Summary Administration Package - Small Estates

Small Estates General Summary: Small Estate laws were enacted in order to enable heirs to obtain property of the deceased without probate, or with shortened probate proceedings, provided certain conditions are met. Small estates can be administered with less time and cost. If the deceased had conveyed most property to a trust but there remains some property, small estate laws may also be available. Small Estate procedures may generally be used regardless of whether there was a Will. In general, the two forms of small estate procedures are recognized:

1.Small Estate Affidavit -Some States allow an affidavit to be executed by the spouse and/or heirs of the deceased and present the affidavit to the holder of property such as a bank to obtain property of the deceased. Other states require that the affidavit be filed with the Court. The main requirement before you may use an affidavit is that the value of the personal and/or real property of the estate not exceed a certain value.

2.Summary Administration -Some states allow a Summary administration. Some States recognize both the Small Estate affidavit and Summary Administration, basing the requirement of which one to use on the value of the estate. Example: If the estate value is 10,000 or less an affidavit is allowed but if the value is between 10,000 to 20,000 a summary administration is allowed.

Montana Summary:

Under Montana statute, where as estate is valued at less than $50,000, an interested party may, thirty (30) days after the death of the decedent, issue a small estate affidavit to to demand payment on any debts owed to the decedent.

Montana Requirements:

Montana requirements are set forth in the statutes below.

Part 11 Collection of Personal Property by Affidavit and Summary Administration Procedure for Small Estates

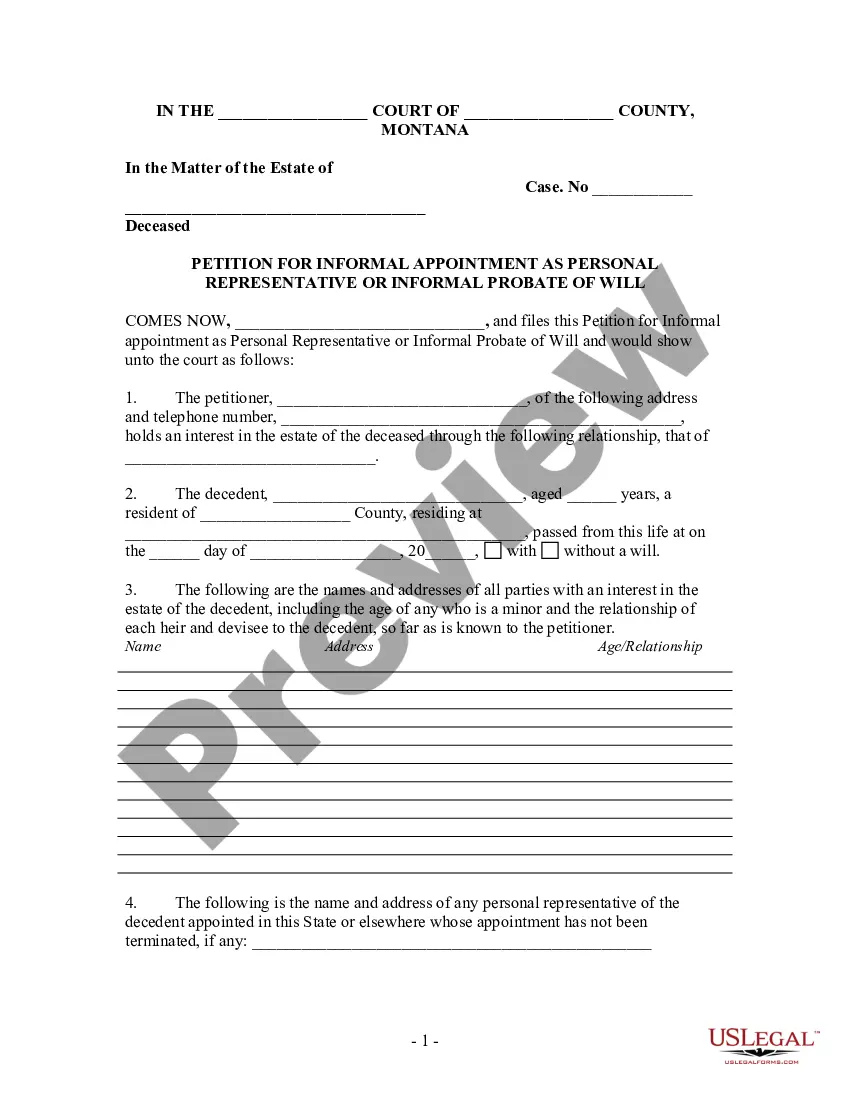

72-3-1101. Collection of personal property by affidavit.

