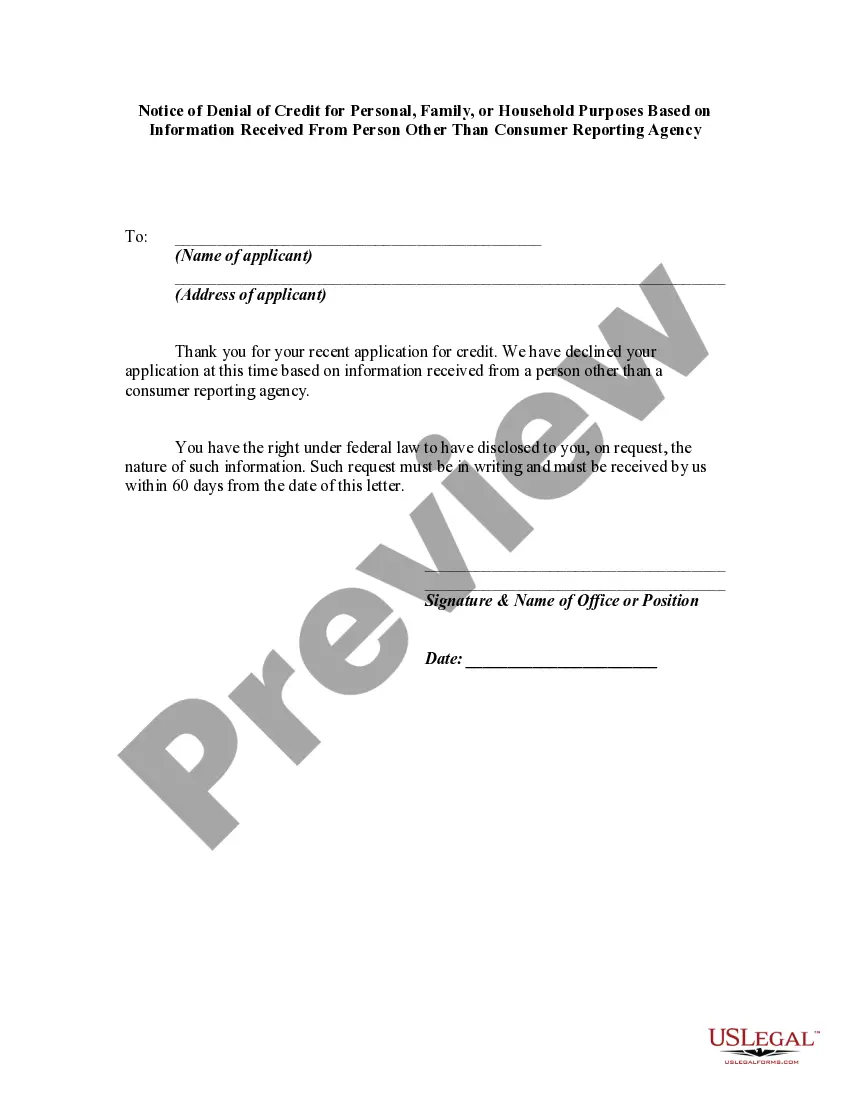

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information.

Montana Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document that provides detailed information about the denial of credit to an individual. This notice is necessary when a person's credit application has been denied based on information obtained from a source other than a consumer reporting agency. The purpose of this notice is to inform the individual of the specific reason(s) for the denial and to provide them with an opportunity to review and dispute the information used in making the decision. It is important to understand that this notice is not issued by a consumer reporting agency but by the entity that denied the credit application. Montana's law requires that this notice be provided within a certain timeframe and must include certain information to ensure compliance. The notice should clearly state the reason(s) for denial, including details of the information received from the person or entity that provided the adverse information. It is important to note that there may be different types of Montana Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency. These can vary depending on the specific circumstances and the type of credit being applied for. Some potential variations may include: 1. Montana Notice of Denial of Mortgage Loan Application: Commonly used when a person's application for a mortgage loan is denied based on adverse information obtained from a source other than a consumer reporting agency. 2. Montana Notice of Denial of Credit Card Application: Used when a credit card application is denied due to adverse information obtained from a person or entity other than a consumer reporting agency. 3. Montana Notice of Denial of Personal Loan Application: Applicable when an individual's application for a personal loan is denied based on information received from a source other than a consumer reporting agency. 4. Montana Notice of Denial of Student Loan Application: Used when a student loan application is denied due to adverse information obtained from a person or entity other than a consumer reporting agency. In conclusion, the Montana Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a critical document that outlines the reasons for credit denial and provides individuals with an opportunity to address and dispute the adverse information. It is crucial to understand the specific type of denial notice required based on the type of credit applied for in order to ensure compliance with Montana law.Montana Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document that provides detailed information about the denial of credit to an individual. This notice is necessary when a person's credit application has been denied based on information obtained from a source other than a consumer reporting agency. The purpose of this notice is to inform the individual of the specific reason(s) for the denial and to provide them with an opportunity to review and dispute the information used in making the decision. It is important to understand that this notice is not issued by a consumer reporting agency but by the entity that denied the credit application. Montana's law requires that this notice be provided within a certain timeframe and must include certain information to ensure compliance. The notice should clearly state the reason(s) for denial, including details of the information received from the person or entity that provided the adverse information. It is important to note that there may be different types of Montana Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency. These can vary depending on the specific circumstances and the type of credit being applied for. Some potential variations may include: 1. Montana Notice of Denial of Mortgage Loan Application: Commonly used when a person's application for a mortgage loan is denied based on adverse information obtained from a source other than a consumer reporting agency. 2. Montana Notice of Denial of Credit Card Application: Used when a credit card application is denied due to adverse information obtained from a person or entity other than a consumer reporting agency. 3. Montana Notice of Denial of Personal Loan Application: Applicable when an individual's application for a personal loan is denied based on information received from a source other than a consumer reporting agency. 4. Montana Notice of Denial of Student Loan Application: Used when a student loan application is denied due to adverse information obtained from a person or entity other than a consumer reporting agency. In conclusion, the Montana Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a critical document that outlines the reasons for credit denial and provides individuals with an opportunity to address and dispute the adverse information. It is crucial to understand the specific type of denial notice required based on the type of credit applied for in order to ensure compliance with Montana law.