This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

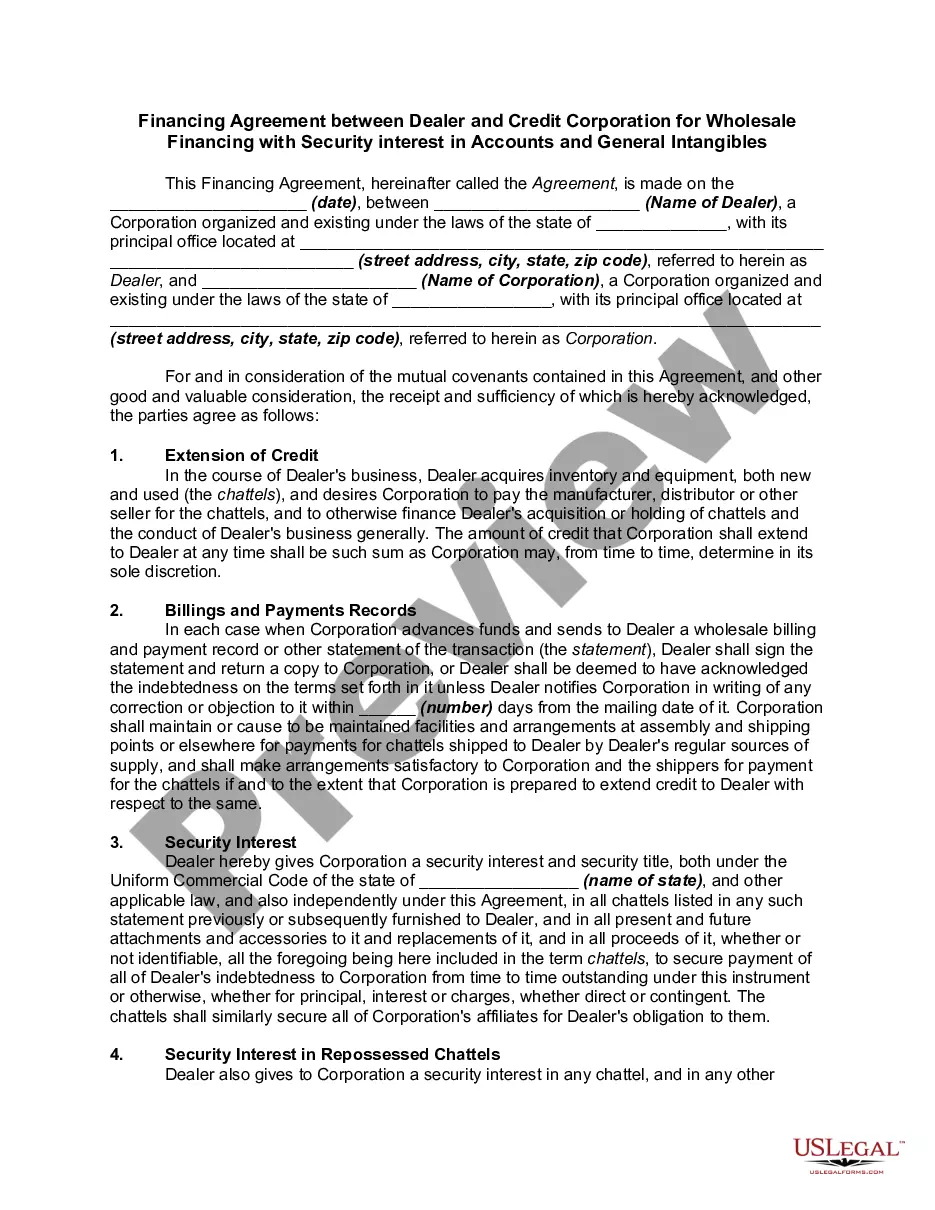

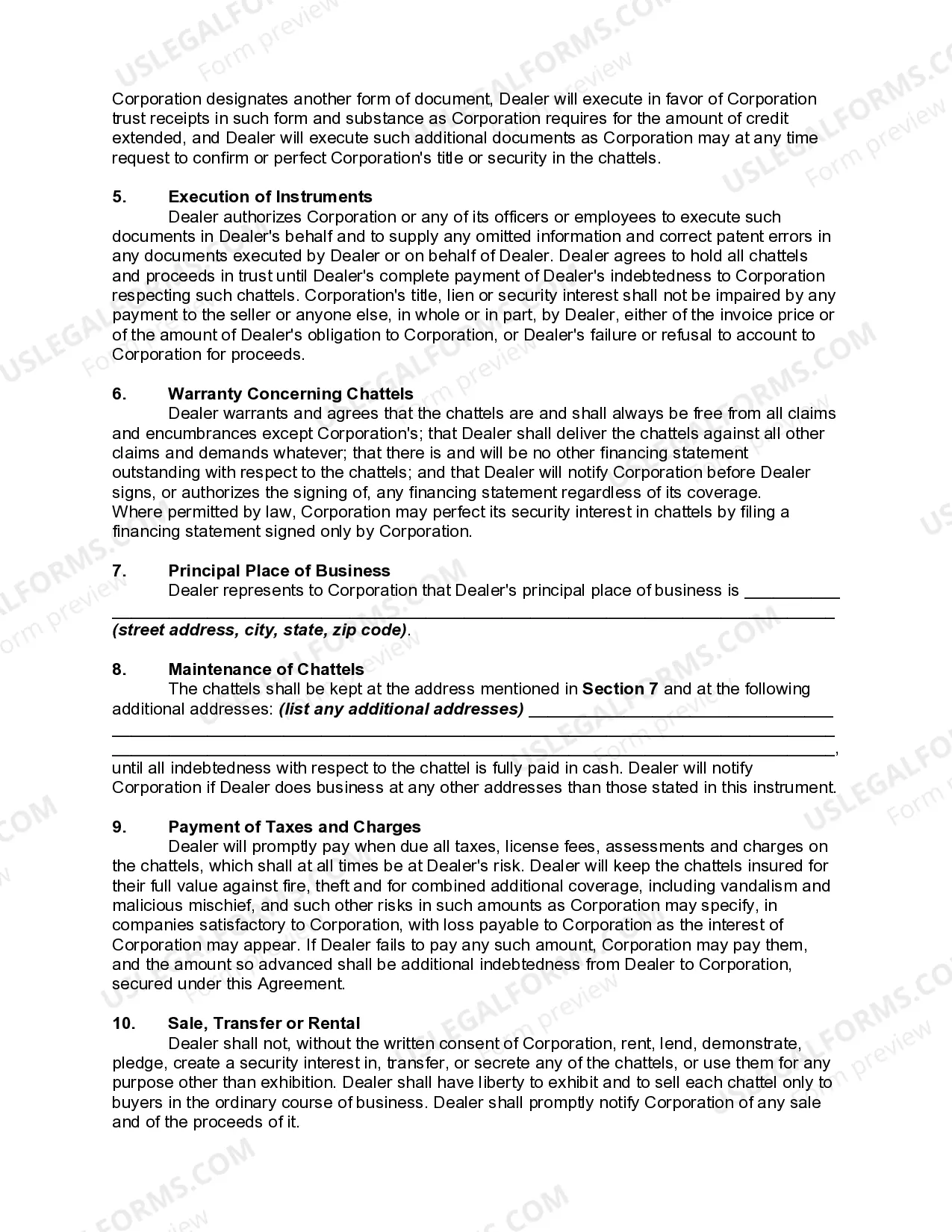

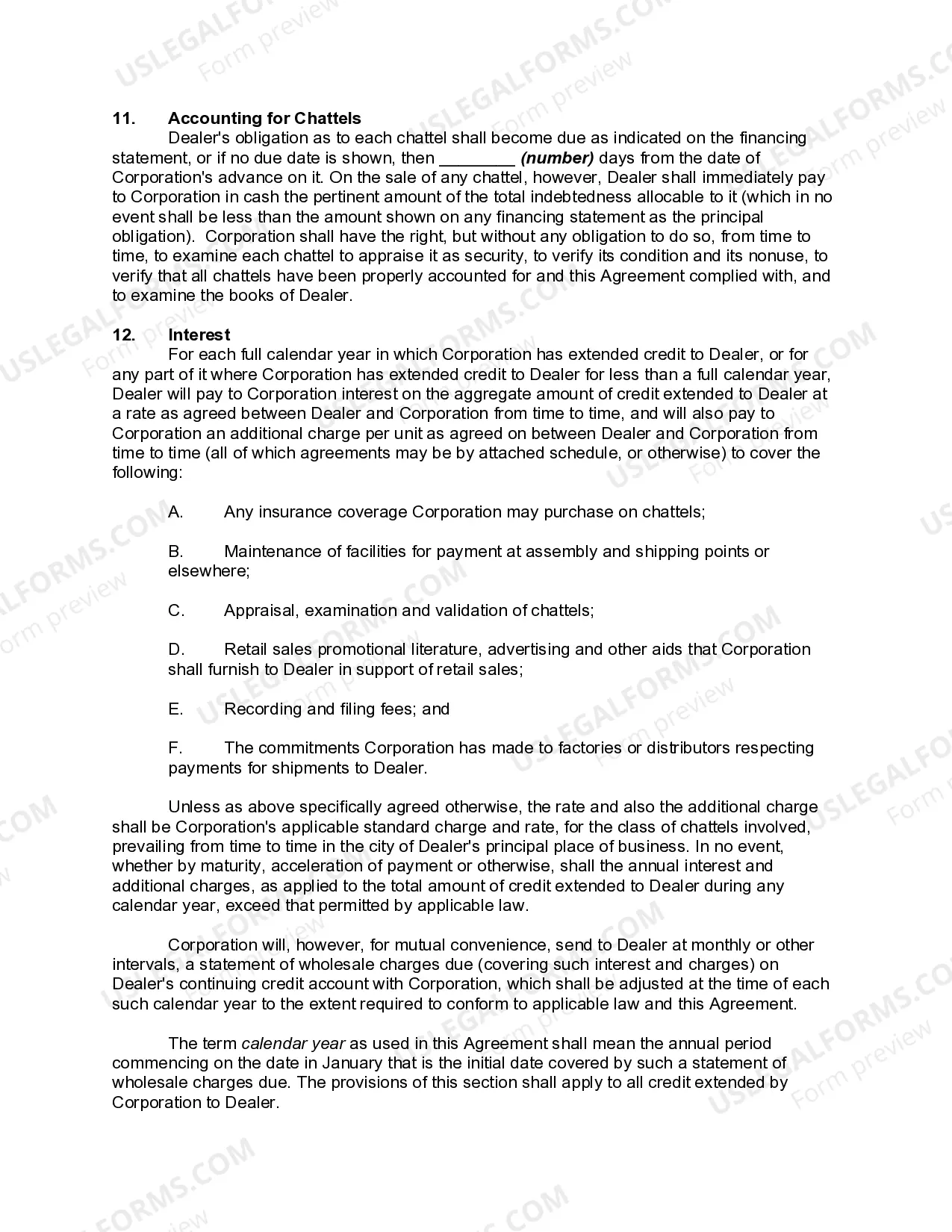

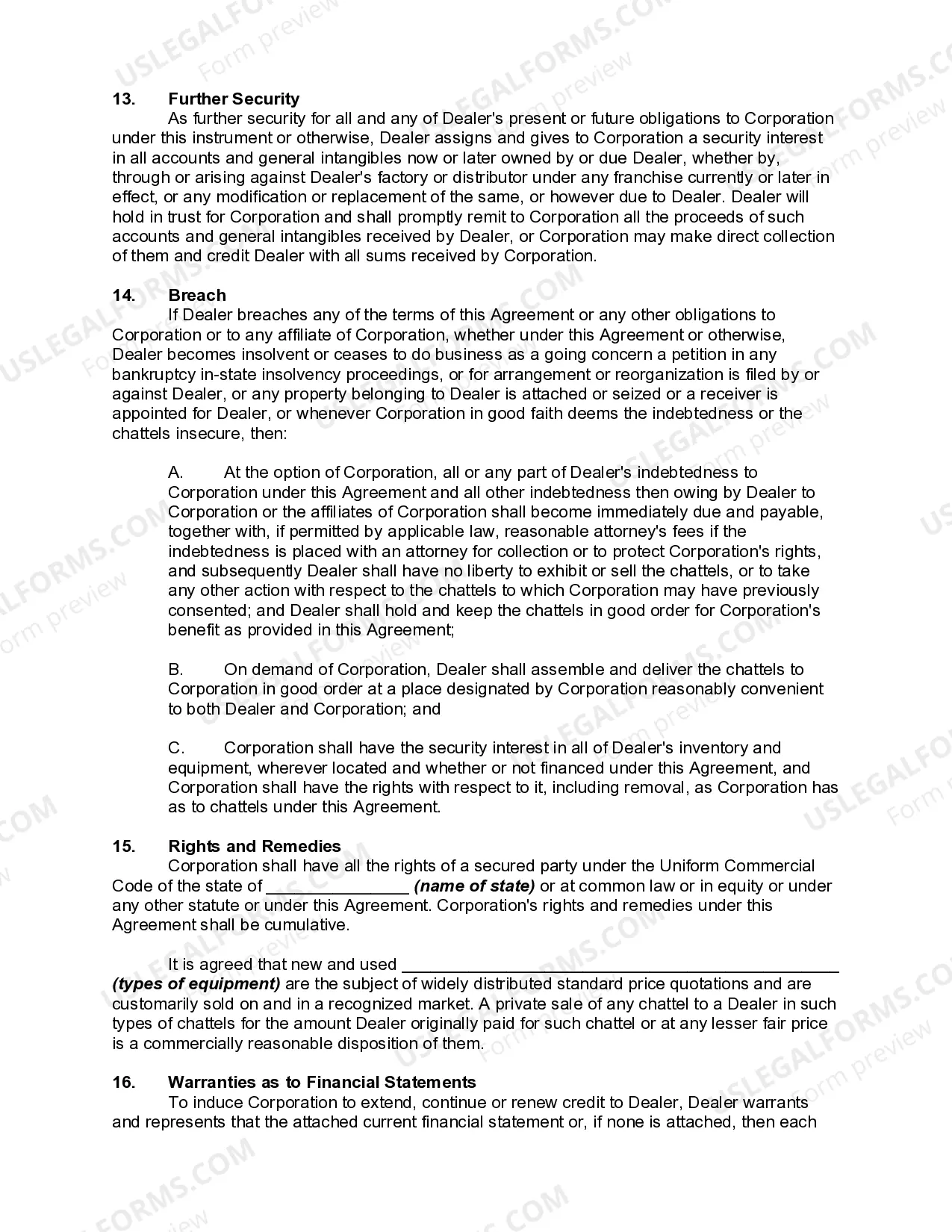

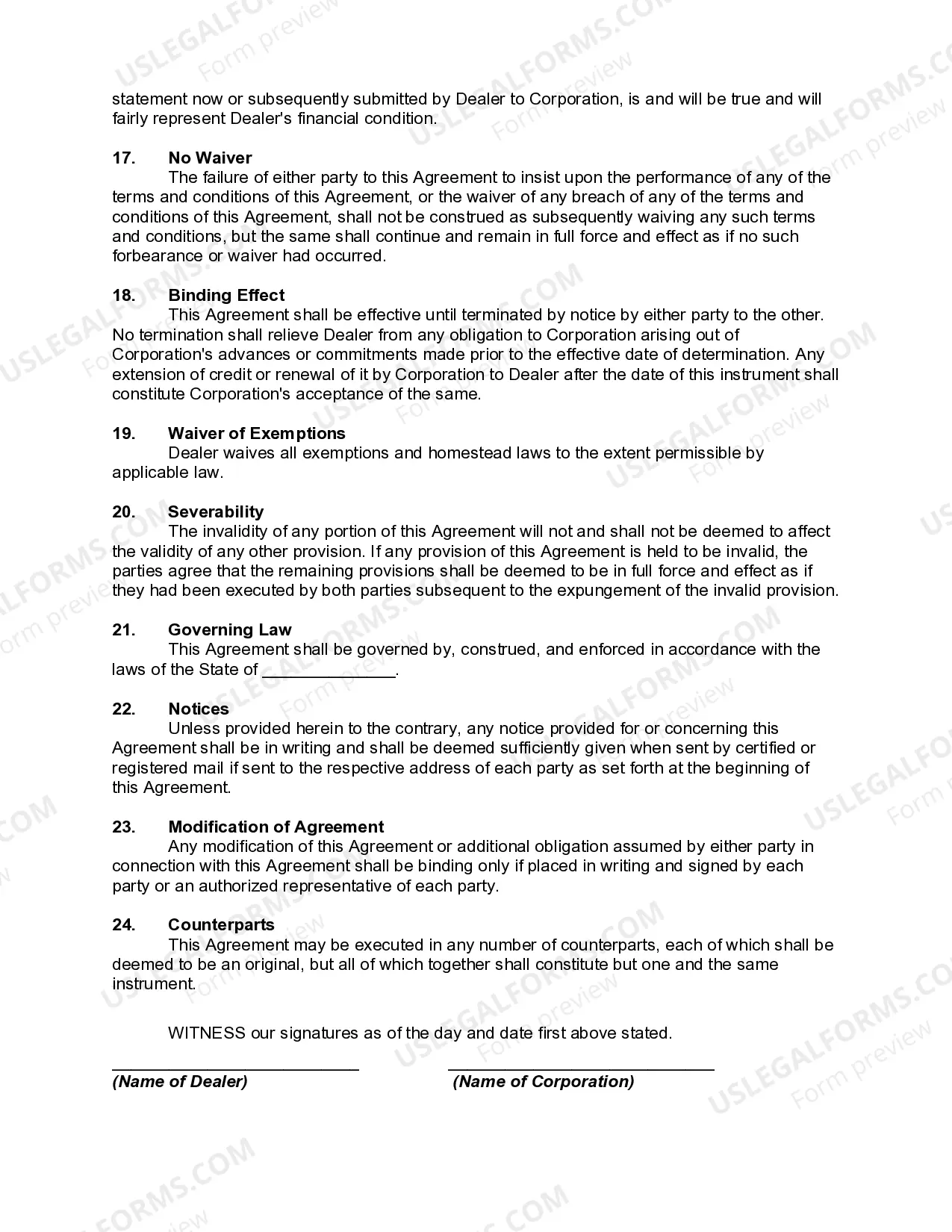

Keywords: Montana Financing Agreement, Dealer, Credit Corporation, Wholesale Financing, Security Interest, Accounts, General Intangibles Description: A Montana Financing Agreement between a dealer and a credit corporation for wholesale financing with a security interest in accounts and general intangibles is a legal contract that outlines the