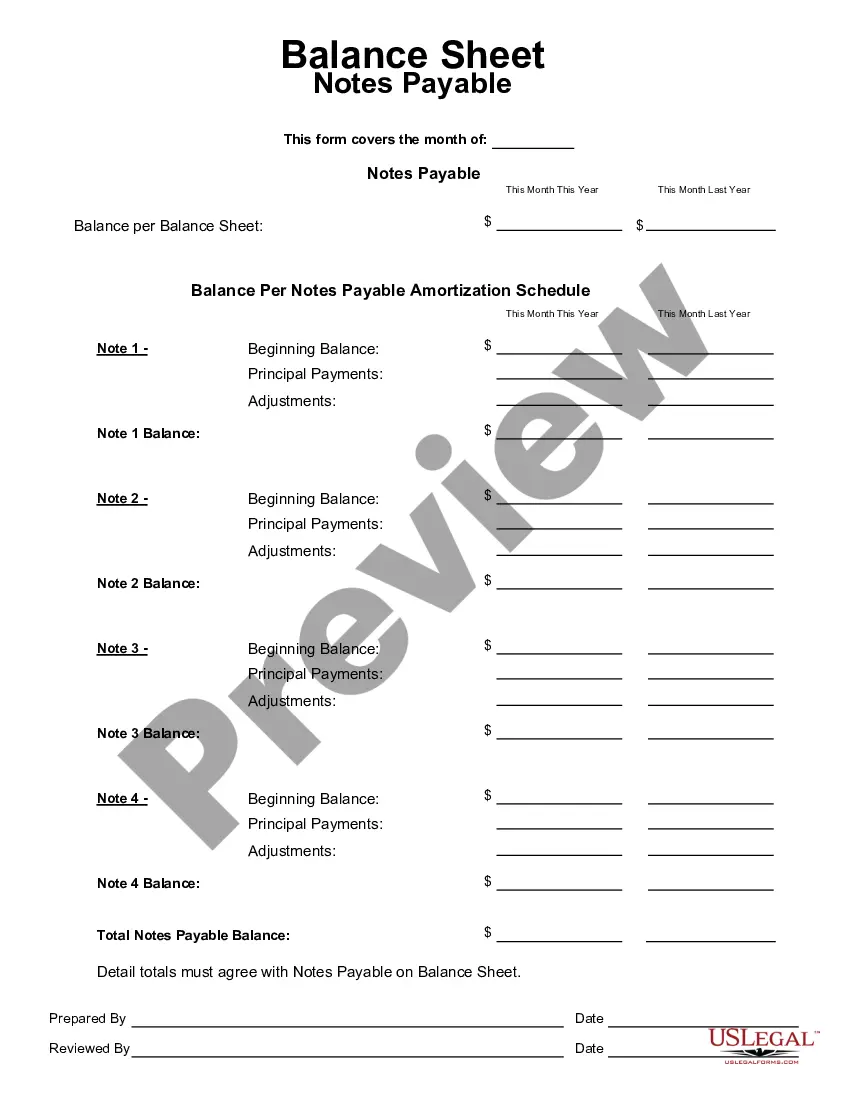

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Montana Report from Review of Financial Statements and Compilation by Accounting Firm is a comprehensive document that provides a detailed analysis of a company's financial statements and accounting practices. It is prepared by a professional accounting firm to provide an independent assessment of a company's financial health and compliance with accounting standards. The Montana Report from Review of Financial Statements and Compilation by Accounting Firm includes several key components. Firstly, the report will typically provide a brief introduction, outlining the purpose of the report and the scope of the review or compilation. It will also mention the period covered by the financial statements and any limitations to the review or compilation. Next, the report will discuss the accounting firm's responsibilities in performing the review or compilation. This may include determining whether the financial statements are free from material misstatements, assessing the adequacy of accounting policies, and evaluating the overall presentation of the financial statements. The report will then present the accounting firm's findings and conclusions. If the report is a Review of Financial Statements, it will provide a limited assurance statement, expressing that the accounting firm did not become aware of any material modifications that should be made to the financial statements. In the case of a Compilation, the report will state that the financial statements were prepared by management without the accounting firm expressing any assurance. Additionally, the Montana Report from Review of Financial Statements and Compilation by Accounting Firm may include other required elements such as management's responsibility for the financial statements, a summary of significant accounting policies, and any recommended adjustments or disclosures. There are various types of Montana Reports from Review of Financial Statements and Compilation by Accounting Firm, each serving a specific purpose and providing a distinct level of assurance. Some common types include: 1. Compilation Report: A compilation report is the most basic type of report. It involves presenting financial statements that have been prepared by management without any additional testing or auditing by the accounting firm. This report is typically used when users of the financial statements need basic financial information. 2. Review Report: A review report provides a higher level of assurance compared to a compilation report. The accounting firm performs analytical procedures and inquiries to obtain limited assurance that the financial statements are free of material misstatements. This report is often used when a company needs moderate assurance on the accuracy of its financial statements. In conclusion, the Montana Report from Review of Financial Statements and Compilation by Accounting Firm is a critical document that provides stakeholders with valuable insights into a company's financial health. It ensures transparency and reliability in financial reporting, thus assisting decision-makers, investors, and creditors in making informed judgments.Montana Report from Review of Financial Statements and Compilation by Accounting Firm is a comprehensive document that provides a detailed analysis of a company's financial statements and accounting practices. It is prepared by a professional accounting firm to provide an independent assessment of a company's financial health and compliance with accounting standards. The Montana Report from Review of Financial Statements and Compilation by Accounting Firm includes several key components. Firstly, the report will typically provide a brief introduction, outlining the purpose of the report and the scope of the review or compilation. It will also mention the period covered by the financial statements and any limitations to the review or compilation. Next, the report will discuss the accounting firm's responsibilities in performing the review or compilation. This may include determining whether the financial statements are free from material misstatements, assessing the adequacy of accounting policies, and evaluating the overall presentation of the financial statements. The report will then present the accounting firm's findings and conclusions. If the report is a Review of Financial Statements, it will provide a limited assurance statement, expressing that the accounting firm did not become aware of any material modifications that should be made to the financial statements. In the case of a Compilation, the report will state that the financial statements were prepared by management without the accounting firm expressing any assurance. Additionally, the Montana Report from Review of Financial Statements and Compilation by Accounting Firm may include other required elements such as management's responsibility for the financial statements, a summary of significant accounting policies, and any recommended adjustments or disclosures. There are various types of Montana Reports from Review of Financial Statements and Compilation by Accounting Firm, each serving a specific purpose and providing a distinct level of assurance. Some common types include: 1. Compilation Report: A compilation report is the most basic type of report. It involves presenting financial statements that have been prepared by management without any additional testing or auditing by the accounting firm. This report is typically used when users of the financial statements need basic financial information. 2. Review Report: A review report provides a higher level of assurance compared to a compilation report. The accounting firm performs analytical procedures and inquiries to obtain limited assurance that the financial statements are free of material misstatements. This report is often used when a company needs moderate assurance on the accuracy of its financial statements. In conclusion, the Montana Report from Review of Financial Statements and Compilation by Accounting Firm is a critical document that provides stakeholders with valuable insights into a company's financial health. It ensures transparency and reliability in financial reporting, thus assisting decision-makers, investors, and creditors in making informed judgments.