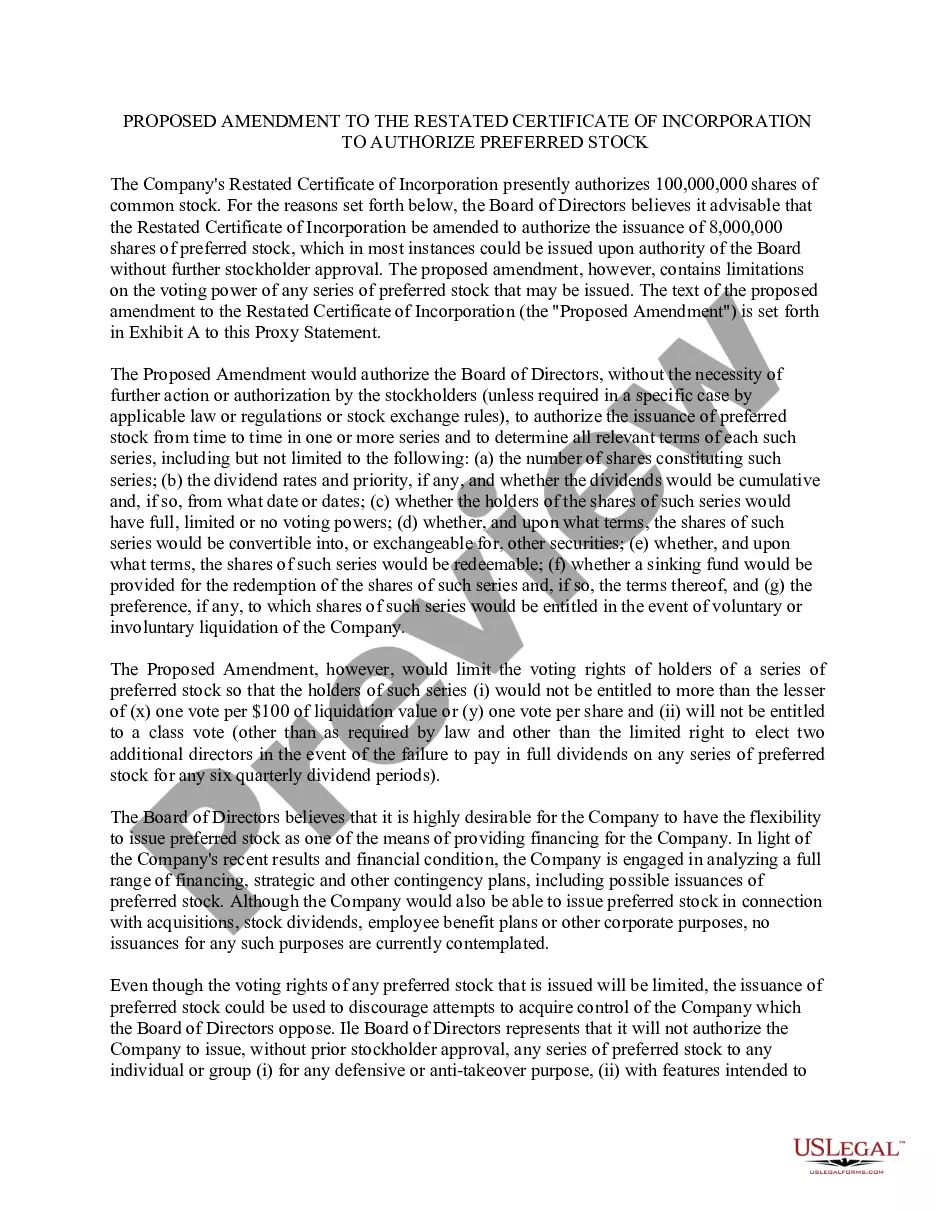

Mississippi Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

Are you inside a placement the place you need files for either enterprise or specific purposes nearly every day time? There are plenty of legitimate papers themes available online, but locating types you can depend on is not easy. US Legal Forms offers a large number of form themes, just like the Mississippi Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, that are composed to fulfill federal and state requirements.

If you are currently knowledgeable about US Legal Forms site and possess an account, basically log in. Afterward, it is possible to down load the Mississippi Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock web template.

Should you not come with an accounts and wish to begin to use US Legal Forms, follow these steps:

- Obtain the form you want and make sure it is to the right area/county.

- Use the Preview option to analyze the form.

- Browse the information to actually have selected the proper form.

- In the event the form is not what you`re trying to find, use the Lookup area to get the form that meets your needs and requirements.

- Once you find the right form, simply click Purchase now.

- Opt for the rates program you need, submit the required details to generate your account, and purchase the transaction making use of your PayPal or bank card.

- Pick a convenient document format and down load your version.

Find every one of the papers themes you might have bought in the My Forms food selection. You may get a more version of Mississippi Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock anytime, if necessary. Just click on the necessary form to down load or print out the papers web template.

Use US Legal Forms, the most considerable variety of legitimate types, to conserve time as well as avoid faults. The service offers professionally manufactured legitimate papers themes which you can use for a range of purposes. Produce an account on US Legal Forms and start making your life a little easier.

Form popularity

FAQ

Mississippi limited liability company's amendments may now be completed using the MS Secretary of State's online filing system. You will have the option to complete the whole process and pay online or print your amendment and mail it with a check payable to ?Secretary of State.?

After filing your original return and should you need to file an amended return, you must usually file an amended return by the later of these dates: Three years from the time you filed your original return. Two years from the date you paid the taxes on your return.

The IRS form for amending a return is Form 1040-X. You'll also need any forms that will be impacted by your change. For example, if you're changing your itemized deductions, you'll also need a copy of Schedule A for that tax year.

You can complete the amendments using the online filing system of the Secretary of State. You can choose to finish the whole process, including the $50 payment, online. But, if you want to mail the amendment, you have to print it and attach a check payable to the Secretary of State.

° When to file: Generally, to claim a refund, you must file Form 1040X within three years from the date you filed your original return or within two years from the date you paid the tax, whichever is later. ° Processing time: Normal processing time for amended returns is 8 to 12 weeks.