terms and conditions under which a dealer obtains financing from a credit corporation for their wholesale operations. This type of agreement is commonly used in Montana to facilitate the smooth functioning of wholesale businesses, particularly in industries such as automotive, consumer electronics, and industrial equipment. These financing agreements serve as a means for dealers to secure the necessary funds to purchase inventory and manage their wholesale operations effectively. By obtaining financing from a credit corporation, dealers can stock their inventory, expand their product offerings, and fulfill orders from their customers in a timely manner. The Montana Financing Agreement typically includes specific provisions that outline the responsibilities and obligations of both parties involved. It establishes the terms of the loan, detailing the amount of financing provided, the interest rate, and the repayment schedule. The agreement also specifies the dealership's obligations, such as providing regular financial statements and maintaining proper inventory records. In order to secure the loan, the credit corporation typically requires a security interest in the dealer's accounts and general intangibles. This means that the credit corporation has a legal claim on the dealer's assets, including accounts receivable, customer lists, and other intangible assets. This security interest provides collateral for the credit corporation in case the dealer defaults on their loan obligations. There might be different types of Montana Financing Agreements between dealers and credit corporations based on the specific industry or nature of the wholesale business. These agreements can include variations in terms, interest rates, repayment options, and the extent of security interests. For example, in the automotive industry, there might be specific financing agreements tailored to dealerships specializing in new vehicles versus used vehicles. In conclusion, the Montana Financing Agreement between a dealer and a credit corporation for wholesale financing with security interest in accounts and general intangibles is a crucial legal contract for dealers in Montana. It allows them to access the necessary funds to operate their wholesale businesses, expand their offerings, and meet the demands of their customers. These agreements provide benefits for both parties involved and ensure a mutually beneficial relationship in the wholesale industry.