Mississippi General Consent Form for Qualified Joint and Survivor Annuities - QJSA

Description

How to fill out General Consent Form For Qualified Joint And Survivor Annuities - QJSA?

US Legal Forms - one of the largest collections of legal documents in the United States - presents a selection of legal form templates that you can download or print.

By using the website, you can discover thousands of forms for business and personal needs, organized by categories, states, or keywords. You can access the latest versions of forms, such as the Mississippi General Consent Form for Qualified Joint and Survivor Annuities - QJSA, within moments.

If you have a subscription, Log In and download the Mississippi General Consent Form for Qualified Joint and Survivor Annuities - QJSA from the US Legal Forms collection. The Download button will display on every form you view. You can access all previously saved forms in the My documents section of your account.

Process the transaction. Use your Visa or Mastercard or PayPal account to complete the purchase.

Select the format and download the form onto your device. Edit and print the saved Mississippi General Consent Form for Qualified Joint and Survivor Annuities - QJSA.

Any form you add to your account has no expiration date and is yours indefinitely. Therefore, if you wish to download or print another copy, just head to the My documents section and click on the form you desire.

Access the Mississippi General Consent Form for Qualified Joint and Survivor Annuities - QJSA with US Legal Forms, the largest collection of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs.

- If you are using US Legal Forms for the first time, here are simple steps to help you get started.

- Ensure you have selected the correct form for your city/county.

- Click the Preview button to review the form's content.

- Check the form details to make sure you have the right document.

- If the form doesn’t meet your requirements, utilize the Search box at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your selection by clicking the Buy now button.

- Then, select the pricing plan you prefer and provide your information to register for an account.

