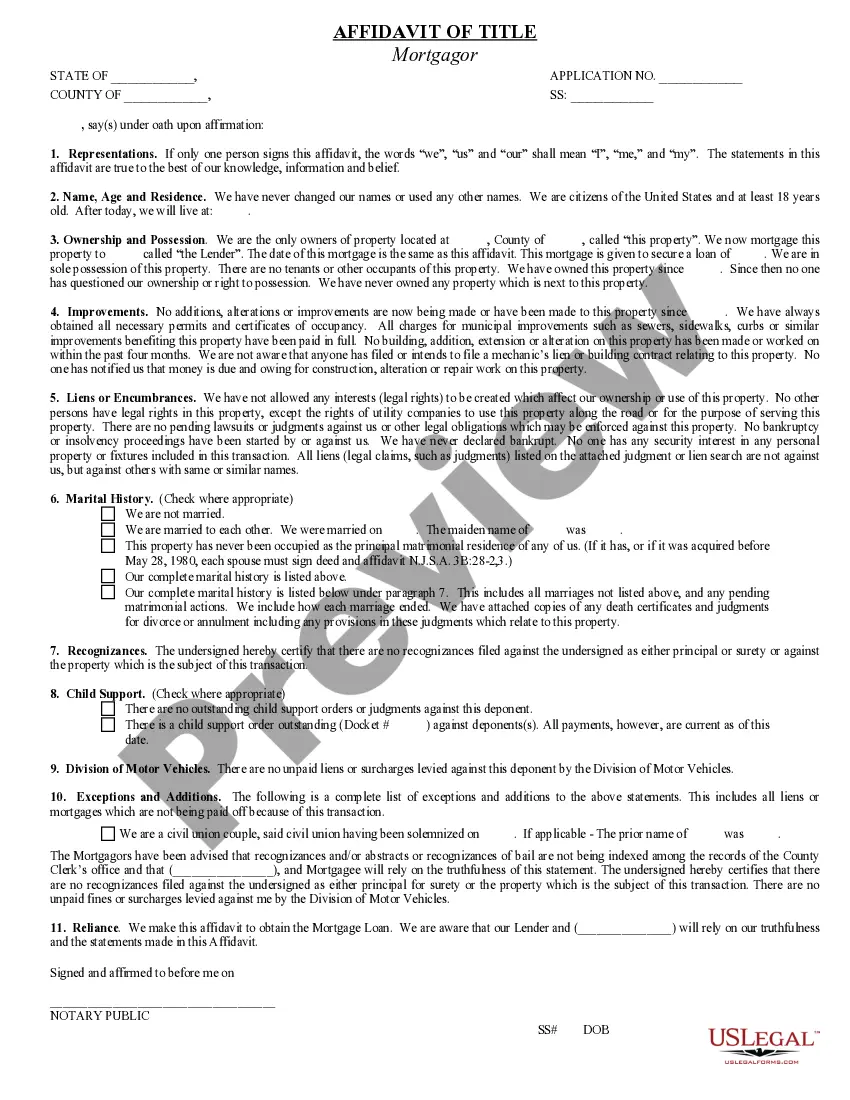

Montana Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

If you have to full, obtain, or produce authorized record web templates, use US Legal Forms, the greatest assortment of authorized types, which can be found online. Take advantage of the site`s basic and handy search to get the papers you require. Various web templates for enterprise and person functions are categorized by groups and states, or key phrases. Use US Legal Forms to get the Montana Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage in just a couple of mouse clicks.

When you are presently a US Legal Forms consumer, log in to the bank account and then click the Download key to obtain the Montana Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage. Also you can accessibility types you earlier saved within the My Forms tab of the bank account.

Should you use US Legal Forms initially, follow the instructions below:

- Step 1. Ensure you have chosen the form for the right metropolis/nation.

- Step 2. Make use of the Preview method to examine the form`s information. Never forget to see the description.

- Step 3. When you are unsatisfied using the type, make use of the Research discipline at the top of the display screen to discover other versions of your authorized type template.

- Step 4. After you have discovered the form you require, select the Buy now key. Opt for the costs prepare you prefer and add your accreditations to sign up on an bank account.

- Step 5. Method the transaction. You can utilize your charge card or PayPal bank account to perform the transaction.

- Step 6. Select the formatting of your authorized type and obtain it in your system.

- Step 7. Comprehensive, change and produce or sign the Montana Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage.

Each authorized record template you buy is the one you have forever. You have acces to every single type you saved in your acccount. Select the My Forms section and select a type to produce or obtain yet again.

Remain competitive and obtain, and produce the Montana Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage with US Legal Forms. There are thousands of professional and express-particular types you can utilize for the enterprise or person requires.

Form popularity

FAQ

TL;DR: The primary mortgage market is used for homebuyers and lenders. Lenders finance a borrower's purchase of a home. The secondary mortgage market is between lenders and mortgage investors. Lenders will sell the debt to the investor who will buy it to make a profit.

A first mortgage is a primary lien on the property that secures the mortgage. The second mortgage is money borrowed against home equity to fund other projects and expenditures.

First Mortgagee means any person named as a mortgagee or beneficiary in any First Mortgage, or any successor to the interest of any such person under such First Mortgage.

A second mortgage, however, allows you to use your home's equity and put it to work. Instead of having that money tied up in your home, it's available for expenses you have right now. This option can be a help or a hindrance, depending on your financial goals.

The Bottom Line Because the second mortgage also uses the same property for collateral as the first mortgage, the original mortgage has priority on the collateral should the borrower default on their payments. If the loan goes into default, the first mortgage lender gets paid before the second mortgage lender.