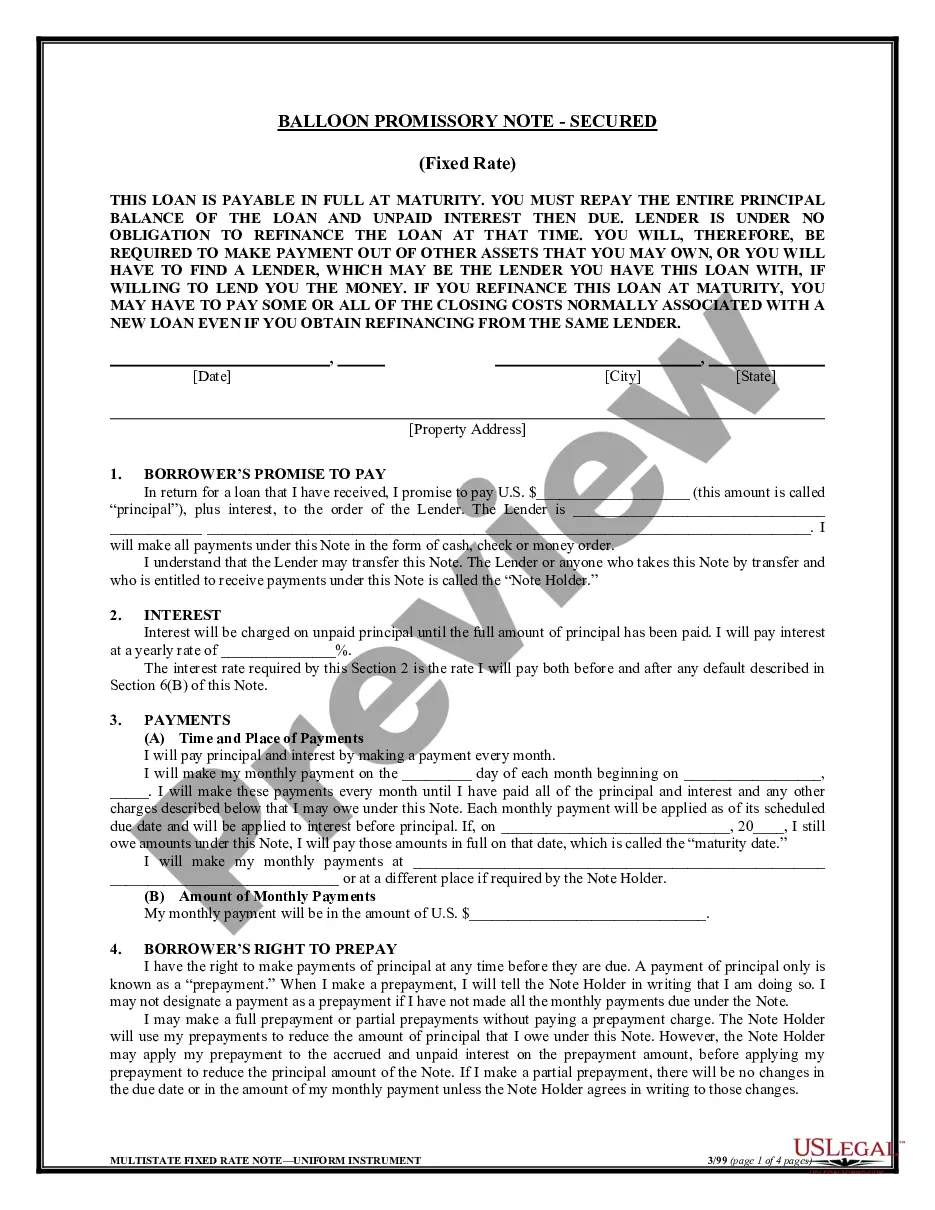

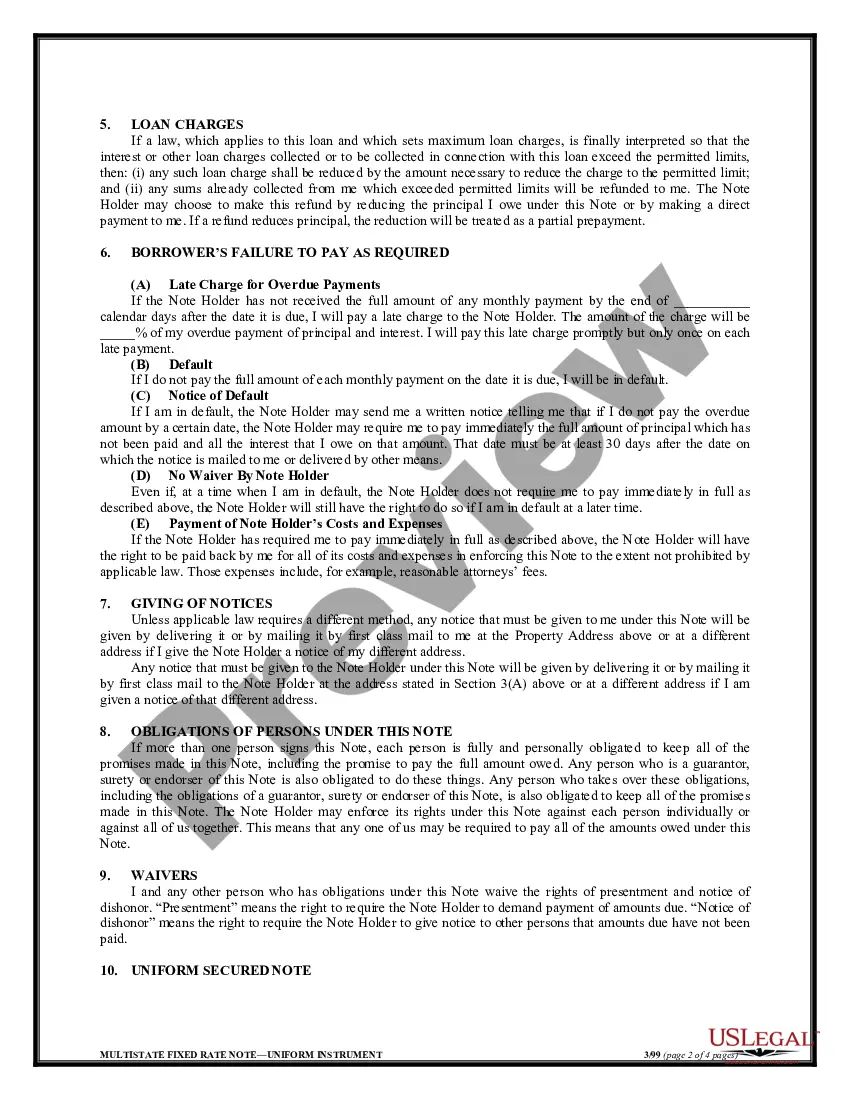

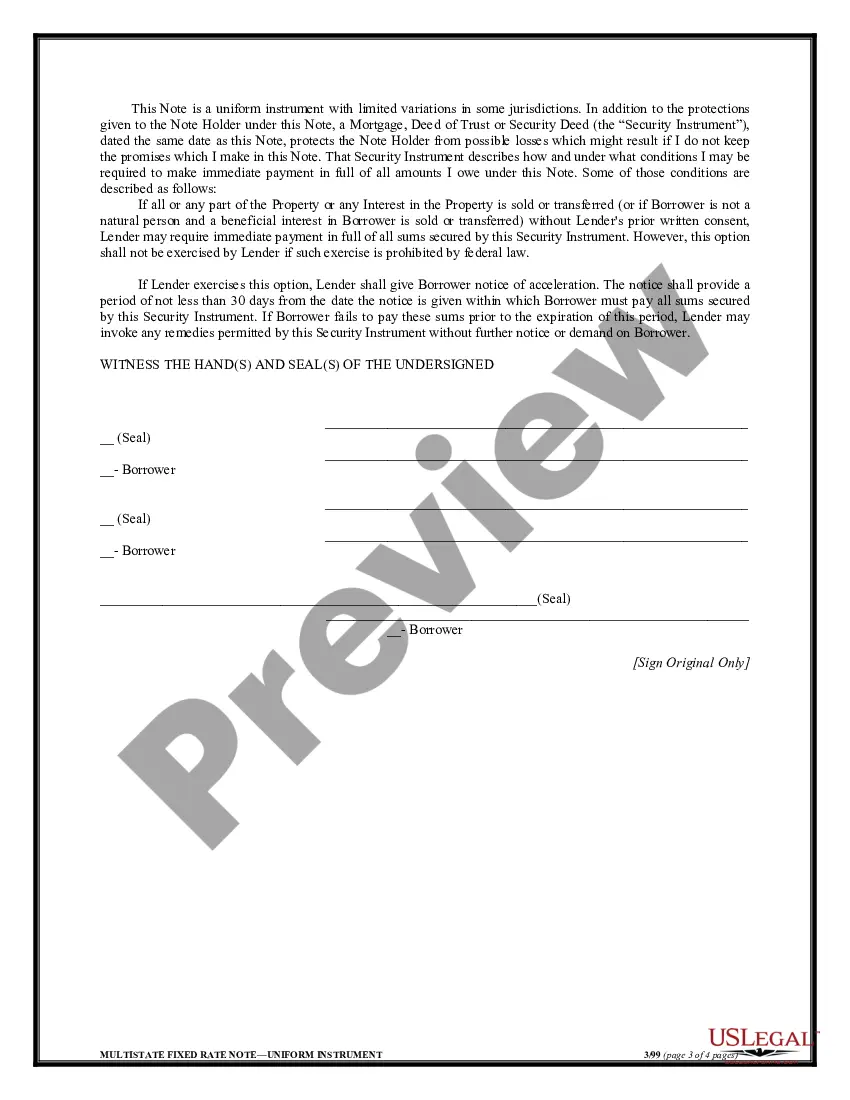

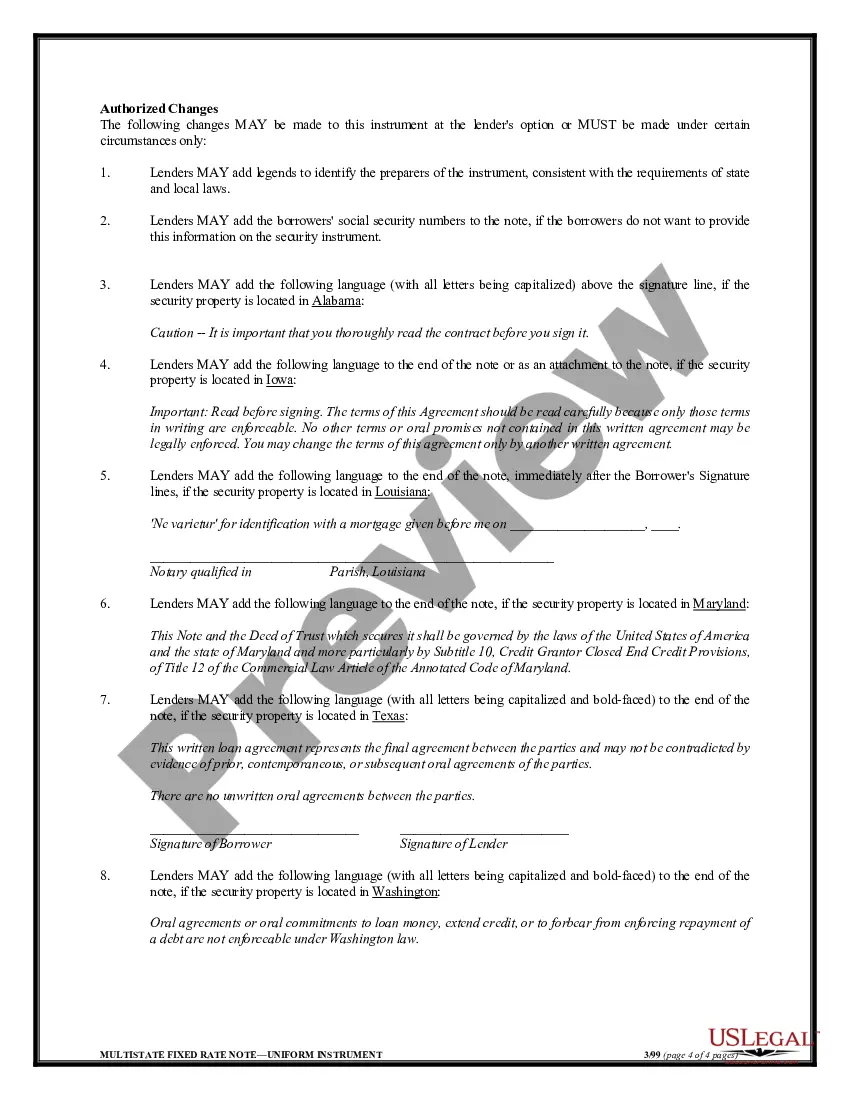

Montana Balloon Secured Note is a financial instrument commonly used in real estate transactions. It is a type of promissory note that involves a borrower promising to repay a loan alongside an additional "balloon payment" at the end of the loan term. This type of note is commonly used when the borrower requires a large amount of money upfront but expects to have increased resources or assets to fully repay the loan by the end of the term. The primary characteristic of a Montana Balloon Secured Note is the inclusion of a balloon payment. This payment is typically substantially higher than the regular installments made throughout the term of the loan. It serves as a way to minimize the borrower's regular payment obligations and allows them to use their available resources more effectively. The balloon payment is generally made at the end of the loan term, allowing borrowers to plan and budget accordingly. The "secured" aspect of the note refers to the collateral provided by the borrower to the lender to secure the loan. In the case of a Montana Balloon Secured Note, the collateral is usually a property or real estate asset. By using the property