(1) Thirty days after the death of a decedent, any person indebted to the decedent or having possession of tangible personal property or an instrument evidencing a debt, obligation, stock, or chose in action belonging to the decedent shall make payment of the indebtedness or deliver the tangible personal property or an instrument evidencing a debt, obligation, stock, or chose in action to a person claiming to be the successor of the decedent upon being presented an affidavit made by or on behalf of the successor stating that:

(a) the value of the entire estate, wherever located, less liens and encumbrances, does not exceed $50,000, except as provided in subsection (2);

(b) 30 days have elapsed since the death of the decedent;

(c) no application or petition for the appointment of a personal representative is pending or has been granted in any jurisdiction; and

(d) the claiming successor is entitled to payment or delivery of the property.

(2) The department of revenue may refund unclaimed property to a successor of the decedent, pursuant to the provisions of Title 70, chapter 9, part 8, if the value of the unclaimed property is $5,000 or less regardless of the value of the estate.

(3) A transfer agent of any security shall change the registered ownership on the books of a corporation from the decedent to the successor or successors upon the presentation of an affidavit as provided in subsection (1).

History: En. 91A-3-1201 by Sec. 1, Ch. 365, L. 1974; R.C.M. 1947, 91A-3-1201; amd. Sec. 1, Ch. 124, L. 1981; amd. Sec. 1, Ch. 234, L. 1999; amd. Sec. 2, Ch. 513, L. 2005; amd. Sec. 1, Ch. 85, L. 2013.

72-3-1102. Effect of affidavit.

(1) The person paying, delivering, transferring, or issuing personal property or the evidence of personal property pursuant to affidavit is discharged and released to the same extent as if the person dealt with a personal representative of the decedent. The person is not required to see to the application of the personal property or evidence of personal property or to inquire into the truth of any statement in the affidavit.

(2) If any person to whom an affidavit is delivered refuses to pay, deliver, transfer, or issue any personal property or evidence of personal property, it may be recovered or its payment, delivery, transfer, or issuance compelled upon proof of their right in a proceeding brought for the purpose by or on behalf of the persons entitled to the property.

(3) A person to whom payment, delivery, transfer, or issuance is made is answerable and accountable for the property to any person representative of the estate or to any other person having a superior right.

History: En. 91A-3-1202 by Sec. 1, Ch. 365, L. 1974; R.C.M. 1947, 91A-3-1202; amd. Sec. 2388, Ch. 56, L. 2009.

72-3-1103. Small estates -- summary administration procedure.

If it appears from the inventory and appraisal that the value of the entire estate, less liens and encumbrances, does not exceed homestead allowance, exempt property, family allowance, costs and expenses of administration, reasonable funeral expenses, and reasonable and necessary medical and hospital expenses of the last illness of the decedent, the personal representative, without giving notice to the creditors, may immediately disburse and distribute the estate to the persons entitled thereto and file a closing statement as provided in 72-3-1104.

History: En. 91A-3-1203 by Sec. 1, Ch. 365, L. 1974; R.C.M. 1947, 91A-3-1203; amd. Sec. 2, Ch. 124, L. 1981; amd. Sec. 16, Ch. 582, L. 1989.

72-3-1104. Small estates -- closing by sworn statement of personal representative.

(1) Unless prohibited by order of the court and except for estates being administered by supervised personal representatives, a personal representative may close an estate administered under the summary procedures of 72-3-1103 by filing with the court, at any time after disbursement and distribution of the estate, a verified statement stating that:

(a) to the best knowledge of the personal representative, the value of the entire estate, less liens and encumbrances, did not exceed homestead allowance, exempt property, family allowance, costs and expenses of administration, reasonable funeral expenses, and reasonable, necessary medical and hospital expenses of the last illness of the decedent;

(b) the personal representative has fully administered the estate by payment of estate taxes and by disbursing and distributing it to the persons entitled to it; and

(c) the personal representative has sent a copy of the closing statement to all distributees of the estate and to all creditors or other claimants of whom the personal representative is aware whose claims are neither paid nor barred and has furnished a full account in writing of the administration to the distributees whose interests are affected.

(2) If actions or proceedings involving the personal representative are not pending in the court 1 year after the closing statement is filed, the appointment of the personal representative terminates.

(3) A closing statement filed under this section has the same effect as one filed under 72-3-1004.

History: En. 91A-3-1204 by Sec. 1, Ch. 365, L. 1974; R.C.M. 1947, 91A-3-1204; amd. Sec. 3, Ch. 124, L. 1981; amd. Sec. 17, Ch. 582, L. 1989; amd. Sec. 23, Ch. 9, Sp. L. May 2000.