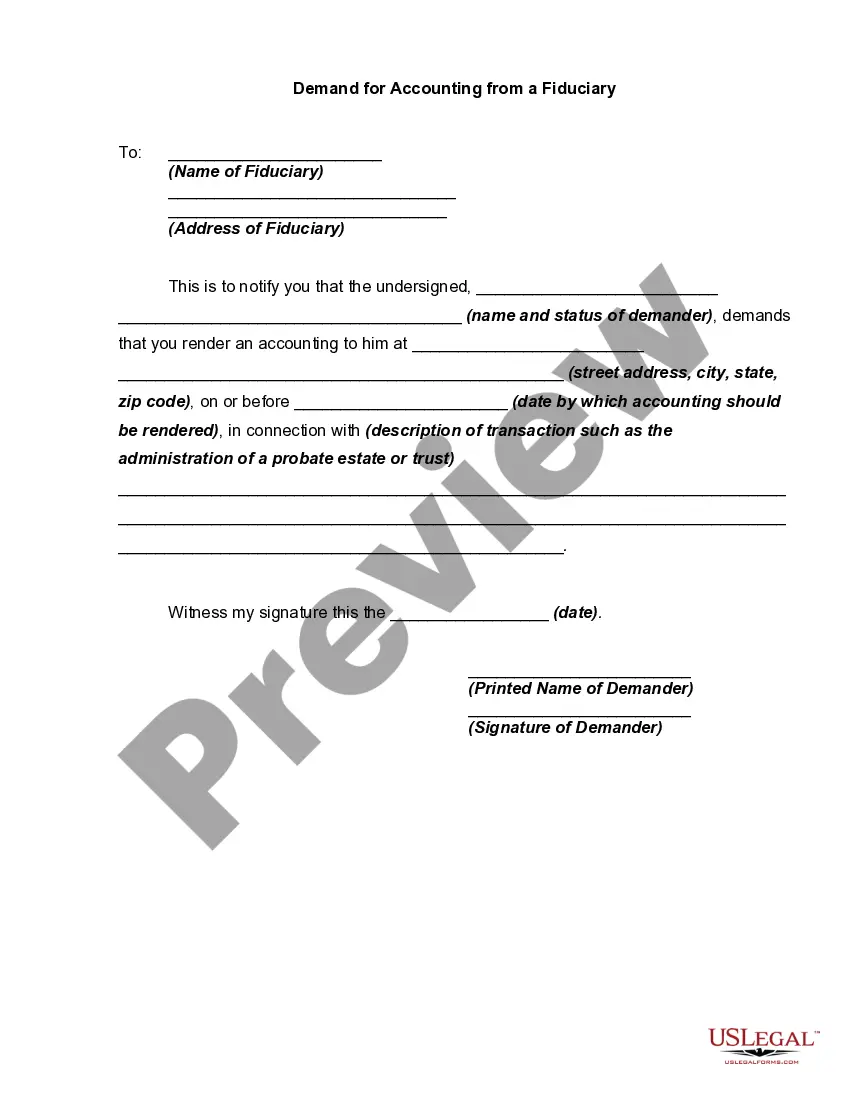

Sometimes, a prior demand by a potential plaintiff for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Title: Understanding the Montana Demand for Accounting from a Fiduciary: An In-depth Overview Introduction: In the state of Montana, a demand for accounting from a fiduciary is an essential legal procedure that ensures transparency and accountability in various fiduciary relationships. This article aims to provide a comprehensive understanding of what this demand entails, its purpose, and the types of demands one may encounter. Keywords: Montana fiduciary, demand for accounting, fiduciary relationships, transparency, accountability. I. What is a Montana Demand for Accounting from a Fiduciary? A Montana demand for accounting from a fiduciary refers to a legal request made by a beneficiary or a court to a fiduciary, compelling them to provide a detailed and accurate report of all financial transactions, assets, and liabilities connected to a specific fiduciary relationship. Keywords: legal request, beneficiary, court, financial transactions, assets, liabilities. II. Purpose and Importance: The demand for accounting serves various crucial purposes, including: 1. Ensuring transparency: By compelling a fiduciary to disclose financial information, the demand for accounting promotes transparency and allows beneficiaries to gain a clear understanding of their rights and interests. 2. Verifying fiduciary conduct: The demand enables beneficiaries to verify the fiduciary's actions and ensure that they are acting in compliance with their legal obligations and responsibilities. 3. Preventing mismanagement or fraud: Accounting demands act as a safeguard against potential mismanagement, negligence, or fraudulent activities by unveiling any irregularities or discrepancies in the fiduciary's financial records. 4. Resolving disputes: If conflicts arise between beneficiaries and fiduciaries regarding financial matters, a demand for accounting provides an avenue for resolution by bringing forth accurate financial information to support or resolve disputes. Keywords: transparency, beneficiaries, rights, interests, fiduciary conduct, mismanagement, fraud, disputes. III. Types of Montana Demand for Accounting from a Fiduciary: There are several types of demand for accounting a beneficiary may potentially utilize, depending on the specific fiduciary relationship and the circumstances involved. These can include: 1. Formal Judicial Accounting Demand: Initiated by filing a lawsuit in a Montana court, this demand entails obtaining a detailed accounting of the fiduciary's financial activities while under court supervision. 2. Informal Accounting Demand: Beneficiaries may send a written request to the fiduciary, asking for a voluntary accounting without involving the court system. Although not legally binding, it can often lead to resolution and a better understanding of the fiduciary's activities. Keywords: formal judicial accounting demand, lawsuit, court supervision, informal accounting demand, written request, voluntary accounting. Conclusion: In summary, a Montana demand for accounting from a fiduciary is a vital tool that ensures transparency, accountability, and the protection of beneficiaries in various fiduciary relationships. By understanding its purpose and the available types of demand, beneficiaries can assert their rights and address any concerns they may have in these relationships. Keywords: Montana demand for accounting, fiduciary relationships, transparency, accountability, protection, beneficiaries, legal rights.