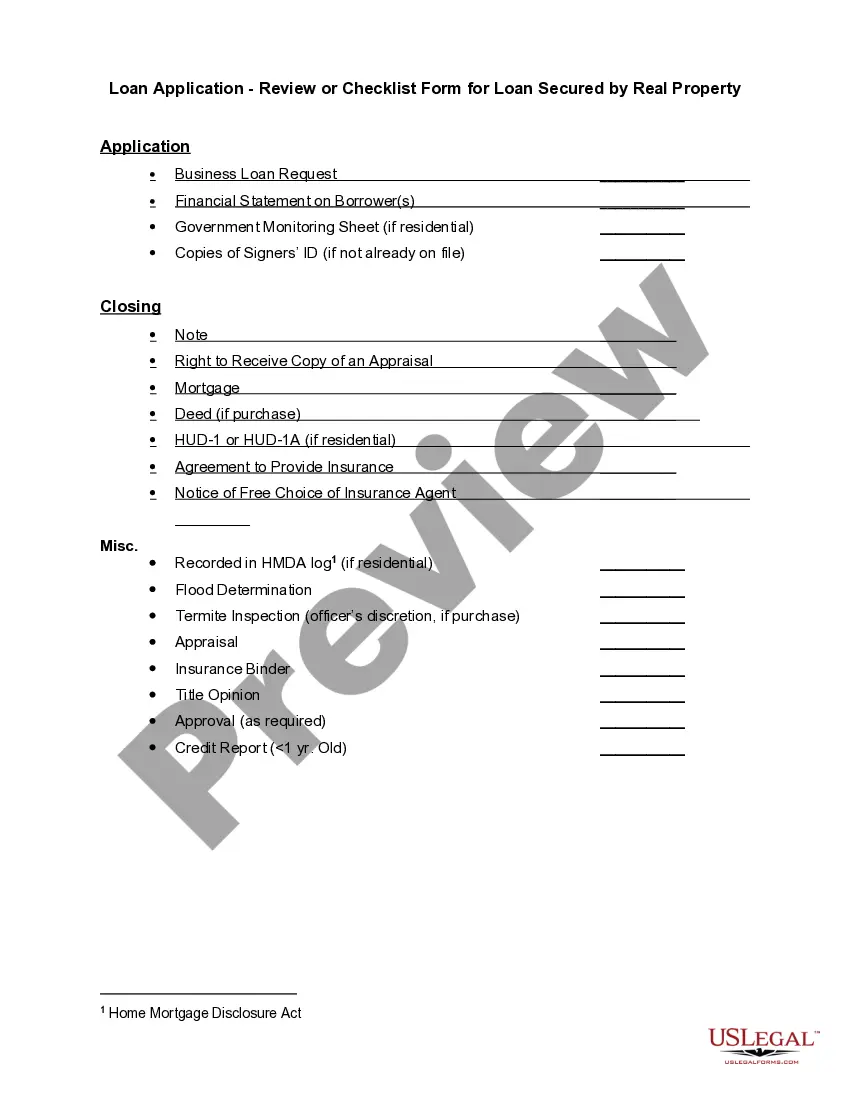

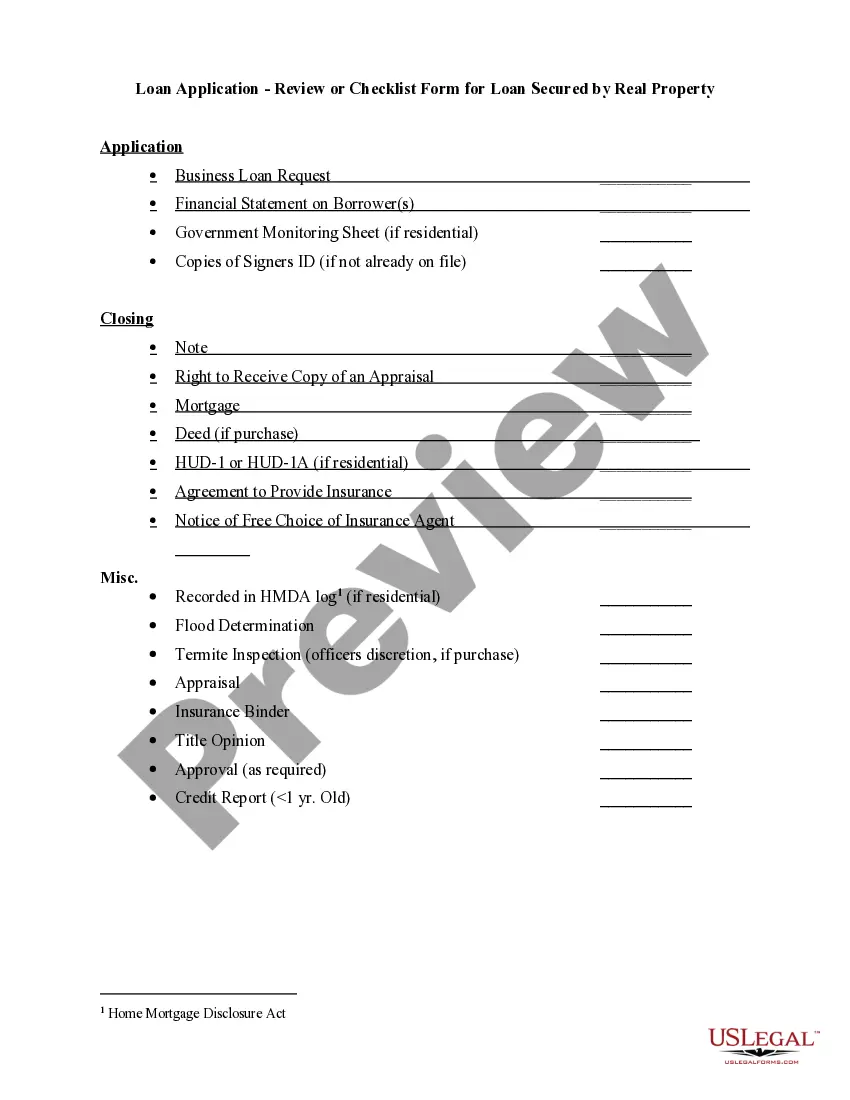

Montana Checklist for Business Loans Secured by Real Estate

Description

How to fill out Checklist For Business Loans Secured By Real Estate?

If you wish to complete, down load, or printing authorized record web templates, use US Legal Forms, the biggest collection of authorized varieties, that can be found on-line. Make use of the site`s simple and practical look for to discover the papers you will need. Various web templates for business and individual purposes are categorized by categories and claims, or keywords. Use US Legal Forms to discover the Montana Checklist for Business Loans Secured by Real Estate within a handful of clicks.

In case you are currently a US Legal Forms client, log in to your account and click on the Download button to obtain the Montana Checklist for Business Loans Secured by Real Estate. You can also access varieties you in the past saved inside the My Forms tab of the account.

If you are using US Legal Forms for the first time, follow the instructions below:

- Step 1. Make sure you have selected the form for the appropriate metropolis/nation.

- Step 2. Make use of the Preview choice to check out the form`s content. Never neglect to read through the explanation.

- Step 3. In case you are not satisfied using the type, take advantage of the Research field at the top of the screen to get other models from the authorized type template.

- Step 4. After you have identified the form you will need, go through the Buy now button. Opt for the rates prepare you favor and include your accreditations to sign up on an account.

- Step 5. Method the transaction. You may use your credit card or PayPal account to accomplish the transaction.

- Step 6. Find the file format from the authorized type and down load it in your system.

- Step 7. Comprehensive, change and printing or signal the Montana Checklist for Business Loans Secured by Real Estate.

Each and every authorized record template you acquire is your own for a long time. You may have acces to each type you saved in your acccount. Click on the My Forms portion and pick a type to printing or down load yet again.