Form popularity

FAQ

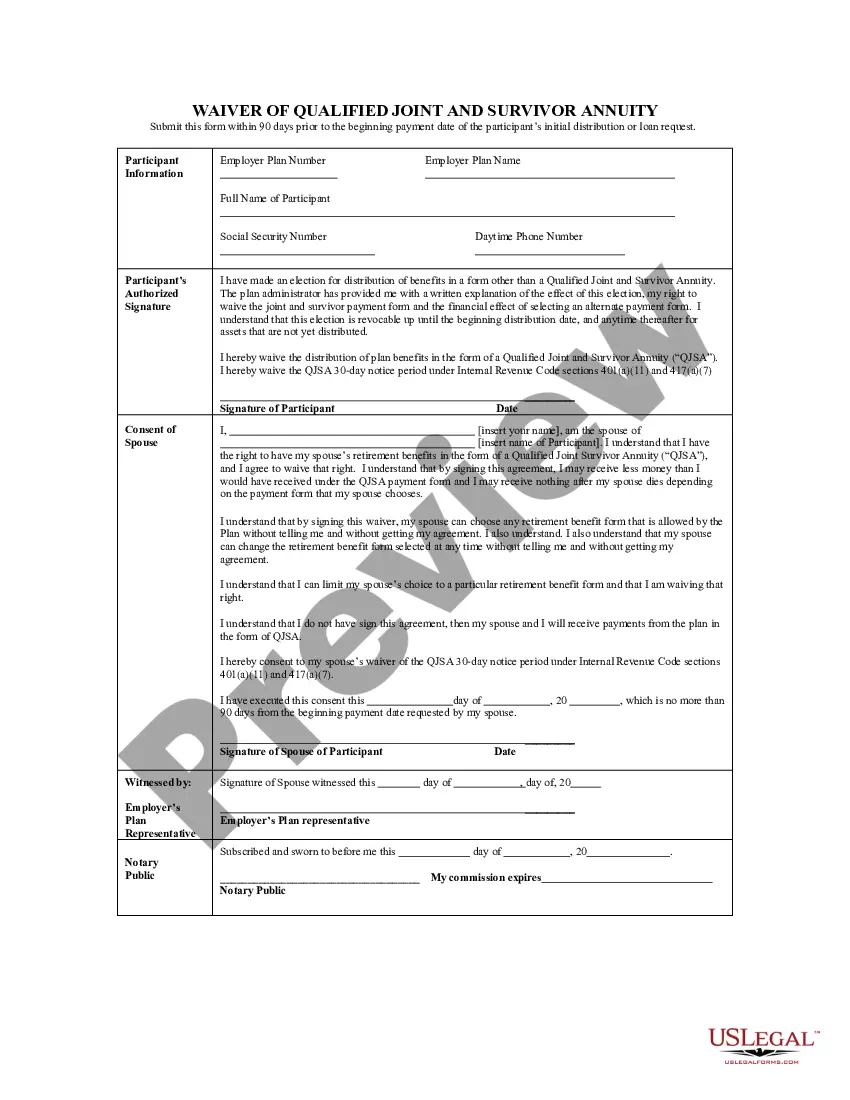

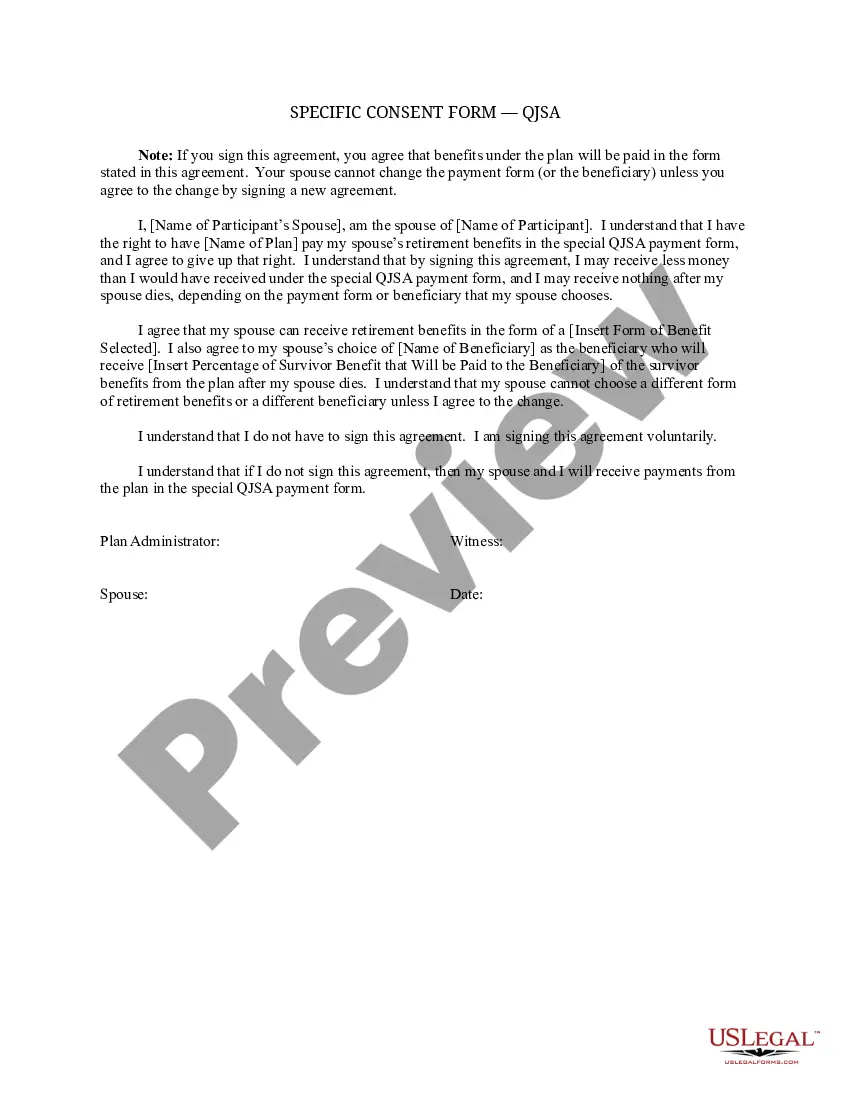

The QJSA payment form gives your spouse, the annuitant, a retirement payment for the rest of his or her life. Under the QJSA payment form, after your spouse dies, the contract will pay you, the surviving spouse, at least 50% percent of the retirement benefit that was paid to your spouse, the annuitant.

A QJSA is when retirement benefits are paid as a life annuity (a series of payments, usually monthly, for life) to the participant and a survivor annuity over the life of the participant's surviving spouse (or a former spouse, child or dependent who must be treated as a surviving spouse under a QDRO) following the

A joint and survivor annuity is an insurance product designed for couples that continues to make regular payments as long as one spouse lives. A joint and survivor annuity has the advantage of providing income if one or both people live longer than expected. This is not a good choice for a younger couple.

A QJSA is when retirement benefits are paid as a life annuity (a series of payments, usually monthly, for life) to the participant and a survivor annuity over the life of the participant's surviving spouse (or a former spouse, child or dependent who must be treated as a surviving spouse under a QDRO) following the

Qualified Optional Survivor Annuity (QOSA) an immediate annuity for your life, with a survivor annu- ity for the life of your spouse which is equal to 75% of the amount of the annuity, which is payable during the joint lives of you and your spouse.

If you do not waive the QPSA, after your death the Plan will pay your spouse the QPSA unless your spouse elects another benefit form. The QPSA will not pay benefits to other beneficiaries after your spouse dies. If you waive the QPSA, the Plan will pay your account to your designated beneficiary.

Qualified Joint and Survivor Annuity (QJSA) includes a level monthly payment for your lifetime and a survivor benefit for your spouse after your death equal to the percentage designated of that monthly payment.

Spousal Waiver Form means that form established by the Plan Administrator, in its sole discretion, for use by a spouse to consent to the designation of another person as the Beneficiary or Beneficiaries under a Participant's Account.

ANSWER: Spousal consent is required if a married participant designates a nonspouse primary beneficiary and may be necessary if a 401(k) plan offers one or more annuity forms of distribution. Here is a summary of these rules and the way many 401(k) plans avoid spousal consents.