as collateral, the lender has the right to seize and sell the asset in the event of default on the loan, providing them with recourse to recover their investment. Montana Balloon Secured Note has different variations depending on the specific terms and conditions agreed upon by the borrower and lender: 1. Interest Rate Variation: This type of note may have a fixed or adjustable interest rate. A fixed rate remains the same throughout the term, providing stability and predictability in the borrower's repayment obligations. Conversely, an adjustable rate can fluctuate based on prevailing market conditions, which can be advantageous if rates decrease but can also increase the borrower's payment amounts. 2. Collateral Requirements: While real estate is a common form of collateral, other valuable assets such as vehicles, equipment, or inventory can also be used to secure the note. This variation allows borrowers to leverage their assets for financing, providing flexibility depending on their specific needs. 3. Loan Term: Balloon payments are typically associated with shorter loan terms, ranging from three to ten years. However, the specific loan term can differ, depending on the agreement between the borrower and the lender. Longer loan terms may have lower regular payments but would require a more significant balloon payment at the end. Montana Balloon Secured Note provides both borrowers and lenders with specific advantages. Borrowers can access significant upfront funds, enabling them to invest in projects or assets that may have significant long-term returns. Lenders can mitigate their risk by holding valuable collateral and receiving regular interest payments throughout the loan term, culminating in a substantial balloon payment at its expiration. However, it is essential for borrowers and lenders to carefully evaluate the terms and risks associated with Montana Balloon Secured Notes before engaging in such financial agreements.

Montana Balloon Secured Note

Description

How to fill out Montana Balloon Secured Note?

Finding the right legal file format might be a battle. Needless to say, there are tons of templates available online, but how will you obtain the legal type you want? Make use of the US Legal Forms web site. The support provides a large number of templates, such as the Montana Balloon Secured Note, that you can use for enterprise and personal requires. Every one of the types are inspected by professionals and meet up with federal and state requirements.

When you are previously signed up, log in for your bank account and click on the Down load button to obtain the Montana Balloon Secured Note. Make use of bank account to appear through the legal types you possess bought formerly. Check out the My Forms tab of your bank account and acquire yet another backup in the file you want.

When you are a fresh consumer of US Legal Forms, allow me to share straightforward recommendations that you can comply with:

- Initially, be sure you have selected the proper type to your area/area. You can look through the shape making use of the Preview button and read the shape information to make certain this is basically the best for you.

- In the event the type fails to meet up with your expectations, utilize the Seach area to obtain the appropriate type.

- Once you are positive that the shape would work, click the Purchase now button to obtain the type.

- Choose the costs plan you desire and enter the needed information. Create your bank account and buy the transaction making use of your PayPal bank account or Visa or Mastercard.

- Select the file formatting and download the legal file format for your gadget.

- Complete, modify and produce and indicator the attained Montana Balloon Secured Note.

US Legal Forms is definitely the biggest collection of legal types for which you will find numerous file templates. Make use of the company to download skillfully-produced papers that comply with condition requirements.