MIRA, the Mississippi Insurance Commissioner is appointed as the receiver of a troubled insurance company. The Commissioner has the authority to take control of the company's assets, operations, and administration to rehabilitate or liquidate the insurer. The goal is to maximize the value of assets and minimize potential losses for policyholders, creditors, and other interested parties. The act outlines a detailed procedure for the initiation of rehabilitation or liquidation proceedings, including the appointment of an ancillary receiver if necessary. It provides guidelines for establishing and maintaining a claim filing process, conducting investigations, and enforcing obligations of the insurer and its policyholders. Keywords: Mississippi Insurers Rehabilitation and Liquidation Model Act, MIRA, rehabilitation, liquidation, financially troubled insurance companies, policyholders, insolvent, orderly resolution, Mississippi Insurance Commissioner, receiver, assets, administration, maximize value, minimize losses, creditors, interested parties, initiation of proceedings, ancillary receiver, claim filing process, investigations, obligations. Different types of the Mississippi Insurers Rehabilitation and Liquidation Model Act may include: 1. MIRA Amendments: These are additional legislative updates made to the original act to address changing industry practices, regulations, or enhancements in protection for policyholders and creditors. 2. MIRA Regulations: These are specific rules formulated by the Mississippi Insurance Commissioner's office to provide detailed guidance on implementing and interpreting the MIRA provisions. These regulations may cover aspects such as claims handling, financial reporting requirements, or the role of the Commissioner during rehabilitation or liquidation proceedings. 3. MIRA Case Law: Over time, court decisions related to the MIRA have contributed to shaping and refining its interpretation and application. Examining case law can provide a deeper understanding of how the act is implemented and the legal precedents established in Mississippi. 4. Model Act Comparison: It is worth noting that other states may have adopted similar rehabilitation and liquidation model acts. Comparing the Mississippi Insurers Rehabilitation and Liquidation Model Act with those of other states can reveal potential similarities or differences, highlighting best practices or areas for improvement. Overall, the Mississippi Insurers Rehabilitation and Liquidation Model Act is a vital legal framework that coordinates the rehabilitation or liquidation of financially troubled insurance companies in Mississippi to safeguard the interests of policyholders, creditors, and other stakeholders.The Mississippi Insurers Rehabilitation and Liquidation Model Act (MIRA) is a legal framework that governs the rehabilitation and eventual liquidation of financially troubled insurance companies in the state of Mississippi. This act aims to protect the interests of policyholders and ensure the orderly and fair resolution of insolvent insurance companies. Under the MIRA, the Mississippi Insurance Commissioner is appointed as the receiver of a troubled insurance company. The Commissioner has the authority to take control of the company's assets, operations, and administration to rehabilitate or liquidate the insurer. The goal is to maximize the value of assets and minimize potential losses for policyholders, creditors, and other interested parties. The act outlines a detailed procedure for the initiation of rehabilitation or liquidation proceedings, including the appointment of an ancillary receiver if necessary. It provides guidelines for establishing and maintaining a claim filing process, conducting investigations, and enforcing obligations of the insurer and its policyholders. Keywords: Mississippi Insurers Rehabilitation and Liquidation Model Act, MIRA, rehabilitation, liquidation, financially troubled insurance companies, policyholders, insolvent, orderly resolution, Mississippi Insurance Commissioner, receiver, assets, administration, maximize value, minimize losses, creditors, interested parties, initiation of proceedings, ancillary receiver, claim filing process, investigations, obligations. Different types of the Mississippi Insurers Rehabilitation and Liquidation Model Act may include: 1. MIRA Amendments: These are additional legislative updates made to the original act to address changing industry practices, regulations, or enhancements in protection for policyholders and creditors. 2. MIRA Regulations: These are specific rules formulated by the Mississippi Insurance Commissioner's office to provide detailed guidance on implementing and interpreting the MIRA provisions. These regulations may cover aspects such as claims handling, financial reporting requirements, or the role of the Commissioner during rehabilitation or liquidation proceedings. 3. MIRA Case Law: Over time, court decisions related to the MIRA have contributed to shaping and refining its interpretation and application. Examining case law can provide a deeper understanding of how the act is implemented and the legal precedents established in Mississippi. 4. Model Act Comparison: It is worth noting that other states may have adopted similar rehabilitation and liquidation model acts. Comparing the Mississippi Insurers Rehabilitation and Liquidation Model Act with those of other states can reveal potential similarities or differences, highlighting best practices or areas for improvement. Overall, the Mississippi Insurers Rehabilitation and Liquidation Model Act is a vital legal framework that coordinates the rehabilitation or liquidation of financially troubled insurance companies in Mississippi to safeguard the interests of policyholders, creditors, and other stakeholders.