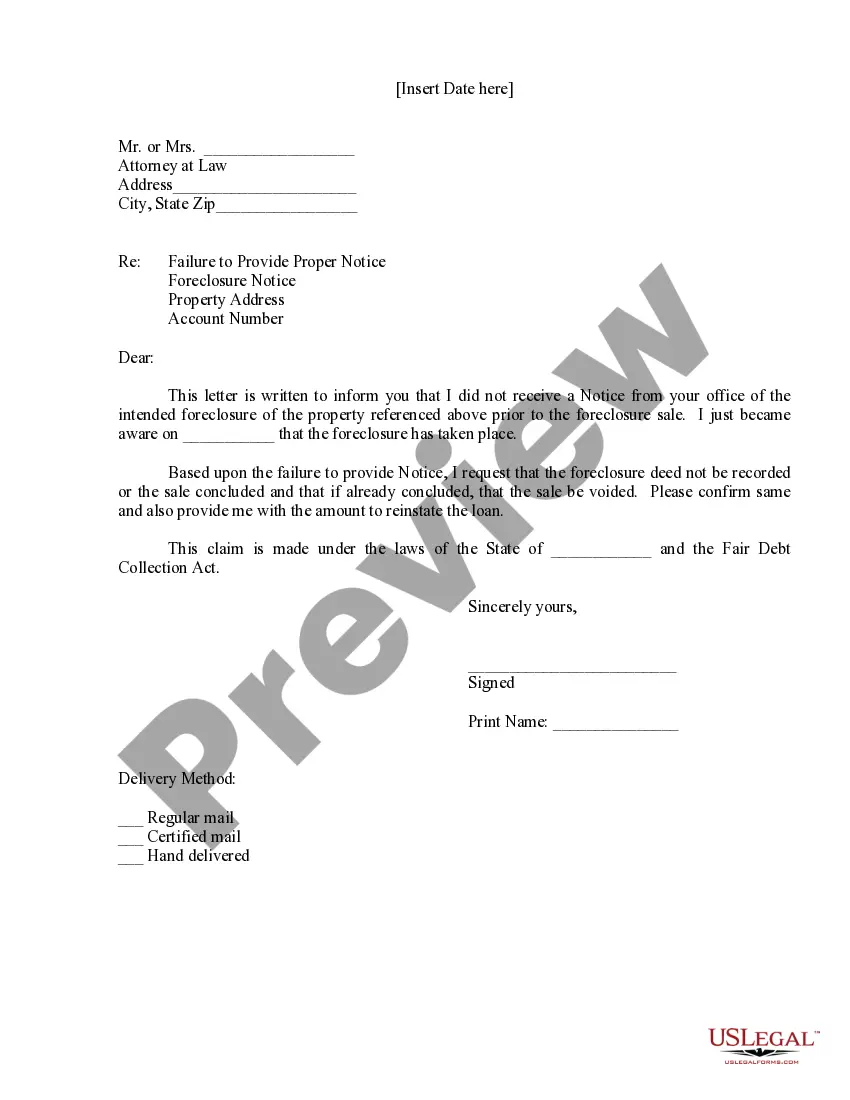

Montana Sample Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Letter To Foreclosure Attorney - After Foreclosure - Did Not Receive Notice?

US Legal Forms - one of the largest libraries of lawful kinds in the United States - offers an array of lawful file themes you may down load or produce. Making use of the web site, you will get a huge number of kinds for organization and personal purposes, categorized by classes, suggests, or key phrases.You can find the most recent types of kinds such as the Montana Sample Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice within minutes.

If you currently have a subscription, log in and down load Montana Sample Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice through the US Legal Forms catalogue. The Download option will show up on every form you perspective. You have access to all formerly delivered electronically kinds inside the My Forms tab of your account.

In order to use US Legal Forms the very first time, listed below are basic recommendations to help you get started off:

- Be sure to have picked the right form for the town/county. Select the Review option to examine the form`s content. Look at the form explanation to actually have selected the proper form.

- In case the form does not match your needs, make use of the Search area at the top of the display to obtain the the one that does.

- If you are content with the shape, validate your choice by clicking the Buy now option. Then, choose the prices plan you favor and offer your credentials to register for an account.

- Approach the financial transaction. Use your bank card or PayPal account to finish the financial transaction.

- Pick the formatting and down load the shape on the device.

- Make modifications. Fill out, change and produce and indicator the delivered electronically Montana Sample Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice.

Each web template you put into your account does not have an expiry particular date which is your own eternally. So, if you want to down load or produce yet another backup, just check out the My Forms area and click on about the form you need.

Get access to the Montana Sample Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice with US Legal Forms, the most extensive catalogue of lawful file themes. Use a huge number of professional and status-distinct themes that fulfill your small business or personal needs and needs.

Form popularity

FAQ

Judicial: In Mississippi, the lenders can file in court for a judicial foreclosure proceeding, where the court must issue a final judgment of foreclosure. The property is then sold as part of a publicly noticed sale by the sheriff.

No Redemption Period After a Nonjudicial Foreclosure in Mississippi. Some states have a law that gives a foreclosed homeowner time after the foreclosure sale to redeem the property. In Mississippi, however, you don't get a post-sale redemption period after a foreclosure.

A homeowner has many options to stop a foreclosure in Mississippi, which are follows: Deed in lieu of foreclosure: The borrower transfers the property to lender, who then waives the mortgage debt and doesn't pursue foreclosure. Forbearance: The lender agrees to reduce or suspend payments for a period of time.

If you miss four consecutive mortgage payments (120 days), most lenders begin the process of foreclosure on your home. If you miss one mortgage payment, lenders will often issue you a 15-day grace period to pay without incurring a penalty.

On the contrary, Mississippi laws do not give the right of redemption after the foreclosure. The borrower may have the right to stop the non-judicial foreclosure when you ?reinstate? the loan, as long as the total overdue amount (including interest and fees) will be paid off.

The foreclosed homeowner might get a five-day notice to quit (leave). While you can stay in the property until you're forcibly removed through the eviction process, it's generally best to leave before the deadline to move out given in the notice to quit expires.

Put your name, address, phone number, loan number, and date on the top of the letter. List the name and address of your lender. information about any money you have saved for a workout agreement. Tell the lender you are working with a foreclosure counselor and include their name and agency.

Under the PTFA, the lease survives foreclosure. You may stay in the property for the entire term of your lease or 90 days, whichever is longer. The only exception to this rule is if the new owner wants to live in your unit, in which case you are still entitled to 90 days before you can be forced to move.