Be competitive and down load, and printing the Montana Checklist for Business Loans Secured by Real Estate with US Legal Forms. There are thousands of specialist and express-distinct varieties you can utilize for your business or individual demands.

Form popularity

FAQ

Real estate and home equity are the most commonly offered collateral for small businesses because a house is typically the most valuable asset an individual possesses. However, most banks will only take a small fraction of equity accrued on a house as collateral because they follow stringent debt-to-income ratios.

Using property as collateral on a business loan Lenders prefer assets of a high value that can be resold relatively quickly in the event of default. This allows them to recoup their money with few issues and as property is one of the highest value assets available, it's commonly used to secure a business loan.

Secured business loans enable you to access funding by providing an asset, such as a property your business owns, as security. Because there's less risk to the lender, interest rates can be lower compared to unsecured business loan rates. The lender can sell your asset to recover the funds if you don't repay.

What can I use as collateral for a business loan? Cash is the most liquid form of collateral, while securities like treasury bonds, stocks, certificates of deposit (CDs) and corporate bonds can also be used. Tangible assets, such as real estate, equipment, inventory and vehicles, are another popular form of collateral.

Secured business loans use collateral to reduce lender risk, allowing small business owners to potentially unlock more attractive rates and terms. Collateral can include cash deposits, business assets or real estate. But if you fail to repay the loan, the lender can seize the collateral to recoup its losses.

A secured business loan requires a specific piece of collateral, such as a business vehicle or commercial property, which the lender can claim if you fail to repay your loan.